Two Software Stocks the AI Narrative Broke

Unlocked Edition #4. February 2026

Sometimes the best opportunities show up when an entire sector is in the penalty box. Today’s idea is a double feature: buying two beaten-down U.S. software names — Backblaze and Sprinklr — after the recent AI-driven selloff. Both look priced for disappointment. We think at least one (and possibly both) deserves a rebound.

You’re reading a free weekly idea. Want 1–3 ideas every Tuesday plus access to 40+ live ideas? Consider becoming a paid subscriber. Already a subscriber? Enjoy the new Unlocked Edition at no additional cost.

Issuers

Backblaze (NASDAQ: BLZE) is a cloud provider that allows businesses and consumers to store, access, and protect data.

Sprinklr (NYSE: CXM) makes customer engagement and social media management software for enterprises.

Expected Profits

Backblaze: 31.5% profit in 16 months; ~250% profit in 12 years (11% CAGR).

Sprinklr: 34.5% profit in 2 years.

Description of the Business

Backblaze. It’s a cloud storage company — somewhat like Amazon Web Services, but focused on simpler, lower-cost storage solutions. Businesses and individuals pay Backblaze to back up and protect their data. At its core, it’s a server backup and cloud storage business built around affordability and ease of use.

Here’s how revenue broke down in 2024:

Subscription-based arrangements — 51.44%. Customers pay a fixed recurring fee for access.

Consumption-based arrangements — 48.15%. Revenue depends on how much storage customers actually use.

Physical media — 0.41%. Products such as USB Restore and the Fireball device, which allow customers to move or recover large datasets offline.

Most of Backblaze’s revenue comes from the U.S. (73.9%). The UK follows at 5.25%, then Canada at 4.51%, with the remainder spread globally.

