The Case for a Lyft Rebound

Unlocked Edition #6. March 2026

Today’s idea is a classic “fallen tech stock” setup: buy shares of the U.S. ride-hailing app Lyft (NASDAQ: LYFT) after its steep decline. We expect a bounce in the share price because the stock now looks undervalued relative to its position in the market.

You’re reading a free weekly idea. Want 1–3 ideas every Tuesday plus access to 40+ live ideas? Consider becoming a paid subscriber. Already a subscriber? Enjoy the new Unlocked Edition at no additional cost.

Expected Profits

29% profit in 17 months;

60% profit in 3 years

Description of the Business

Lyft is a ride-hailing app that connects drivers with passengers and earns a commission from each ride. Since many of our readers may not be based in the U.S. (and Lyft operates almost entirely there), the simplest way to think about the company is as an Uber-like service operating at a smaller scale.

Lyft’s revenue comes from two segments:

Rideshare Marketplace — 92.73%. The Lyft app matches riders with drivers, and Lyft takes a commission on each ride.

Rental — 7.27%. Car rentals for drivers.

Lyft operates primarily in the United States. Other (unnamed) countries contribute just 0.004% of revenue.

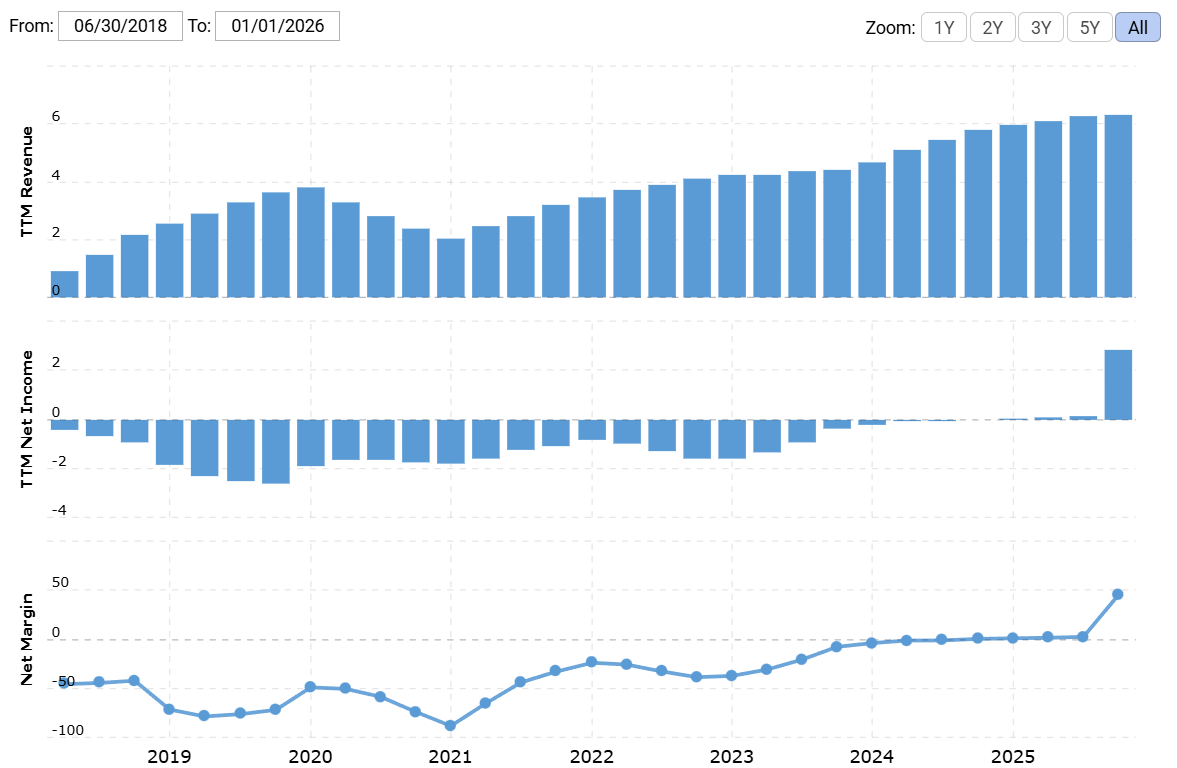

Lyft is still operationally unprofitable, and the company’s headline profitability has mostly come from accounting quirks rather than the underlying business.

