Strait, Shock, and Three Gushing Barrels

Unlocked Edition #14. June 2026

This issue focuses on a higher-volatility opportunity in U.S. oil: three domestic producers positioned to deliver their most profitable year in recent memory as higher energy prices flow straight to the bottom line.

Issuers

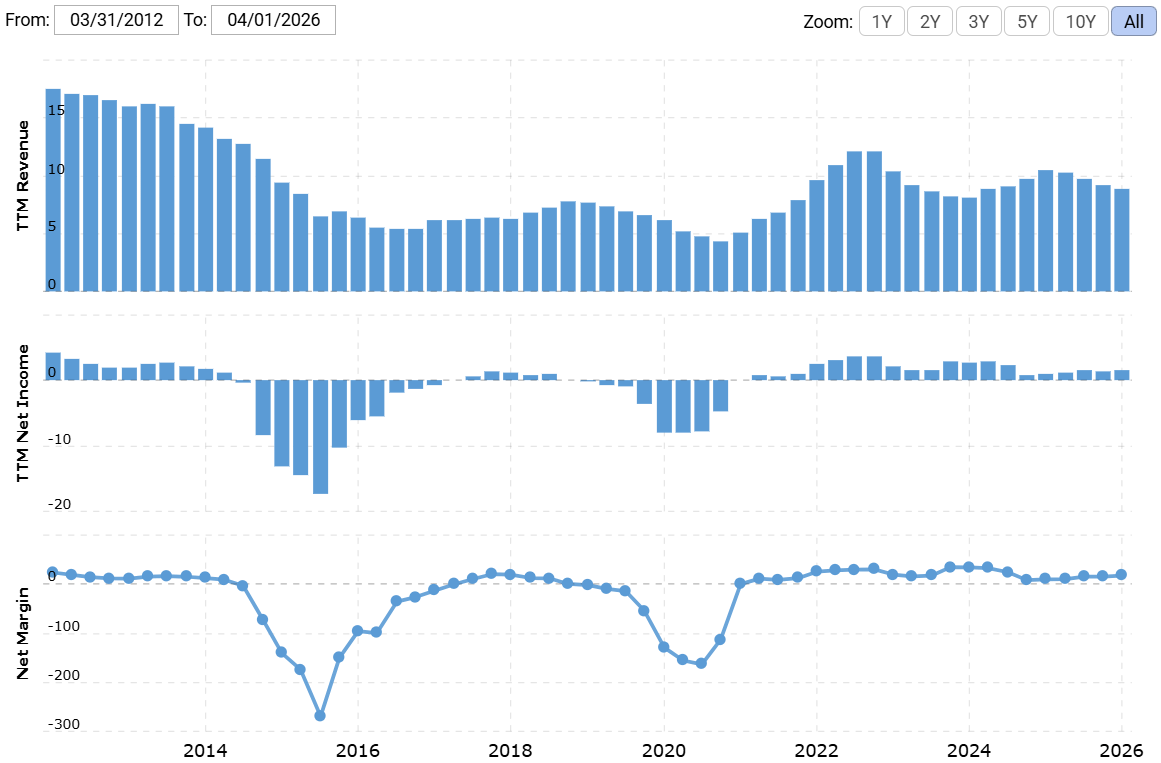

APA Corporation (NASDAQ: APA) is a U.S. oil and gas company with operations across the United States (approximately 52% of revenue), Egypt (approximately 36.48% of revenue), and the United Kingdom.

