Trump vs. Europe: A Bull Case for U.S. Pharma

Unlocked Edition #3

Today we’re putting forward a policy-driven, moderately speculative idea: buy selected U.S. pharma stocks — specifically those with meaningful exposure to European sales — to profit from the likely outcome of ongoing U.S.–EU drug price negotiations.

You’re reading a free weekly idea. Want 1–3 ideas every Tuesday plus access to 40+ live ideas? Consider becoming a paid subscriber. Already a subscriber? Enjoy the new Unlocked Edition at no additional cost.

The Basis of the Idea

A major policy standoff is unfolding between Washington and several European capitals over the future of prescription drug pricing.

One underappreciated reality is that U.S. patients and insurers often pay materially more — roughly 35–45% more — for the same medicines than consumers in other advanced economies. The structural reason isn’t mysterious. Many countries operate national or quasi-national healthcare systems that centralize purchasing power, giving governments substantial leverage to negotiate lower drug prices.

The U.S., by contrast, runs on a fragmented system of private insurers, pharmacy benefit managers, and government programs. That fragmentation disperses bargaining power and generally results in higher list and net prices. Roughly 42% of Americans receive coverage through government-subsidized programs, about 50% through employer-sponsored plans, and roughly 8% remain uninsured. With no single dominant negotiator representing the entire system, pharmaceutical companies have more pricing flexibility domestically.

President Trump’s stated objective is to rebalance this dynamic by pressuring U.S. trading partners to pay more for pharmaceuticals, arguing that if prices rise abroad, it becomes politically and economically easier for U.S. prices to moderate at home. Early signs suggest the strategy may be gaining traction through hard-nosed negotiations, with tariffs reportedly used as leverage. The UK has already signaled willingness to adjust pricing on certain medicines, and similar discussions are underway elsewhere.

If this pattern broadens — and we believe it will, given that the EU has recently conceded ground to Trump on several economic fronts — the implications could be constructive for U.S. pharmaceutical revenues. Overseas markets could reprice upward faster than the U.S. market reprices downward.

Even incremental pricing concessions from large European buyers — particularly France and Germany — could quickly translate into bullish sentiment for the sector. It wouldn’t take much to move shares: a credible negotiation breakthrough could lift U.S. pharma stocks by mid-single to low-double digits in a single session at the sector level, with individual names potentially moving more.

Meanwhile, without a broad U.S. negotiation mechanism, many pharmaceutical companies may not feel compelled to cut domestic prices aggressively or quickly. In fact, they may not even lower them at all — there are limits to what any presidential administration can directly impose. That dynamic could allow earnings to outperform expectations for several quarters.

Our approach is straightforward: select U.S. pharma companies with significant European revenue exposure, add a thematic ETF for broader participation, and position ahead of potential negotiation progress. We believe Trump will extract concessions from EU partners on this issue.

