The Case for Ubisoft’s Bounce-Back

Unlocked Edition #1

You’re reading a free weekly idea. Want 1–3 ideas every Tuesday plus access to 40+ live ideas? Consider becoming a paid subscriber. Already a subscriber? Enjoy the new Unlocked Edition at no additional cost.

Today we have one of the most speculative ideas we’ve ever published: buying shares of the deeply distressed French video game publisher Ubisoft Entertainment (Euronext Paris: UBI). The company is hovering uncomfortably close to the edge of bankruptcy — but precisely because of that, we think it may soon attract an outside investor or acquirer willing to step in.

Expected Profits

17% profit in 15 months;

49% profit in 3 years;

10% CAGR profit over 10 years.

Description of the Business

Ubisoft is a video game publisher and developer founded in 1986. Over nearly four decades, it has built some of the industry’s most recognizable franchises, including Far Cry, Assassin’s Creed, and others. This intellectual property portfolio remains Ubisoft’s single most valuable asset — and arguably the main reason the company is still standing today.

According to Ubisoft’s 2024 annual report, revenue is split as follows:

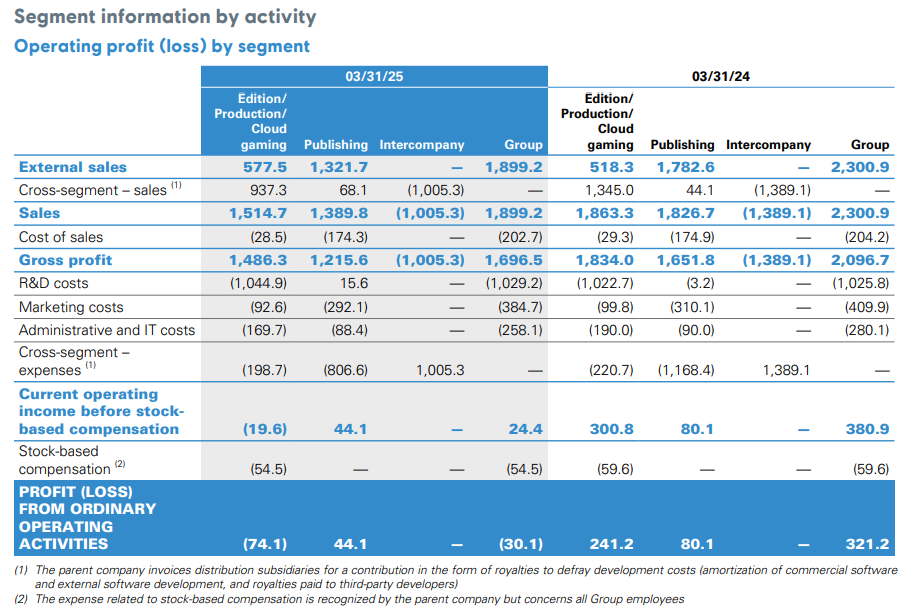

Edition / Production / Cloud Gaming — 30.41%. This segment covers game development and the related online infrastructure required to support modern titles, including servers and low-latency networks. Conceptually, this is the IP ownership and franchise-control side of the business. A large portion of segment revenue is intercompany: Ubisoft’s publishing entities pay “royalties” to this division to help offset development costs.

Publishing — 69.59%. These entities handle global sales, distribution, and local marketing of Ubisoft’s games.