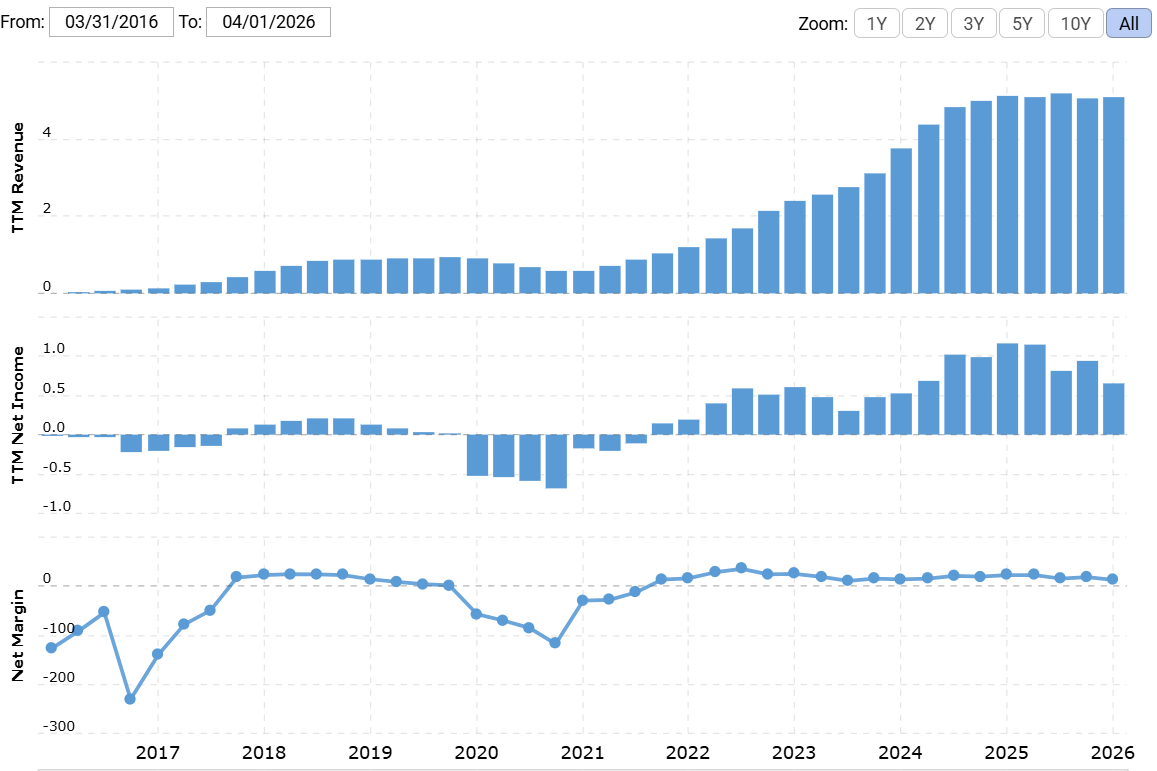

Permian Resources (NYSE: PR) is a U.S. oil company focused on acquiring, optimizing, and developing oil assets in the Delaware Basin.

