The Infrastructure Giant the Market Forgot to Re-Price

Issue #62. March 2026

This stock hit both short-term targets, and we're opening the issue for all readers. If you want ideas like these before the upside is realized, start you free trial.

Today we’re looking at a company that most investors think they already understand: Nokia. The market still remembers the failed phone empire. What it often forgets is that Nokia (HEL: Nokia) quietly rebuilt itself into a global telecom infrastructure provider and the stock now looks unusually cheap relative to that business. That’s why we think shares of the Finnish network-equipment giant Nokia are worth a closer look.

Expected Profits

19.2% profit in 15 months;

31.5% profit in 2.5 years;

~381% profit in 15 years (11% CAGR, incl. dividends)

Description of the Business

Nokia is one of the world’s largest telecom infrastructure companies. Its core products include RF systems, base stations, subsea communication cables, radio controllers, and signal transmission systems.

In simple terms, Nokia builds much of the physical and digital infrastructure that keeps modern telecom networks running. The company is also more vertically integrated than many investors realize. Nokia operates its own manufacturing facilities while also working with major electronics manufacturing partners such as Flex, Foxconn, Jabil, Sanmina, and Fabrinet.

According to the company’s 2025 annual report, revenue is distributed across four main segments:

Network Infrastructure — 40.12%. Products and services that keep connectivity running, from data centers to fiber-optic cables.

Operating margin: 9.8%.Mobile Networks — 39.22%. Communications equipment and services covering everything from legacy 2G networks to modern 5G systems.

Operating margin: 2.8%.Cloud and Network Services — 13.1%. Software and services that allow operators to deploy and monetize cloud-based telecom infrastructure.

Operating margin: 13.0%.Nokia Technologies — 7.55%. Nokia’s technology licensing business, built on more than 150 years of innovation. This unit collects royalty income from Nokia’s massive patent portfolio — and, unsurprisingly, it’s the most profitable part of the company.

Operating margin: 70.6%.

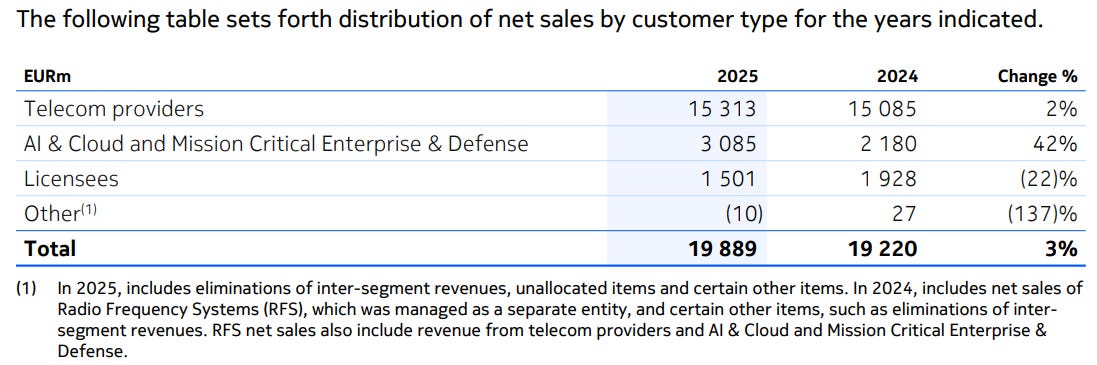

Most of Nokia’s revenue — roughly 75% — comes from telecom providers. However, demand from defense customers and AI-related infrastructure projects has been growing quickly.

Geographically, the United States is Nokia’s single biggest market, accounting for 29.52% of revenue. Europe comes next at 19.44%. India contributes 15.4%, while Finland itself accounts for 8.12%. The rest comes from other global markets.