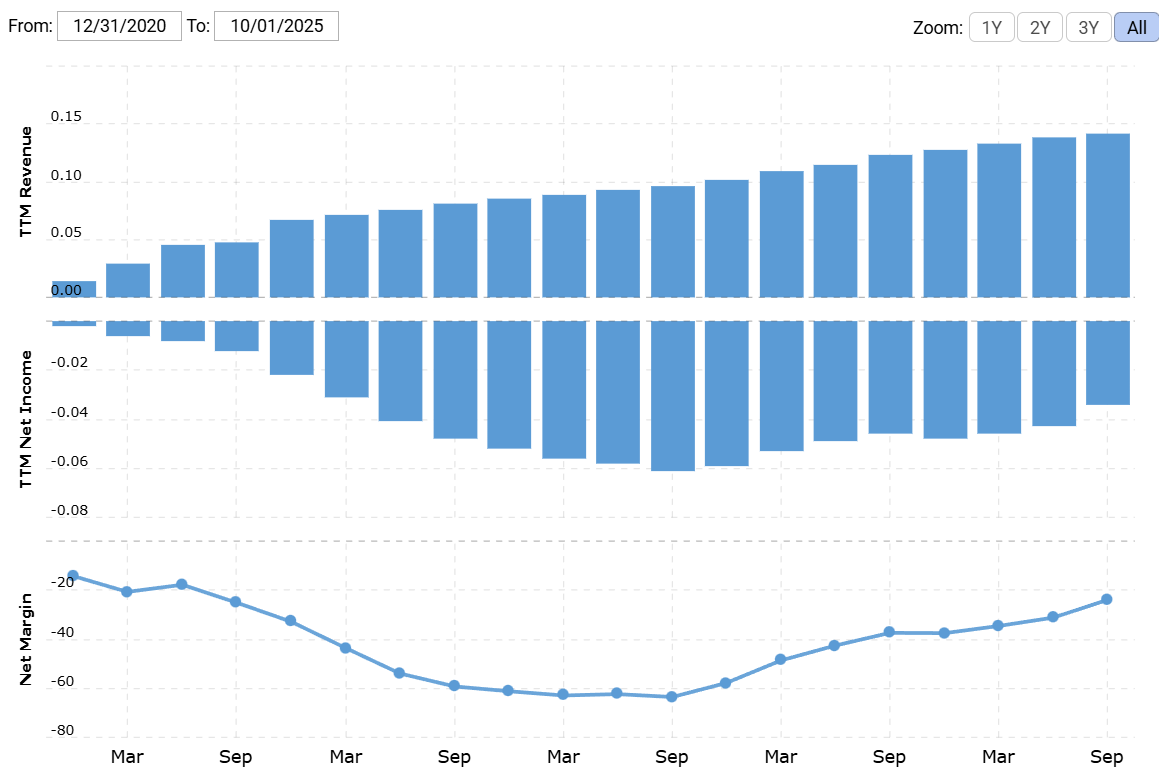

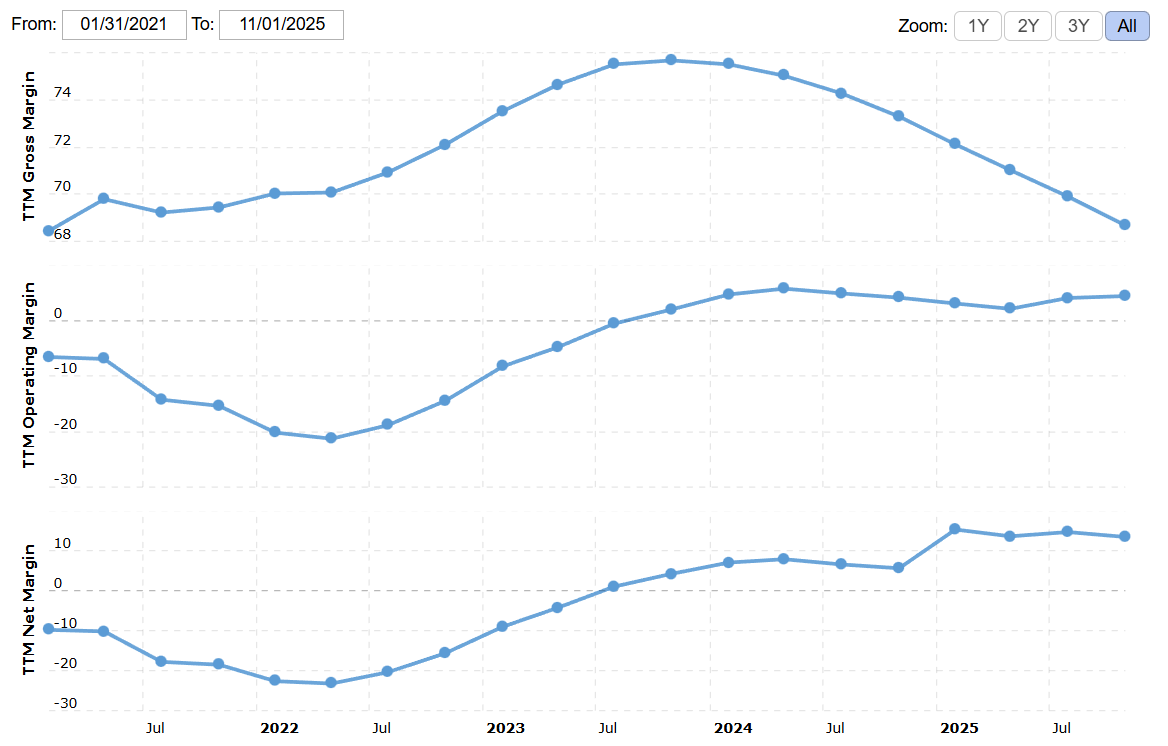

Backblaze is not yet profitable. For the 12-month period ended September 30, 2025, gross margin was 59.12%, operating margin was -23.07%, and net margin was -24.37%. In other words, it’s still in investment mode.

Sprinklr. The company builds enterprise software that helps companies manage customer support and social media presence across multiple channels. Think of it as the digital command center for customer interaction and brand monitoring.

For the fiscal year ended January 31, 2025, revenue looked like this:

Subscriptions — 90.15%. Recurring payments for platform access.

Segment gross margin: 80.4%.Professional services — 9.85%. Consulting and implementation work to tailor the software to client needs.

Segment gross margin: -3.66% (the segment loses money but supports subscription adoption).

More than half of Sprinklr’s revenue comes from the U.S. (54.46%), followed by EMEA at 33.78%. The rest is spread across the Western Hemisphere and other global markets.

