The Qorvo–Skyworks Chip-Merger Bet

Unlocked Edition #13. May 2026

Today’s idea sits at the intersection of a coming microcontroller shortage and a pending semiconductor merger — two independent catalysts for the same pair of stocks. We’re buying Qorvo and Skyworks Solutions before their deal closes, and we think the trade works whether or not it does.

Why We Picked Some Stocks — and Ignored Others

Several well-known microcontroller names didn’t make the cut, and it’s worth explaining why.

Some are simply too expensive. Companies like Microchip Technology, Texas Instruments, and Infineon trade at P/S multiples above 5. We’ve already recommended our share of richly valued ideas, and we’re being more disciplined this time — a microcontroller shortage alone isn’t likely to drive enough earnings growth to justify even higher multiples.

Others fall outside our current coverage universe. Names like ABOV Semiconductor and ELAN Microelectronics trade on exchanges we aren’t focusing on at this stage — for now, we’re limiting our coverage to the U.S., the U.K., major European markets, and Japan.

Issuers

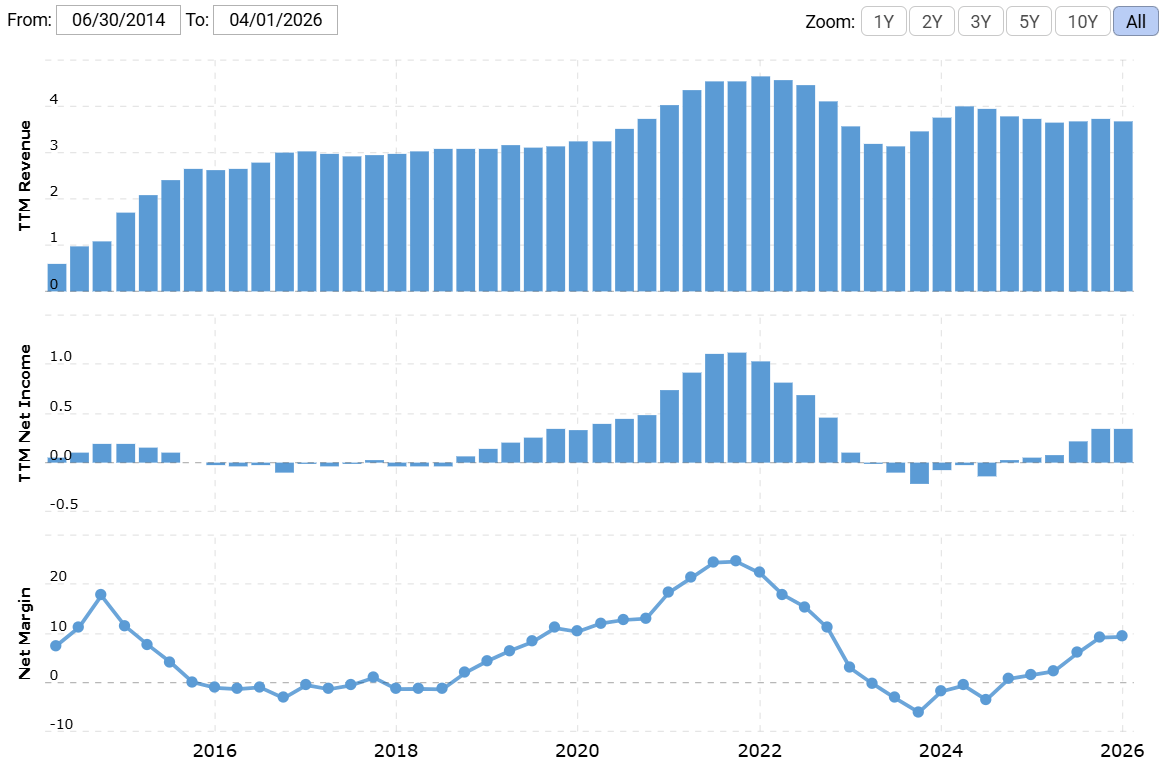

Qorvo (NASDAQ: QRVO) — American semiconductor company that supplies RF components to Apple and other major electronics manufacturers, with business prospects closely tied to how those key customers perform.