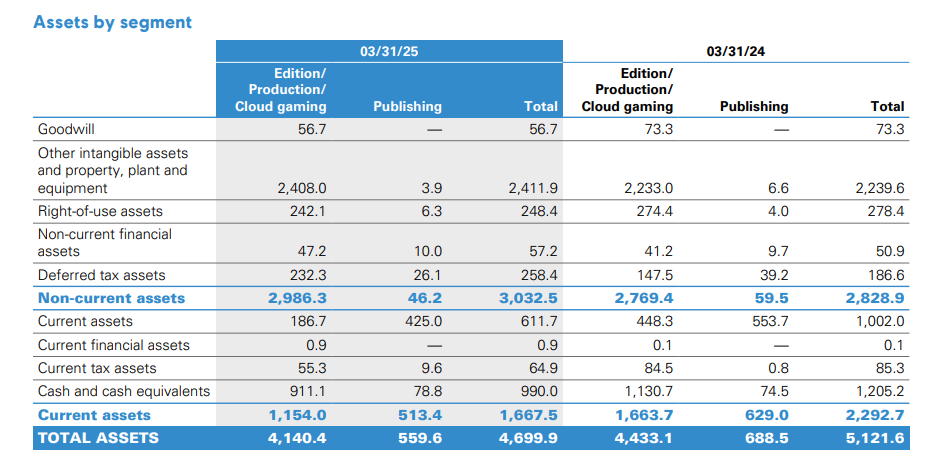

Speaking frankly, this structure is messy and not especially helpful for investors. A significant share of reported revenue is effectively Ubisoft billing itself, which makes it harder to assess true operating margins. Shareholders would likely benefit more from a cleaner breakdown — by franchise, content type, or lifecycle stage. It’s also telling that most of Ubisoft’s assets are concentrated in the Edition division.

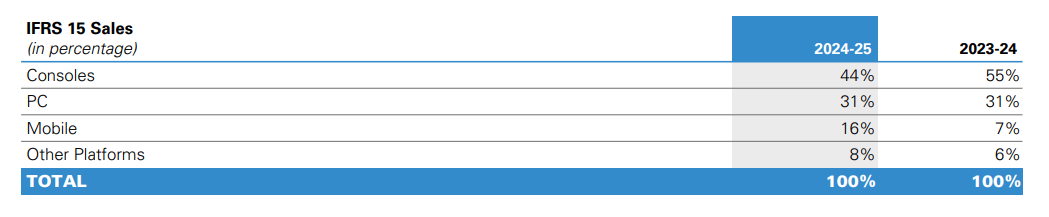

Most of Ubisoft’s sales are now generated online. Consoles account for the largest share at 44%, followed by a still-significant PC contribution of 31%.

Financially, Ubisoft is currently loss-making. For the 12-month period ending September 30, 2025, the company reported a gross margin of 57.14%, an operating margin of 5.82%, and a net margin of -3.86%.

By region, sales are split as follows: North America accounts for 45.63%, Europe for 32.11%, and the rest of the world for 22.26%.

Why the Stock Fell So Much

Over the past decade, Ubisoft has lost roughly 95% of its market value. That kind of collapse doesn’t happen overnight — and it deserves some historical context.

Ubisoft was once regarded as a craft-driven studio with strong creative credentials. In the 1990s and early 2000s, titles such as Prince of Persia and Beyond Good & Evil were critically acclaimed, even when commercial success was uneven. Financially, those years were mixed but manageable: profits fluctuated, debt remained under control, and the business survived.

The inflection point came around 2009, following the success of Assassin’s Creed II. Ubisoft developed a highly scalable open-world formula — large maps, sandbox mechanics, and repeatable design patterns — and applied it across multiple franchises, including Far Cry and Ghost Recon. For a time, this worked. Revenues grew steadily.

But costs grew too. Game development became more expensive across the industry, and Ubisoft’s margins failed to improve meaningfully. Debt increased alongside revenue, and profitability remained erratic: some strong years, some deeply unprofitable ones.

By late 2024, the cracks were impossible to ignore. Gamers showed clear fatigue with Ubisoft’s formulaic output, while financial performance remained underwhelming. In December 2024, GamesIndustry.biz published a 2025 forecast suggesting Ubisoft faced a stark choice: go private or sell itself after years of creative and financial missteps. We found that assessment convincing — and still do.

The forecast quickly proved prescient. In January 2026, Ubisoft announced delays to numerous long-awaited titles and outright cancellations of several high-profile projects, including the Prince of Persia: The Sands of Time remake. The market reaction was brutal. Ubisoft now expects a €1 billion operating loss in fiscal year 2025–2026, driven largely by a one-time €650 million write-down tied to restructuring.