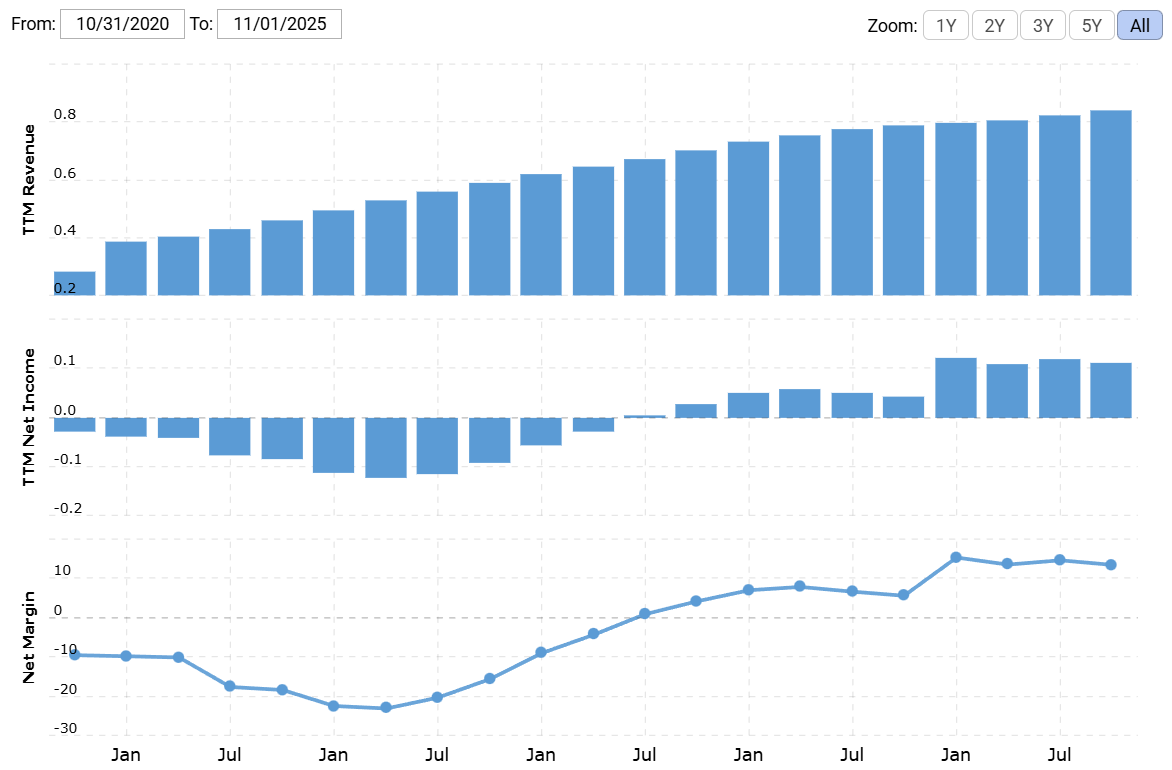

Sprinklr is profitable — at least on paper. For the 12-month period ended September 30, 2025, its gross margin was 68.68%, operating margin 4.35%, and net margin 13.42%. However, the net margin was partly boosted by one-time non-operating gains (we’ll revisit that in the “Cons”).

Why These Stocks Are Down

Neither company committed a catastrophic error, yet both trade near historic lows. Since 2021, Backblaze has lost roughly 62% of its market value, while Sprinklr has dropped about 79%.

Some of that decline was justified. Both companies once grew faster and traded at much richer multiples. When growth normalized, valuations compressed. That re-rating phase is largely behind us.

The more recent pressure comes from a broader wave of anti-software sentiment. The launch of a new AI tool by Anthropic rattled the sector and triggered another round of selling across software stocks. Billions in market cap evaporated in days.

We think that reaction is excessive. AI disruption is real — but its pace, impact, and winners are still uncertain. Historically, when sectors swing from “priced for perfection” to “priced for extinction,” selective bargains emerge.

Many software stocks now trade near multi-year lows. Eventually, active investors begin rotating back into names that look cheap relative to fundamentals.

The selloff also makes M&A more plausible. At current valuations, both Backblaze and Sprinklr could attract strategic buyers or minority investors looking to gain exposure at a discount.

Finally, the current prices don’t fully reflect improving business trends. Both companies traded at much higher valuations when revenue growth and profitability metrics were actually worse. That disconnect — stronger fundamentals, weaker share prices — is often where opportunity hides.

Backblaze: Pros

Cloud Remains a Structural Tailwind. Even before AI entered the mainstream, global data creation was exploding. AI only accelerates that trend. More data means more storage. Storage doesn’t disappear just because AI gets smarter — in fact, AI models require massive datasets to function.

Extremely Cheap. Backblaze’s market cap is just about $247 million. Its P/S is about 1.6. That’s modest for a cloud infrastructure company, even a small one.