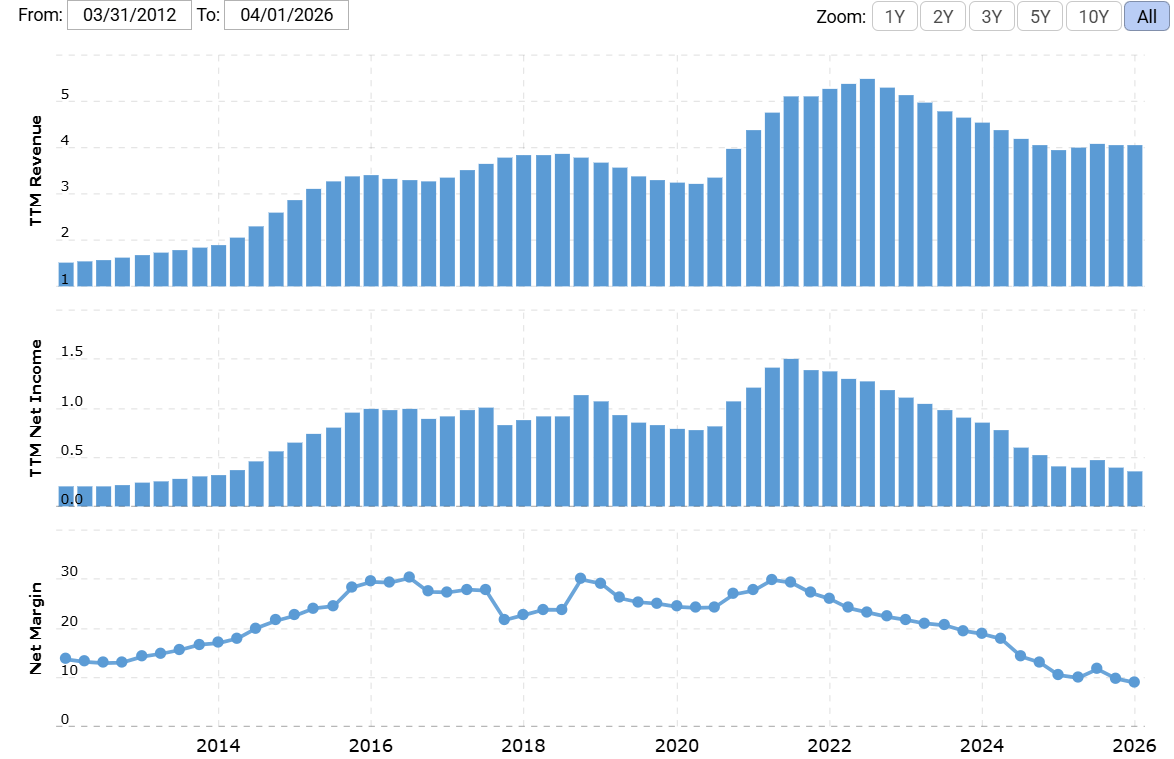

Skyworks Solutions (NASDAQ: SWKS) — American semiconductor company manufacturing sophisticated electronic components, including diodes, amplifiers, antenna-tuning systems, circulators, isolators, and data filters.

Expected Profits

If the deal closes: 21% profit in 16 months, excluding dividends; 12% CAGR over 10 years, including dividends

If the deal doesn’t close — Qorvo: 20% profit in 2 years, excluding dividends; 8% CAGR over 10 years, including dividends

If the deal doesn’t close — Skyworks: 16.5% profit in 2 years, excluding dividends; 8% CAGR over 10 years, including dividends

Description of the Business

Qorvo. According to the company’s 2025 annual report, revenue is structured as follows:

Advanced Cellular Group (ACG) — 69.35%. RF solutions for smartphones, wearables, laptops, and tablets.

Segment operating margin: 26.2%.High Performance Analog (HPA) — 19.18%. Radio-frequency chips and power-management solutions for infrastructure, defense and aerospace, and automotive power.

Segment operating margin: 26.8%Connectivity and Sensors Group (CSG) — 11.46%. Connectivity and sensor components and systems. Segment operating margin: -10% (loss-making).