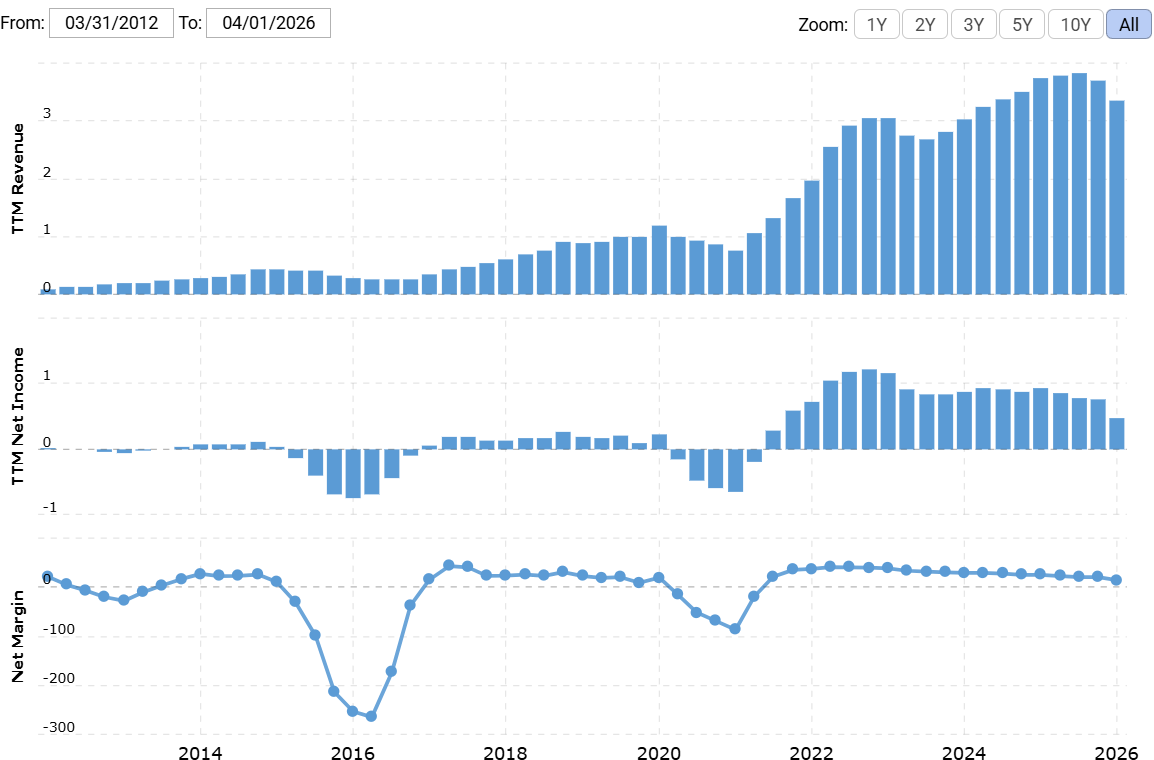

Matador Resources (NYSE: MTDR) is a Texas-based oil and gas company with operations concentrated in the Permian Basin.

Expected Profits

APA Corporation (APA): 23.5% profit in 16 months; 121% profit in 7 years, 12% CAGR, including dividends

Permian Resources (PR): 18.5% profit in 16 months; 108% profit in 7 years, 11% CAGR, including dividends

Matador Resources (MTDR): 20% profit in 16 months; 108% profit in 7 years, 11% CAGR, including dividends