Issuers

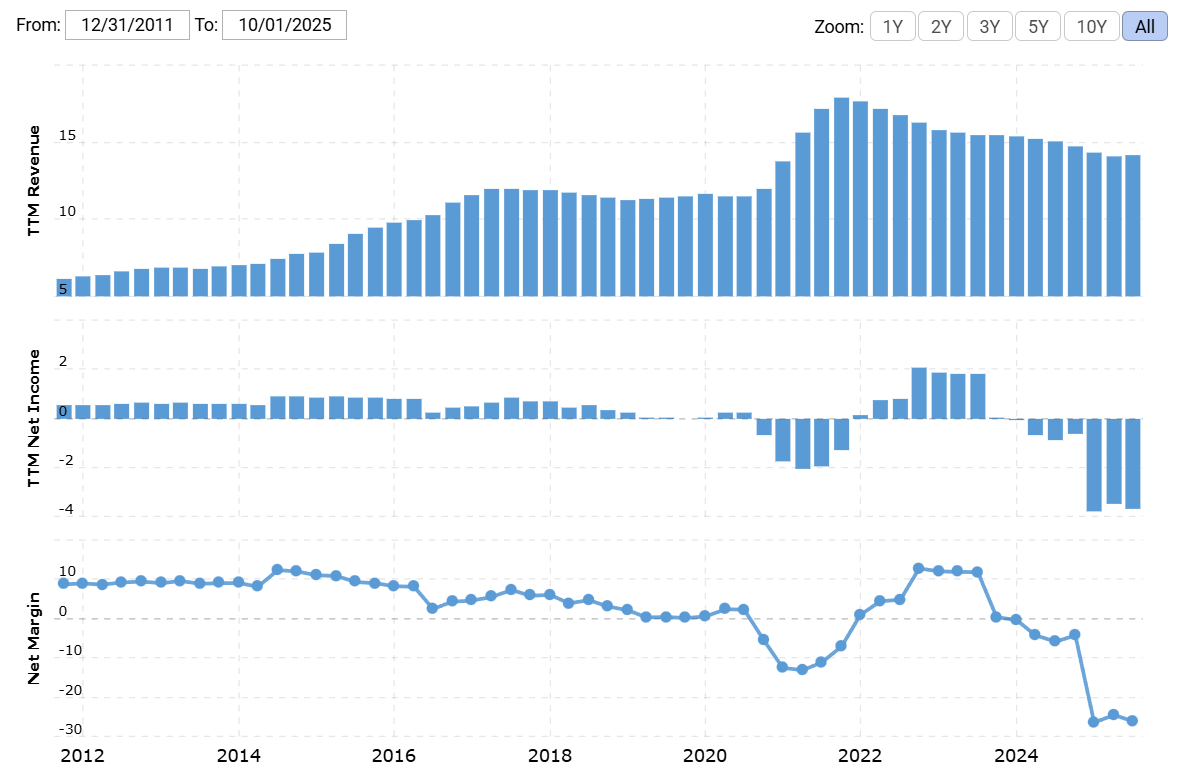

Viatris (NASDAQ: VTRS)

Market cap: $18.37 billion

P/S: 1.29

P/E: —

Dividend yield: 3.08% ($0.48 per share a year)

Sales by region: Developed markets (mostly Europe) 37.4%, U.S. 23.38%, emerging markets 15.32%, China 13.01%, Japan-Australia-New Zealand 9.16%.

Profitability: The company is currently reporting losses. For the 12 months ending October 1, 2025, gross margin was 35.97%, operating margin negative 18.76% and net margin negative 26.13%.

Special note: Recent losses were largely driven by non-operating items — asset impairments, litigation settlements, and substantial non-cash charges tied to acquisition amortization.

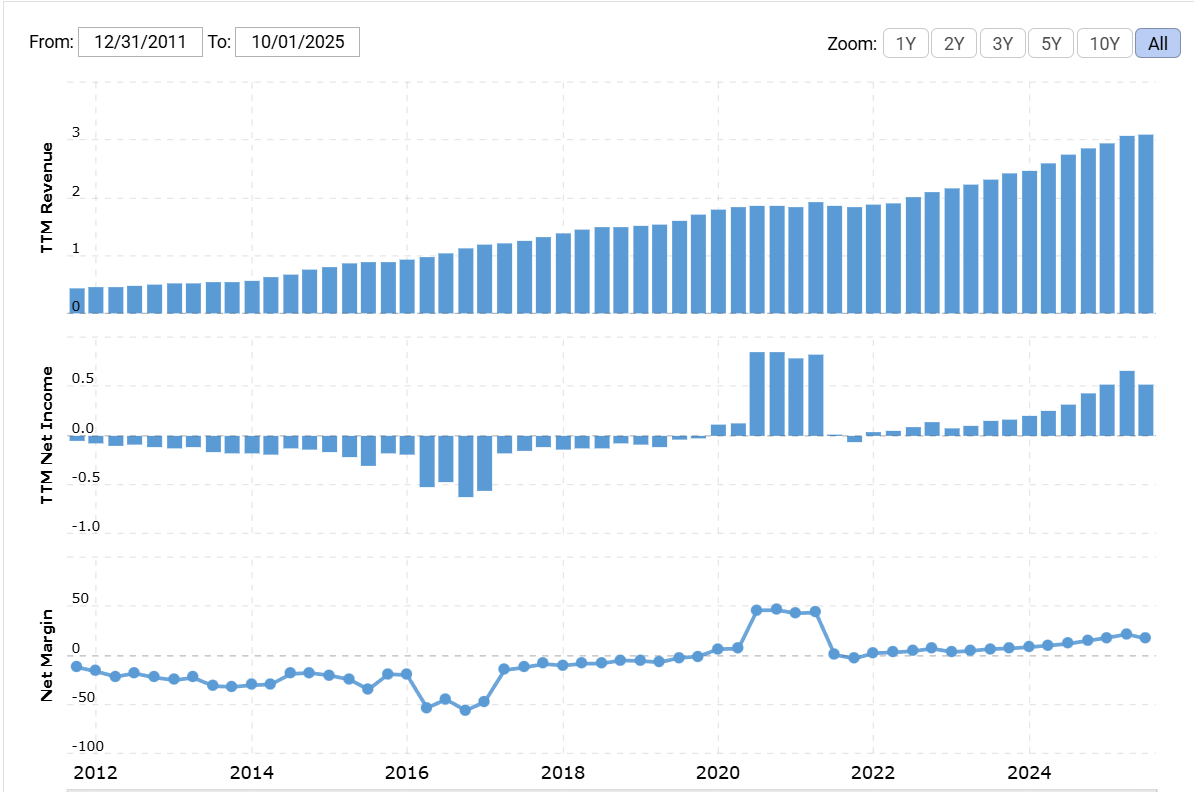

BioMarin Pharmaceutical (NASDAQ: BMRN)

Market cap: $11.46 billion

P/S: 3.6

P/E: 21.66

Dividend yield: —

Sales by region: U.S. 32.92%, Europe 29.51%, Latin America 13.46%, rest of the world 17.57%.