By geography: U.S. — 62.95%, Mainland China — 12.91%, other Asian countries — 11.74%, Taiwan — 9.73%, Europe — 2.67%.

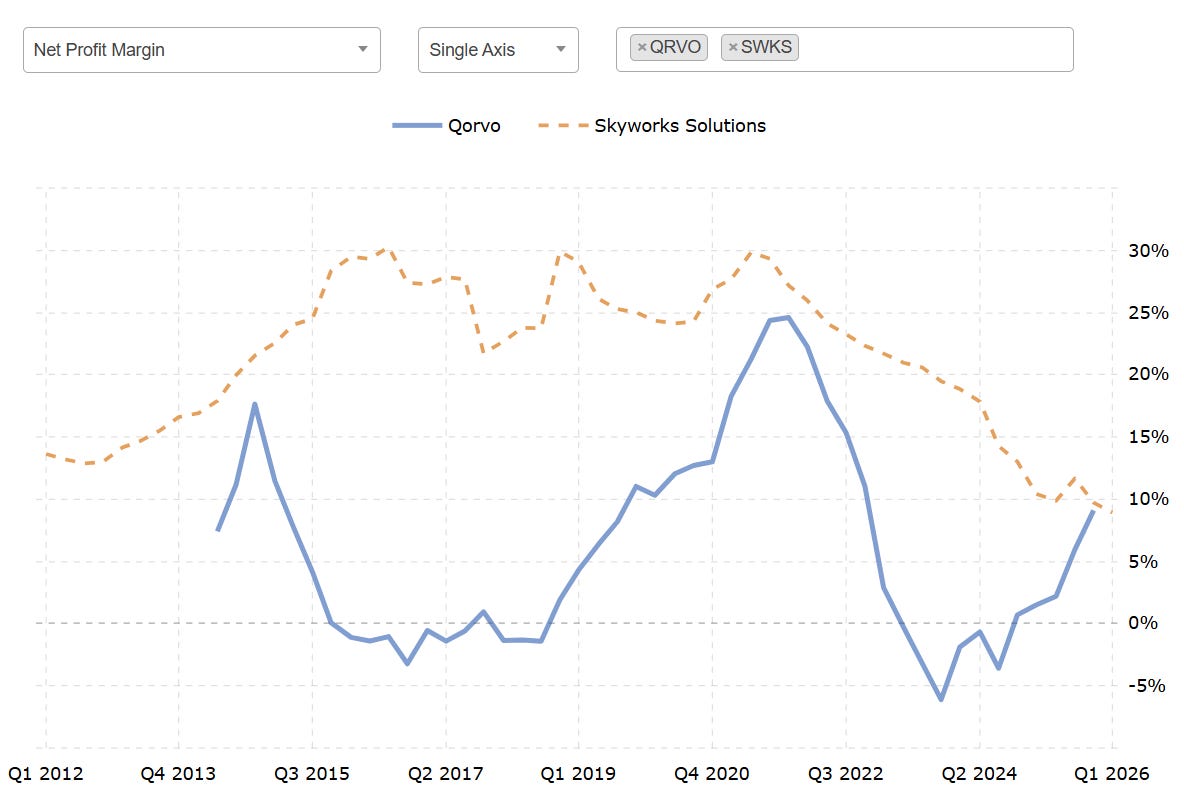

Qorvo is profitable. For the 12-month period ended March 31, 2026: gross margin — 48.59%, operating margin — 11.18%, net margin — 9.22%.

Skyworks Solutions. The company’s 2025 annual report doesn’t provide a segment breakdown.

By geography: U.S. — 77.25%. Taiwan — 6.34%, Mainland China — 6.22%, South Korea — 4.65%, other countries — 5.54%.

Skyworks is profitable. For the 12-month period ended March 31, 2026: gross margin — 41.07%, operating margin — 9.09%, net margin — 8.93%.

What to Keep in Mind: The Companies Are Merging

Both companies have announced plans to merge, with the deal expected to close in early 2027. Under the agreed terms, each Qorvo share will be exchanged for $32.50 in cash plus 0.960 shares of Skyworks. Upon closing, Skyworks shareholders are expected to own about 63% of the combined company, with Qorvo shareholders holding the remaining 37%.