Pros

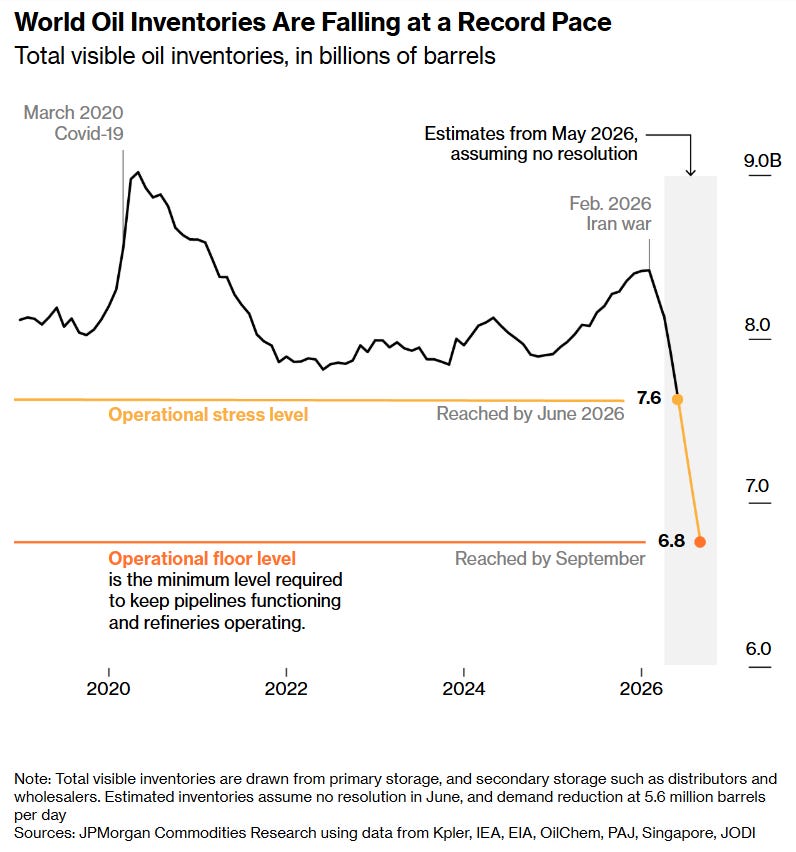

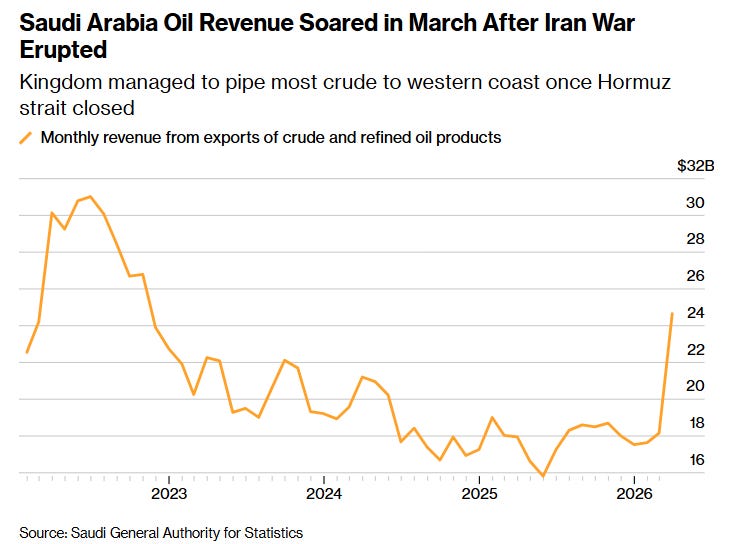

The Oil Shock Has Staying Power. The market’s reaction to the Strait of Hormuz disruption has been, in some respects, surprisingly restrained. Prices have risen significantly, but given that this is the largest oil supply shock in years, the absence of a full-blown spike is almost counterintuitive.

The explanation is strategic reserves: the world’s largest oil consumers released crude from emergency stockpiles to cushion the blow. It worked — temporarily. Those reserves are now being drawn down at a rapid pace, and that buffer won’t last indefinitely.

Even when Persian Gulf output does begin to recover, rebuilding depleted strategic reserves takes time, which implies sustained “replacement” demand for crude and a meaningful floor under prices for months, possibly longer.

The Saudi dynamic adds another wrinkle. The kingdom ships roughly 89% of its oil exports through the Strait of Hormuz and has limited alternative routing capacity. Export volumes fell to around 70% of pre-war levels in March, and yet Saudi Arabia still earned more from oil than it did a year earlier, thanks to the price increase. That arithmetic creates an interesting incentive: major Gulf producers may have little motivation to restore full output if constrained supply continues to support comfortable price levels. For U.S. producers operating entirely outside the Hormuz corridor, this is about as good a setup as the market can offer.