At this point, Ubisoft looks uncomfortably close to bankruptcy. Yet paradoxically, that’s also what makes the stock interesting. Distress often forces change — and that’s where our thesis begins.

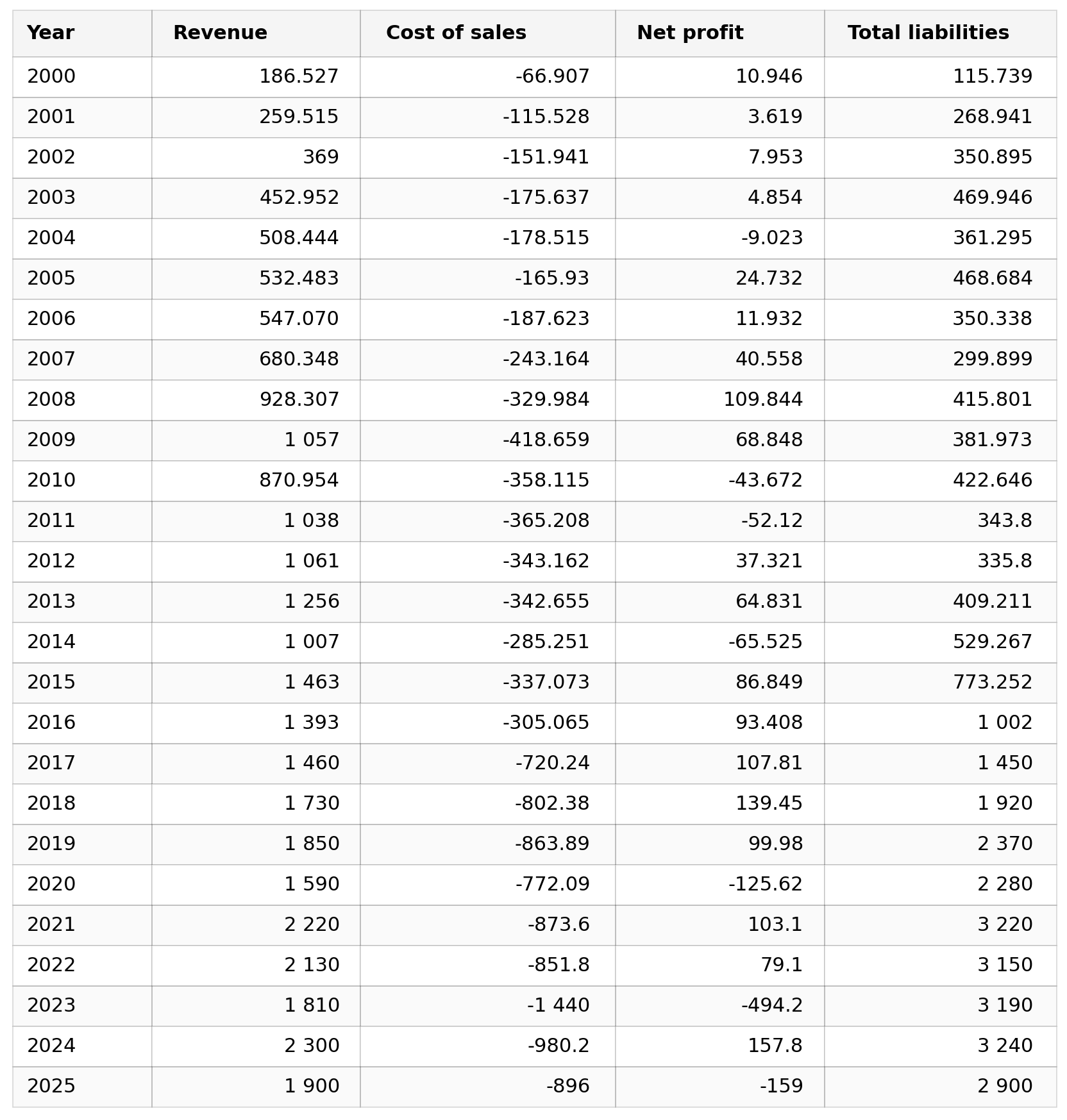

UBISOFT results for every financial year ending March 31, in millions of EUR

Pros

Spin-Off Potential. In 2025, Ubisoft created a new subsidiary focused on its most valuable franchises — Assassin’s Creed, Far Cry, and Rainbow Six — with Tencent investing €1.16 billion for a 25% economic stake. The unit, Ubisoft Nova SAS (branded “Vantage Studios”), remains fully owned within Ubisoft’s structure and is not publicly listed. However, a future spin-off is conceivable. If that happens, existing Ubisoft shareholders would receive shares in the new entity — and investor enthusiasm alone could drive a sharp revaluation, given the quality of the underlying IP.