We think buying both stocks now — ahead of the close — makes sense for a couple of reasons.

The combined company should benefit from greater pricing power and improved margins over time — upside that hasn’t been priced in yet. And if the deal falls apart entirely, we’re still left holding two high-quality semiconductor businesses with room to recover.

Pros

MCU Tailwind. Neither Qorvo nor Skyworks has a large direct exposure to the microcontroller market — Qorvo’s Arm Cortex-M4 platform is one of the more notable exceptions. But that’s not the point. We expect the MCU segment to tighten in 2026–2027, driven by rising automotive demand (one of the largest MCU end markets) and raw-material disruptions in the Middle East — helium supply in particular. Even if the rest of the semiconductor market stays broadly balanced, incremental price strength in MCUs would provide a meaningful earnings tailwind for both companies: MCU is not the biggest part of their business, but demand for it is expected to rise rapidly, which would strengthen overall financial performance (the rest of the semiconductor market will grow too, albeit at a lower pace).

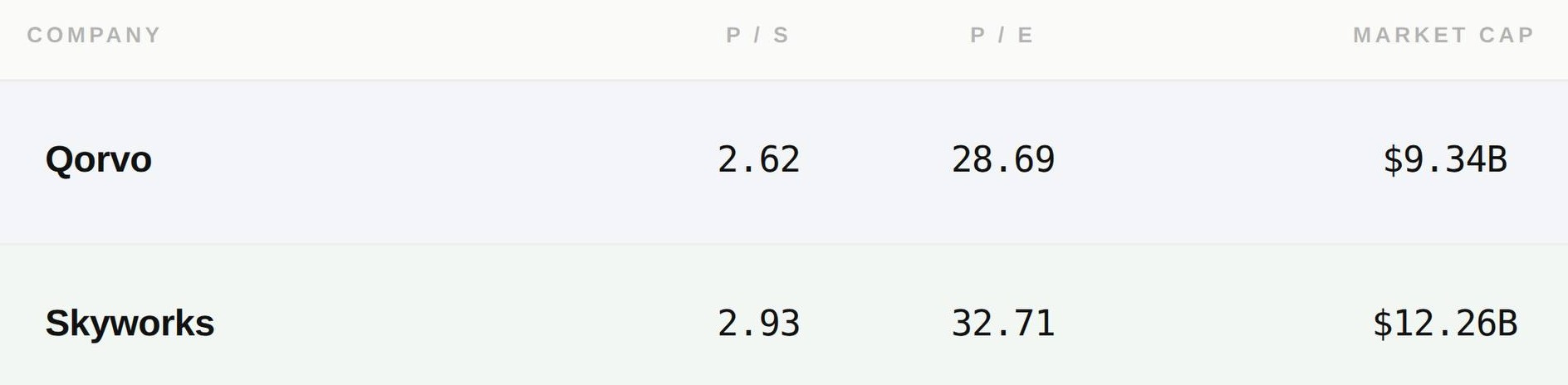

Cheap Enough. Relative to most semiconductor names, Qorvo and Skyworks are modestly priced — on both valuation multiples (both stocks have P/S ratios south of 4 and P/E ratios lower than 45) and market cap (combined company value would be below $30 billion). That’s not a trivial point in a sector where many peers trade at multiples that already assume perfection.

Asset Premium. The combined company would have a larger manufacturing footprint in regions well removed from China — the U.S. and Mexico in particular. In an environment of persistent U.S.–China trade friction, that geographic positioning could justify a valuation premium for the merged entity that neither company commands on its own today.

Dividend. Skyworks pays $2.81 per share annually — a 3.4% yield that sits well above both U.S. and global market averages. Yields at that level attract a different class of investors: income-focused holders who provide a natural floor under the share price and don’t disappear at the first sign of volatility.

Cons

Smartphone Dependence. Both companies thrived during peak 5G adoption — a period when RF content per smartphone was rising, handset volumes were strong, and factories ran at high utilization. Then the cycle turned. Smartphone demand softened, the China and Android markets became less favorable, Apple became an even larger — and therefore riskier — source of revenue concentration, average selling prices declined, inventories had to be worked down, and R&D costs stayed elevated. This is, in large part, the reason the two companies decided to merge in the first place.