In 2025, Lyft reported a gross margin of 41.46%, an operating margin of -2.98%, and an eye-popping net margin of 45.03%. That number looks impressive at first glance — but it’s largely the result of a one-time tax benefit rather than actual operating performance. Strip that out, and Lyft is still firmly in the red.

Why the Stock Is Down

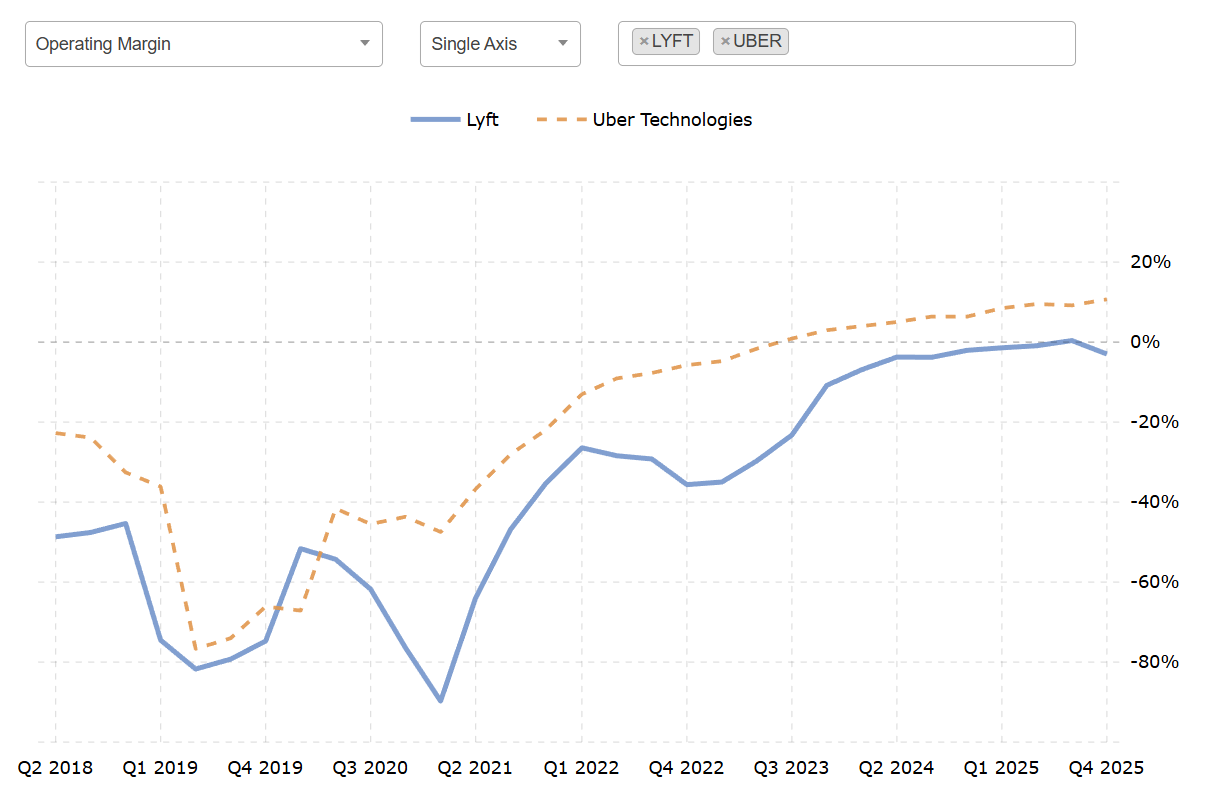

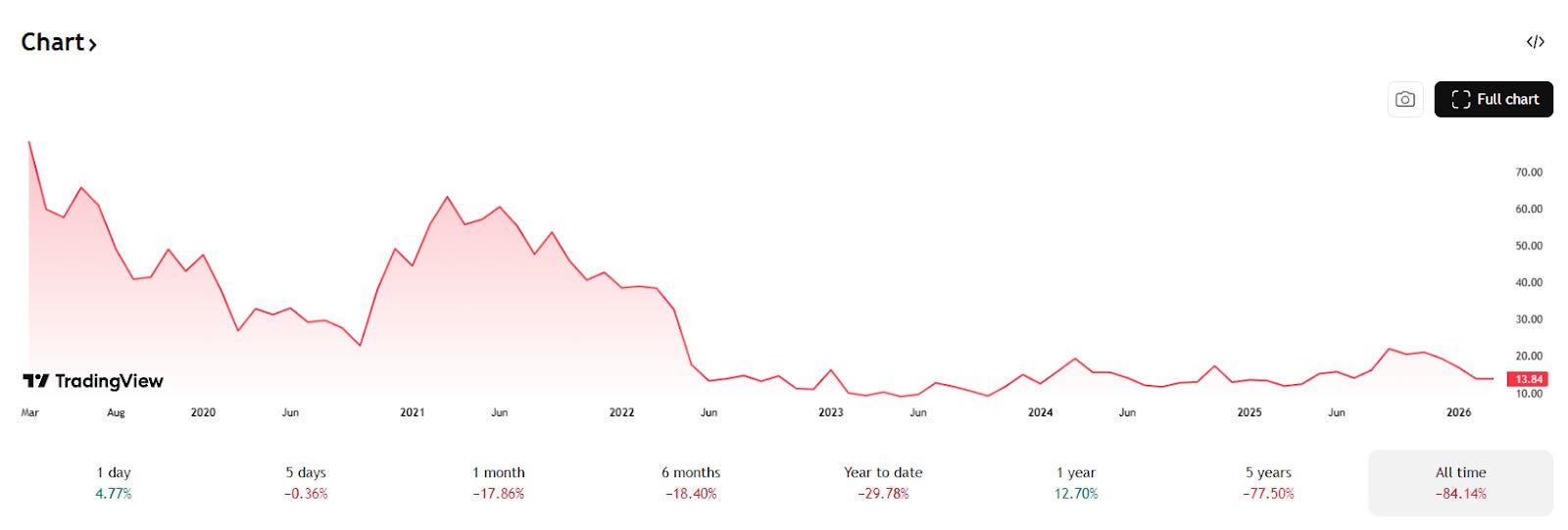

There are plenty of reasons Lyft has lost roughly 84% of its market value since its 2019 IPO: ride-hailing is a brutally low-margin business, competition is intense, growth has slowed, and the company has missed earnings expectations more than once. But the situation can also be summarized in a much simpler way: Lyft has ended up as the “second-place Uber.”

After nearly two decades in the market (Lyft launched in 2007), the company still hasn’t achieved sustained operational profitability. Explaining exactly why would take an entire article, but two structural dynamics are worth highlighting.

First, Lyft has historically built a reputation for treating drivers somewhat better than Uber. Second — and more importantly — it has always operated at a smaller scale. That scale advantage turned out to be critical. Without the same market power, Lyft couldn’t raise prices once it gained customers. Uber, meanwhile, followed the classic platform strategy: compete aggressively on price early, dominate the market, and only then start increasing prices. Unfortunately, Lyft never reached that final stage.

Today, Uber controls close to three-quarters of the U.S. ride-hailing market, while Lyft sits at roughly 24%. That gap matters because Lyft simply doesn’t have the same resources to compete with Uber — either domestically or internationally.

Uber has also expanded aggressively into adjacent businesses such as food delivery and freight brokerage. Lyft, by contrast, remains mostly a ride-hailing intermediary. From a strategic perspective, that leaves Lyft in an awkward position: large enough to matter, but not dominant enough to dictate the market.

Still, we think the stock can bounce — just probably not all the way back to its former highs.