Ubisoft also looks extraordinarily cheap. Its P/S ratio sits at just 0.28, and the entire company is valued at roughly €546 million. We believe Ubisoft’s IP portfolio alone is worth at least €2 billion. That gap suggests substantial upside if the market begins pricing the assets more rationally.

M&A Optionality. Ubisoft’s management has alienated much of its gamer base over the years, so we don’t expect retail enthusiasm to drive the stock. But from a strategic perspective, the company looks like a bargain. For context, Electronic Arts was acquired for $55 billion at a roughly 25% premium, implying a P/S of 7 and a P/E of 50 at the time. Even a similar premium applied to Ubisoft today would still leave the buyer paying a modest price.

We can’t predict who might buy Ubisoft — or when — but the current valuation is almost an invitation. Potential suitors could range from Tencent to other international investors, including Chinese or Middle Eastern capital. Ubisoft is a globally recognized name that could now be acquired for a fraction of its historical value.

The Activist Angle. The Guillemot family, which co-founded Ubisoft in 1986, still occupies key leadership roles. Whether they deserve full blame for the company’s decline is debatable, but many shareholders clearly think change is overdue. This opens the door for an activist campaign demanding new leadership and strategic direction. Despite France’s relatively management-friendly corporate laws, the Guillemots control only about 15% of the shares (and roughly 20% of the votes). That’s not a blocking stake — meaning pressure could work. Tencent, already a strategic partner, could even be the catalyst.

Cons

The Debt Situation Is Severe. In November 2027, Ubisoft must repay a €675 million bond. Given the company’s current condition, refinancing or repayment is far from guaranteed. Investor concern is already visible in the bond market: in January, Ubisoft bonds due in 2031 fell to 73.8 cents on the euro, near record lows.

Overall, Ubisoft carries €2.9 billion in liabilities — nearly six times its market cap. That’s alarming. Short-term liquidity is somewhat better: €990.2 million is due by September 2026, and the company holds nearly the same amount in cash. Still, the margin for error is thin.

We’re Also Skeptical About Internal Reform. Ubisoft has announced layoffs and a new operating structure aimed at streamlining development, but the same management team that led the company into this mess remains in charge. That doesn’t inspire confidence.

Analysts agree. Cantor Fitzgerald’s Edward James noted that delaying seven games and canceling six “is massive” and suggests management lacks control over the development cycle. TD Cowen’s Doug Creutz expressed doubts that the reorg would fix long-standing execution problems. TP ICAP’s Corentin Marty went further, arguing that a return to sustainable cash generation looks unlikely in the near term.

Ultimately, much of our thesis rests on outside intervention — an acquirer, activist investor, or value-focused buyer stepping in to force change. That’s plausible, but it doesn’t leave much credit for current management. Still, there is a longer-term scenario where Ubisoft survives, executes its reorganization, and eventually splits into smaller, franchise-focused companies. That outcome could unlock value and lead to outperformance versus today’s bloated structure.

Verdict

Buy now at €4.70. From here, several paths are possible:

Speculative catalysts such as M&A talks or major partnership announcements could lift the stock to €5.50 within 15 months, implying a 17% profit.

If Ubisoft survives the next three years and shows tangible improvement from its reorganization, shares could reach €7.00 — a 49% profit.

There’s also a slimmer long-term scenario where Ubisoft remains independent for the next decade and delivers roughly 10% CAGR.

Note: If Ubisoft spins off a subsidiary and the new stock outperforms the parent, we would consider that a successful outcome.