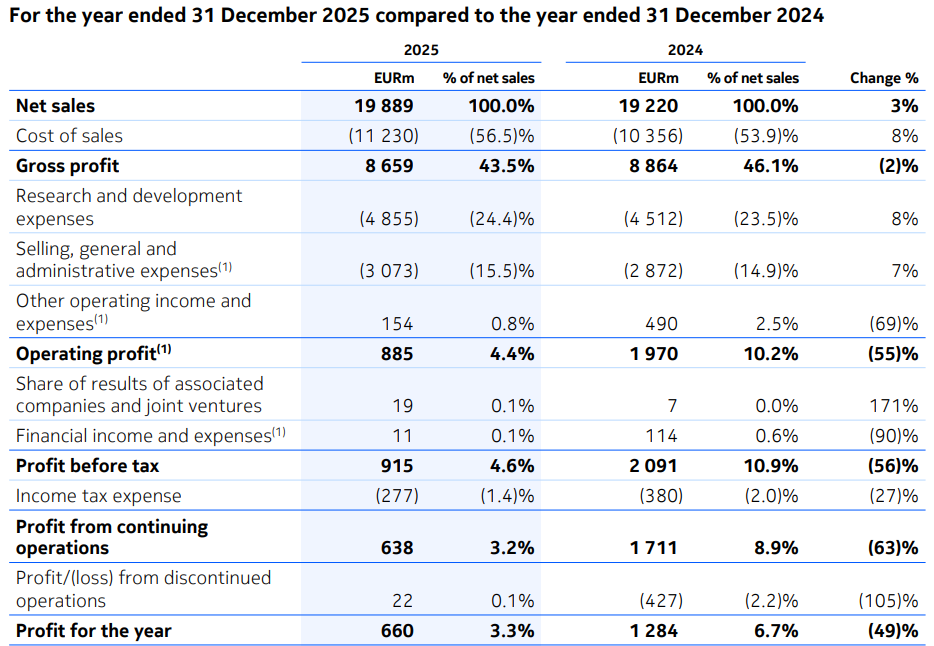

Importantly, Nokia is a profitable business. In 2025 the company reported a gross margin of 43.5%, an operating margin of 4.4%, and a net margin of 3.3%.

Pros

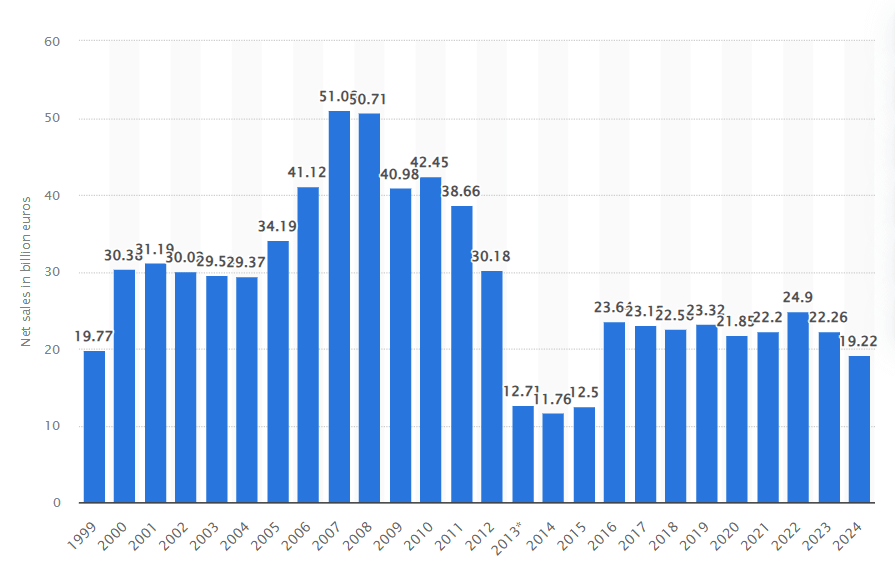

The Stock Has Been Depressed for Years — Perhaps Too Long. Nokia’s share price is still roughly four times lower than its 2007 peak. Much of that decline reflects lingering negative sentiment after the company lost its once-dominant mobile-phone business. But that historical narrative can obscure the current economics. In 2007, Nokia generated roughly €51 billion in revenue at the peak of its handset empire. That revenue later collapsed as smartphones reshaped the industry.

Fast-forward to today: Nokia’s 2025 revenue is about 2.5x lower than that peak. If revenue is roughly 2.5x smaller, you might expect the company’s market value to be perhaps 2.5–3x lower than it was back then. Instead, the stock trades about 4x lower. That discrepancy suggests the market may still be pricing Nokia based on an outdated narrative rather than its current business.

Relatively Cheap. Nokia’s market cap sits at about €37.47 billion, which is modest for a global telecom infrastructure provider. The stock trades at roughly 1.89x P/S — hardly expensive for a company that supplies critical infrastructure to telecom networks around the world. That valuation alone could make the stock attractive to investors.