Pros

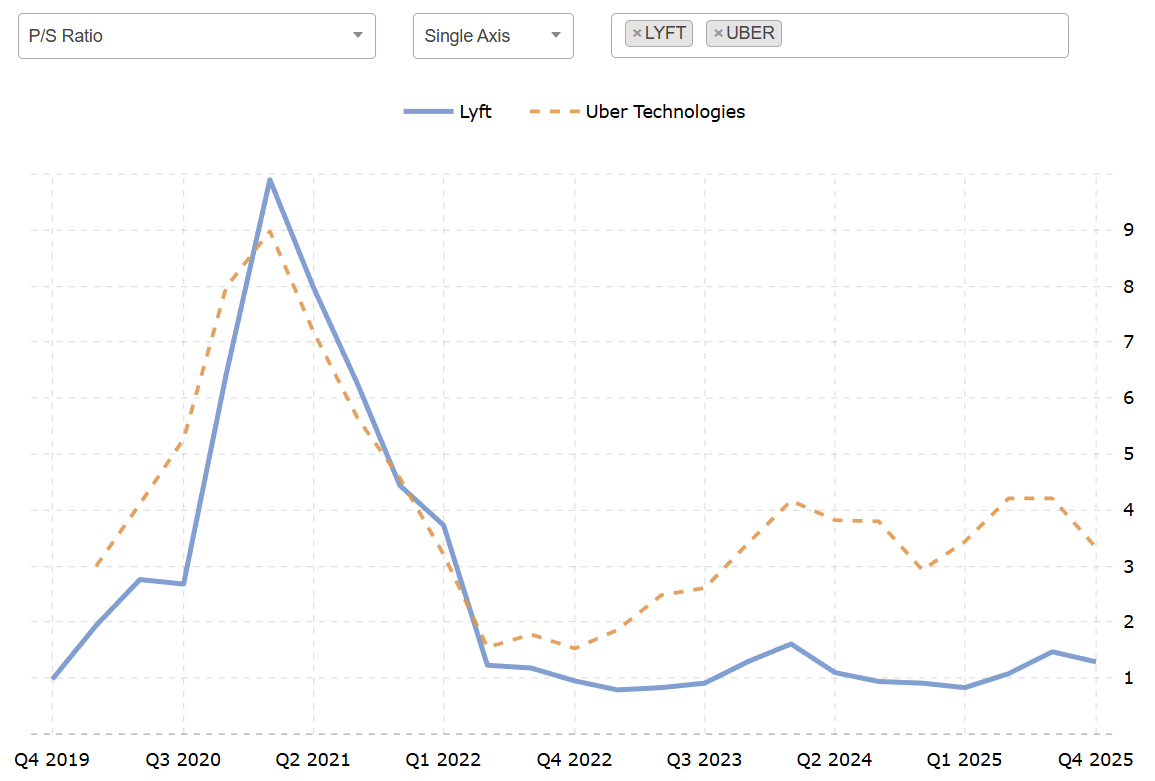

Very Cheap. Lyft currently trades at about 0.88x P/S with a market cap of roughly $5.25 billion. That’s extremely low for a company that still controls nearly a quarter of the U.S. ride-hailing market. At the same time, U.S. retail investors are sitting on unusually large cash balances. If even a portion of that capital rotates back into beaten-down tech names, stocks like Lyft could benefit from simple mean reversion.