AI-resilient — for Now. Backblaze stores data. AI may change how data is processed, but it doesn’t eliminate the need to store it. Unless the economics of cloud storage fundamentally shift, Backblaze’s core demand remains intact.

Sprinklr: Pros

Relatively Cheap. Sprinklr’s market cap is about $1.37 billion, trading at roughly 1.65x P/S.

A Real Business. Many software companies burn cash. Sprinklr generates operating profit. Customer service and social media management remain core priorities for enterprises worldwide, and that shows up in Sprinklr’s results (though cracks are starting to appear—more on that in the “Cons”).

Weak-dollar Tailwind. Nearly half of Sprinklr’s revenue comes from outside the U.S. A weaker dollar means foreign earnings translate into higher reported USD revenue.

Clean Balance Sheet. Sprinklr holds enough cash to cover nearly all liabilities. In uncertain rate environments, financial flexibility matters.

Backblaze: Cons

NRR is slipping. NRR fell from 123% in December 2024 to 106% by the end of 2025. That’s still healthy, but the slowdown signals intensifying competition.

Note: Net retention rate (NRR) shows how much the company’s existing customers are spending compared to last year. 100% NRR means no change, less than 100% means customers are shrinking or leaving, and more than 100% means customers are expanding their spending.

Backblaze competes against giants. Its direct competitors include the three largest cloud platforms in the world — Amazon, Alphabet, and Microsoft — all with extremely deep pockets. Competing with players of that scale requires heavy spending on infrastructure and innovation.

It’s still losing money. Management expects to reach net profitability within the next two years, but that timeline is not set in stone. A lot can change in two years — especially in software, where sentiment can shift quickly. Investors may grow increasingly impatient with loss-making companies if AI disruption narratives intensify and capital rotates toward firms with stronger balance sheets and visible cash flow.

Competitive pressure could also force Backblaze to overspend. When you’re competing with the “Big Three” — Microsoft, Amazon, and Alphabet — you don’t get to operate casually. These companies have enormous balance sheets, deep engineering teams, and the ability to lower prices strategically to defend market share. For a smaller player like Backblaze, staying relevant may require continuous investment in infrastructure, security, performance optimization, and new features.

Sprinklr: Cons

The “real” P/E is higher. On the surface, Sprinklr trades at 12.98x annual earnings. That sounds inexpensive for a software company. But the underlying picture is more nuanced. Over the past 12 months, operating income was roughly $54 million. On top of that, the company recorded about $7.6 million in one-time non-operating income and a substantial one-time tax benefit of $51 million. If you strip out those non-recurring items and focus on normalized profitability, the effective P/E rises closer to 25x. That’s not excessive by software standards, but it’s far less of a bargain than the headline number suggests. For investors already nervous about AI risk in the sector, that higher multiple could dampen enthusiasm.

AI vulnerability. Management emphasizes AI features within the platform — and that’s encouraging — but the core business model sits closer to the disruption front line than Backblaze’s.

First, customers increasingly have the tools to build their own AI-driven agents to handle tasks like customer service routing, automated replies, and sentiment analysis. These tools are becoming cheaper, more flexible, and easier to deploy.

Second, larger enterprise vendors with much deeper pockets — Adobe, Microsoft, ServiceNow, Salesforce — are embedding AI copilots, automated workflows, and intelligent summaries directly into their ecosystem. Many of Sprinklr’s customers already use those broader platforms. As those vendors expand functionality, Sprinklr faces rising competitive pressure from companies with far greater scale.

We’re already seeing some margin compression at Sprinklr. It’s unclear whether the pressure stems from customers experimenting with cheaper AI alternatives or from Sprinklr itself ramping up spending to remain competitive in AI development. Either scenario weighs on near-term profitability. If clients migrate toward lower-cost AI-driven solutions, revenue expansion could slow. If Sprinklr invests aggressively to defend its position, margins could narrow further.

Verdict

Our reference anchor for both stocks is their IPO pricing.

Backblaze. The stock was priced at $16 at IPO, almost four times its current level. From here, we see two paths:

We expect the stock to reach $5.30 within the next 16 months, a 31.5% gain.

If it survives and achieves sustained profitability within the next two years, an 11% CAGR over 12 years is plausible.

Sprinklr. Also priced at $16 at IPO — almost three times today’s price.

We think it can rebound to $7.50 within two years, a 34.5% gain.

That said, we’re less confident in Sprinklr’s long-term durability. AI progress could eventually compress the value of middle-layer customer-management platforms. Over the next two years, however, AI tools remain imperfect — and that gives Sprinklr time.