Profitability: BioMarin is operationally profitable. For the of 12 months ending October 1, 2025, gross margin was 79.56%, operating margin was 19.89%, and net margin was 16.82%.

iShares U.S. Pharmaceuticals ETF (NYSEArca: IHE) — A thematic ETF holding U.S.-listed pharma stocks. Most of its holdings generate less than 18% of sales in Europe, which technically weakens its fit under our “high European exposure” filter. However, if there is a credible breakthrough in the U.S.–EU drug-pricing negotiations, investors are unlikely to split hairs. Capital typically flows broadly into anything associated with U.S. drugmakers — sector ETFs included.

Expected Profits

Viatris: 31.5% profit in 16 months

BioMarin: 25.5% profit in 16 months

iShares U.S. Pharmaceuticals ETF: 22% profit in 16 months

Pros

Weak Dollar. Both BioMarin and Viatris generate more than 65% of revenue outside the U.S. A weakening dollar acts as a tailwind: stronger foreign currencies translate into higher reported USD revenue when earnings are converted back. Simple currency math.

This benefit is less pronounced for the ETF’s holdings, since many generate a larger share of revenue domestically.

Stocks Off Their Highs. Viatris trades at nearly one-third of its 2018 valuation, and BioMarin sits roughly 50% below its 2020 peak. That creates room for a rebound. The reasons for their declines are fairly typical in pharma — R&D disappointments, regulatory setbacks. In our view, currency tailwinds and negotiation-driven optimism could outweigh those negatives.

Rotation Out of Software. Capital flowing out of AI-sensitive software stocks needs a new home. Pharma qualifies as “real economy” business — labs, molecules, patents — not code vulnerable to disruption narratives. AI can accelerate drug discovery, but it can’t yet replace the economics of patent-protected therapies. As AI anxiety drives software volatility, pharma could attract defensive and rotational flows.

Dividend Yield. Viatris offers a yield above U.S. and developed-market averages, which adds a layer of income support.

Moderate Chances of M&A. Both companies have reasonable valuations and manageable market caps, making them plausible acquisition targets for larger pharma players.

Cons

Pharma’s Achilles Heel. Drugmakers operate under a built-in expiration date: patents. In the U.S., effective exclusivity typically lasts around 13 years post-launch. Once it expires, generics enter at dramatically lower prices.

When that happens, revenue erosion usually follows. Consumers rarely choose the higher-priced branded option when a cheaper equivalent exists. Ironically, Viatris itself generates about 37% of revenue from generics — a factor contributing to its margin compression.

This reality forces pharma companies into a perpetual R&D race. Drug development is expensive, slow (often seven years or more), and uncertain. Roughly 90% of compounds entering clinical trials fail. The estimated average cost of developing a successful drug is around $2.8 billion.

To stay competitive, companies often acquire late-stage biotech firms — sometimes at eye-watering prices. Roche’s $3.5 billion acquisition of 89bio is one example. These bets can pay off — but they can also miss.

Both Viatris and BioMarin could pursue expensive R&D acquisitions, which may or may not generate shareholder value.

Viatris Balance Sheet. Viatris carries $22.7 billion in liabilities, with $7.36 billion due by September 2026. The dividend could face pressure if debt servicing takes priority.

BioMarin’s balance sheet is significantly stronger, with enough cash to cover most obligations. The iShares ETF, of course, avoids single-name balance-sheet risk.

Political Volatility. Pharma remains a perennial political target. While healthcare costs are heavily influenced by intermediaries who add limited clinical value, drugmakers are the most visible scapegoats. Expect headline-driven volatility.

That said, diversified exposure through the iShares ETF reduces single-company risk — even if the sector broadly reacts to policy rhetoric.

Verdict

We expect material progress in the U.S.–EU drug-price negotiations within the next 16 months, setting our investment horizon.

Viatris: Buy at $15.95. Target $21 in 16 months — a 31.5% gain, excluding dividends.

BioMarin: Buy at $59.66. Target $75 in 17 months — 25.5% gain.

iShares U.S. Pharmaceuticals ETF: Buy at $89.97. Target $110 in 16 months — a 22% gain.

This is a policy-driven trade. If negotiations advance as expected, sentiment could shift quickly — and in markets, sentiment shifts are often half the battle.