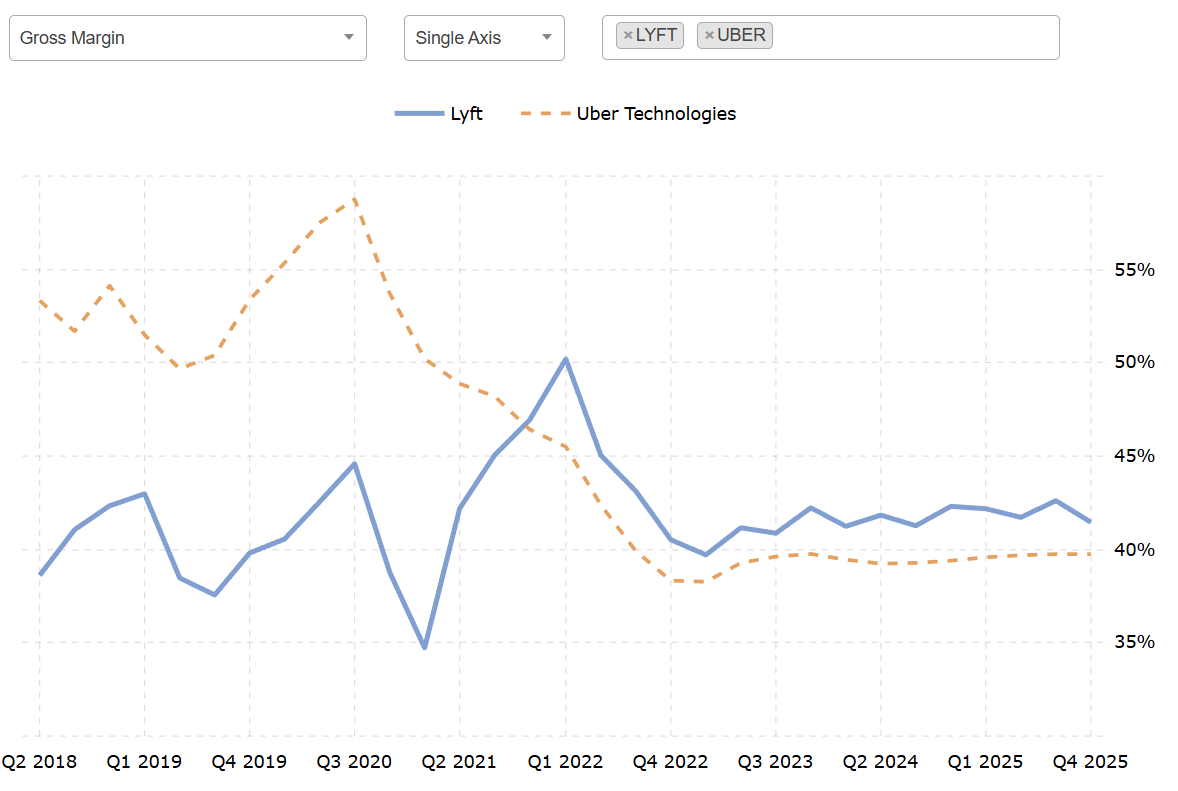

A Credible M&A Story. Lyft actually posts slightly higher gross margins than Uber, while trading at a dramatically lower valuation, both in relative and absolute terms. That valuation gap makes it easy to imagine a private-equity buyer taking a serious look at the company.

Uber could theoretically attempt to acquire Lyft again — it reportedly explored the idea years ago before Lyft rejected it. That said, we’re skeptical regulators would approve such a deal. Buying Lyft would effectively give Uber a near-monopoly in the U.S. ride-hailing market. Even under a more permissive antitrust environment, that would be a very difficult transaction to push through.

A Textbook Activist Setup. Lyft is still far below its 2019 IPO price of $72, making it an obvious candidate for activist involvement.

The timing is also favorable. In August 2025, Lyft eliminated its dual-class share structure — which previously allowed management to outvote other shareholders — and transitioned to a one-share-one-vote system. That opens the door for activist investors to push for changes.

An activist could pursue several levers: pushing for deeper cost cuts, placing a representative on the board, forcing management to present a credible profitability plan, or advocating for a sale of the company. Any of these moves could lift the stock. A coordinated push across several of them could move it even faster.