Apple Concentration. The customer concentration issue deserves its own entry, because it’s that significant. Qorvo derives roughly 50% of sales from Apple and another 10% from Samsung. Skyworks is even more exposed — 67% of its revenue flows from Apple. The merged company may gain some negotiating leverage through scale, but it would still be highly exposed to any shift in Apple’s sourcing strategy or supply-chain decisions.

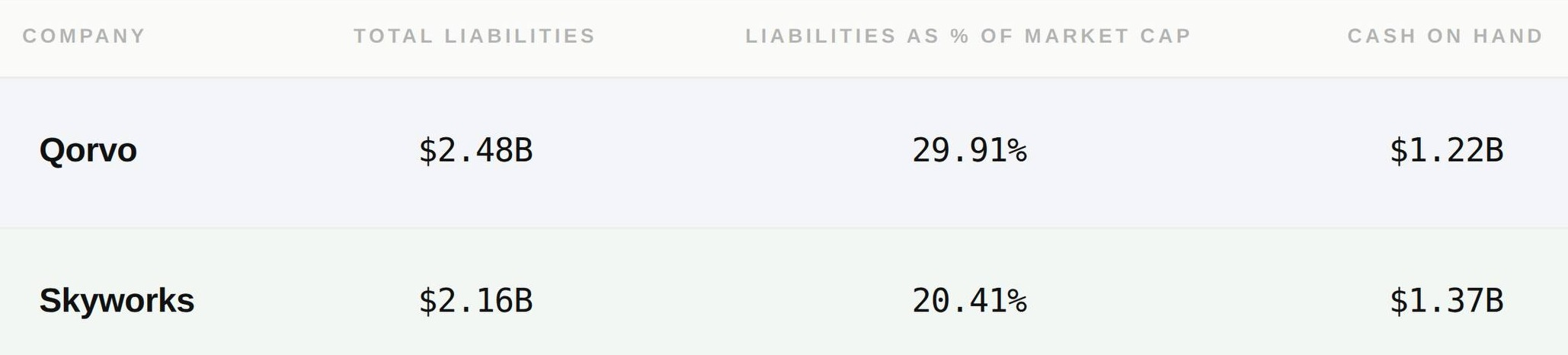

Debt and Payout Risk. Both companies carry moderate debt loads, and for Skyworks the payout ratio adds another layer of risk: the company distributes about 91% of net profit as dividends. If refinancing conditions tighten or management decides to prioritize deleveraging, a dividend cut becomes a real possibility — and cuts at those yield levels tend to leave a mark on the stock.

Weakening Greenback. Both companies generate more than 60% of their sales in the U.S., which means the ongoing decline in the dollar’s purchasing power will not benefit companies (or a combined company going further) the same way as it would benefit outright exporters (those that generate more than 50% of their revenue outside the U.S.). It’s not a crisis — but it’s a missed opportunity worth factoring in.

Verdict

Buy Qorvo at $106.67 and Skyworks at $82.37. The merger is central to the thesis, so here’s how the two scenarios play out:

If the deal closes by September 19, 2027, under the announced terms — each Qorvo share exchanged for $32.50 in cash plus 0.960 Skyworks shares (currently worth $80), you would get a small but low-risk upside on Qorvo (5.46%). If the market assigns synergy credit to the combined company, we think it should trade at no less than $99, representing a 20% premium to Skyworks’ current price. Combined, that’s roughly 21% upside excluding dividends within 16 months. For long-term holders, we expect the position to deliver roughly 12% CAGR over 10 years, including dividends.

If the deal falls apart, both stocks still have room to recover as standalone businesses. At their June 2021 peaks, Qorvo traded around $195 and Skyworks around $191 — a reminder of where these companies have been when the cycle was in their favor.

Short-term: Over a two-year horizon, we think Qorvo can reach $128 (about 20% upside) and Skyworks can reach $96 (roughly 16.5% upside), excluding dividends.

Long-term: Over 10 years, we expect each to generate approximately 8% CAGR, including dividends.