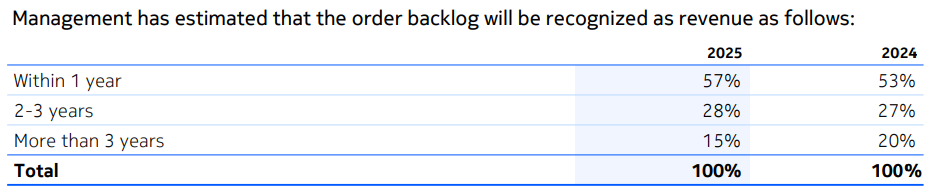

Telecom Infrastructure Behaves a Lot Like Utilities. Technically speaking, telecom companies aren’t utilities like electricity or water providers. In practice, they behave similarly. Connectivity has become essential infrastructure for the modern economy. Few businesses — or individuals — can realistically operate “offline.” As a result, telecom operators tend to plan network investments years in advance, often through long procurement cycles and multi-year contracts. For Nokia, that means a large portion of its revenue is relatively predictable. An increasing share of that demand is now tied to AI infrastructure as well. Data centers and cloud providers require faster networks and higher-capacity fiber connections — exactly the type of equipment Nokia specializes in. Taken together, these factors make Nokia closer to a stable infrastructure supplier than a volatile consumer-tech company.

Diversified Customer Base. Another advantage is Nokia’s customer diversification. No single client accounts for more than 10% of revenue. That spreads risk across dozens of telecom operators and reduces the impact of any one customer cutting back on spending.

A Potential “War-Proof” Premium. Recent geopolitical tensions in the Middle East have reminded investors how quickly conflict can disrupt global supply chains. Most of Nokia’s critical assets are located in the United States and Europe — regions far removed from active conflict zones. If investors begin assigning higher valuations to companies whose operations are geographically insulated from geopolitical disruptions, Nokia could benefit from that shift in sentiment.

Possible Spin-Offs. Nokia today operates several relatively distinct business units. Network infrastructure, mobile networks, cloud services, and the licensing division each function with a fair degree of independence. Because of that structure, it wouldn’t be surprising to see Nokia eventually spin off certain divisions into separate publicly traded companies — an event that could unlock additional shareholder value.

Cons

Dividend Could Be Reduced. Nokia currently pays €0.14 per share annually, which implies a dividend yield of about 2.1%. However, the company’s profits have been somewhat unstable. In strong years the payout ratio might sit around 60%, while in weaker years it can become stretched.

2025 was not particularly strong — Nokia earned roughly €0.11 per share. That means the dividend already exceeds earnings, which makes a reduction — or at least a partial cut — a realistic possibility. If that happens, dividend-focused investors could exit the stock, putting short-term pressure on the share price.

Oil Supply Disruptions. The war in Iran has sent shockwaves through global energy markets, pushing oil and gas prices higher. That could create cost pressure for Nokia, particularly in manufacturing and logistics. It’s unclear how much of those costs Nokia can pass on to customers. If telecom operators resist higher prices, Nokia may end up absorbing a meaningful portion of the increase.

Currency Effects. Nokia’s business is deeply global, which means foreign-exchange movements can materially affect reported results. Because Nokia reports its financials in euros, a stronger euro reduces the value of revenue generated abroad when it is converted back into the company’s reporting currency. The Euro Currency Index rose roughly 7% over the past year, which has already weighed on Nokia’s reported earnings — and could continue to do so if the trend persists.

Profitability Could Remain Volatile. Nokia’s management is currently investing heavily in areas such as optical networking, data-center connectivity, and AI-related infrastructure. Strategically, that investment makes sense. But it also means margins could remain uneven while the company builds out these new growth areas.

P/E Looks High (For Now). Because earnings fluctuate, Nokia’s P/E ratio currently appears elevated — around 60x. That headline number could scare off some investors, even though it largely reflects temporarily depressed earnings rather than excessive valuation.

Verdict

Buy now at €7.3. From there, we see three possible outcomes:

Base case: the stock reaches €8.70 within roughly 15 months, implying a 19.2% gain (excluding dividends).

Upside case: the shares could climb to €9.60 over about 2.5 years, representing a 31.5% gain (excluding dividends).

Long-term case: hold Nokia for 15 years and target ~11% CAGR (including dividends).