Cons

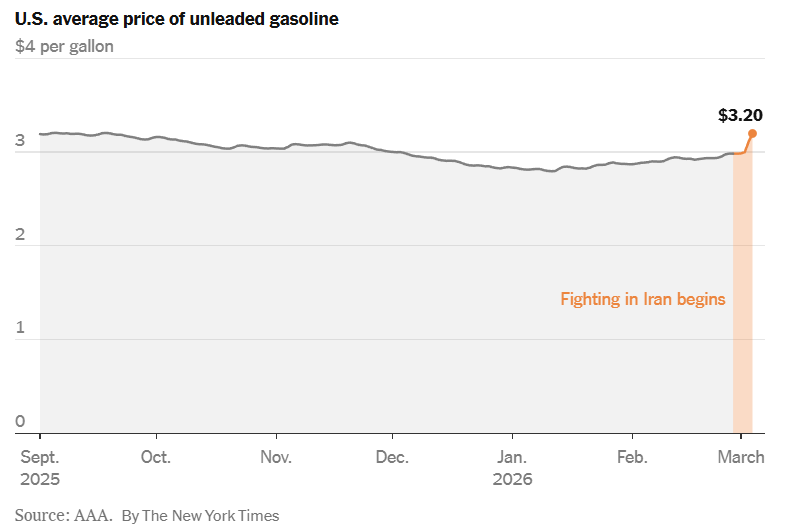

Middle East War. The U.S. war with Iran has pushed global oil prices higher. What happens next largely depends on whether the conflict escalates, particularly if shipping disruptions persist. Gasoline prices, however, have already begun creeping up.

That matters for Lyft because higher fuel costs make driving more expensive for drivers and riders alike. Even small increases in gasoline prices can reduce ride demand at the margin.

The AI Threat Is Real. Lyft may also be unusually exposed to AI-driven disruption. Unlike Uber, it lacks a global footprint and operates almost entirely within the U.S. That concentration creates an interesting risk. If margins continue to tighten, drivers in large metropolitan areas could theoretically “vibe-code” their own ride-hailing platform with lower commissions. That might sound far-fetched, but it’s not entirely unrealistic. Lyft’s revenue is concentrated in dense urban markets where large driver networks already exist. In those cities, drivers could pool capital, build a simpler alternative app, and offer rides at lower commissions. Such a grassroots platform could spread through word of mouth, local communities, and even in-car advertising — gradually chipping away at Lyft’s revenue base.

Still Losing Money. Lyft remains operationally unprofitable, and that’s never an especially comforting feature — regardless of whether the Federal Reserve is cutting rates. At the same time, lending conditions in the U.S. are tightening. Oil-supply risks linked to the Middle East conflict have pushed some lenders to reassess risk, making credit somewhat harder to obtain.

Lyft also carries a substantial liability load of about $5.76 billion — more than its current market cap. Of that amount, $4.53 billion comes due by the end of 2026, while the company currently holds only $1.84 billion in cash. Given that Lyft is still burning money, the balance sheet does introduce a real bankruptcy risk.

Robotaxi Uncertainty. Lyft is also behind Uber in the race toward robotaxis. Even though the company is trying to catch up, it simply doesn’t have the financial firepower to compete with Uber head-to-head in developing autonomous fleets. Lyft could eventually strike a partnership with a robotaxi operator — but that outcome would largely depend on external partners rather than Lyft itself.

In the long run, robotaxis threaten the entire human-driver ride-hailing model — not just Lyft. The timeline will depend heavily on regulatory approvals, but the direction is fairly clear.

And yes, the most accurate depiction of this transition may still be the one from Cyberpunk 2077: the Delamain AI system is introduced to assist human drivers, only to end up replacing them entirely.

Current Market Sentiment. Even without AI disruption, the market simply isn’t very friendly to software companies right now. Investors have been rotating toward asset-heavy businesses — companies tied to infrastructure, commodities, or physical products — on the theory that those businesses are harder for AI to disrupt. That preference could stick around for a while, particularly after a year of disappointing returns for tech stocks.

Verdict

Buy now at $13.18. From there, we see two possible scenarios:

Bounce case: Given the current valuation, a rebound to $17 within the next 17 months looks reasonable. That would be a 29% profit.

Extended case: Over a three-year horizon, the stock could reach $21.10, implying a roughly 60% gain.

That said, we’re hesitant to recommend Lyft as a true long-term holding (unlike many of our other ideas). Over time, lower-commission “vibe-coded” competitors and the rise of robotaxi platforms could eventually make the current business model obsolete.