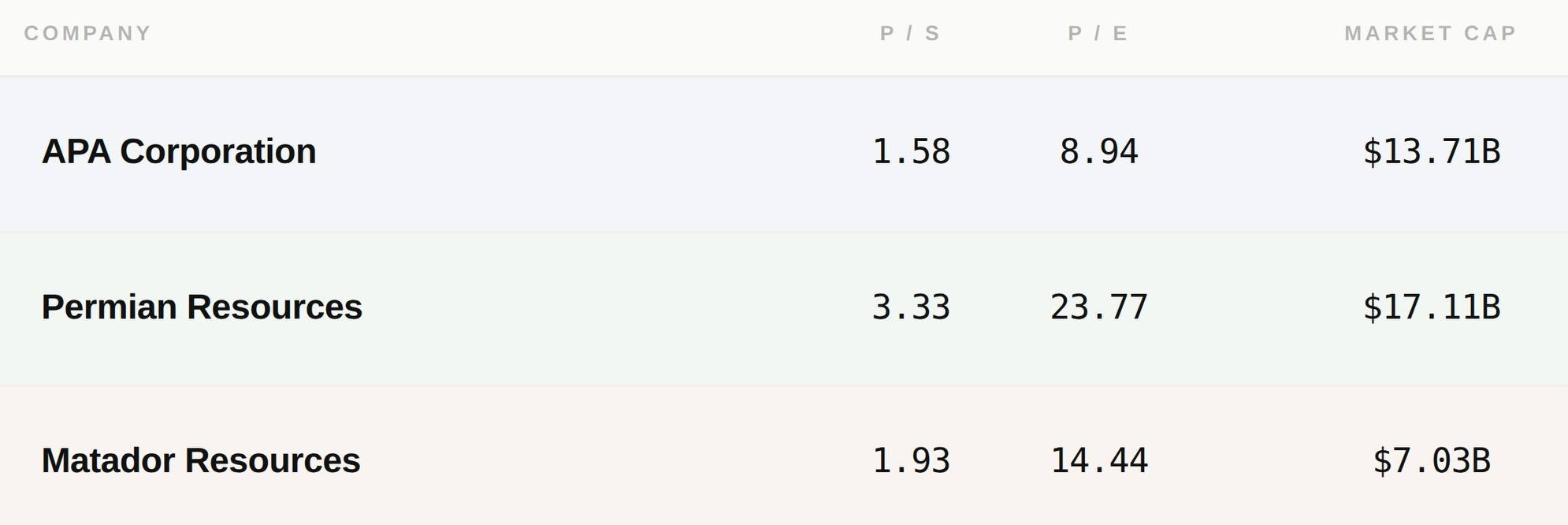

Relatively Cheap. Most of today’s picks trade below the S&P 500 Energy sector’s average valuation and well below the broader market. That combination of low multiples and a favorable pricing environment leaves room for upside without requiring heroic assumptions about where oil goes from here.

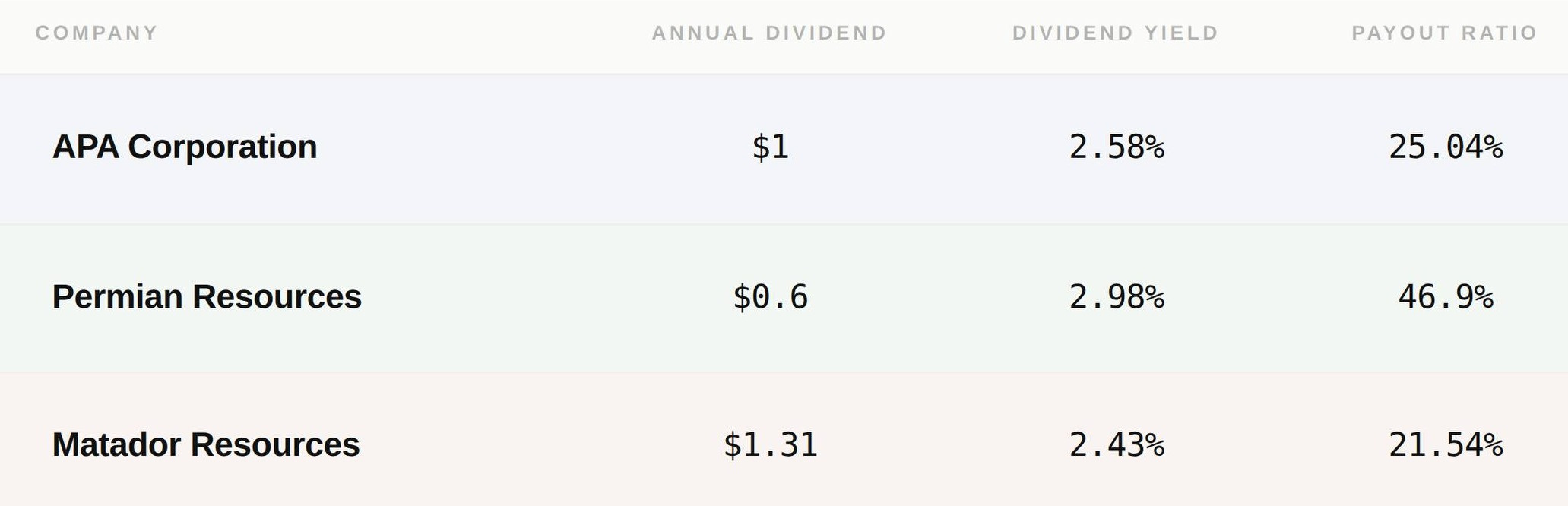

Dividend Potential. All three stocks already yield well above the U.S. market average and all three have payout ratios low enough to support meaningful increases if higher oil prices deliver the earnings windfall we’re expecting. Income-focused investors looking for yield in a high-price energy environment have a habit of rotating into exactly this type of name.

M&A Potential. Cheap valuations, solid profitability, and direct leverage to the current energy environment make all three companies plausible acquisition targets for Big Oil looking to add production, or for private equity hunting yield in a tight market.

Cons

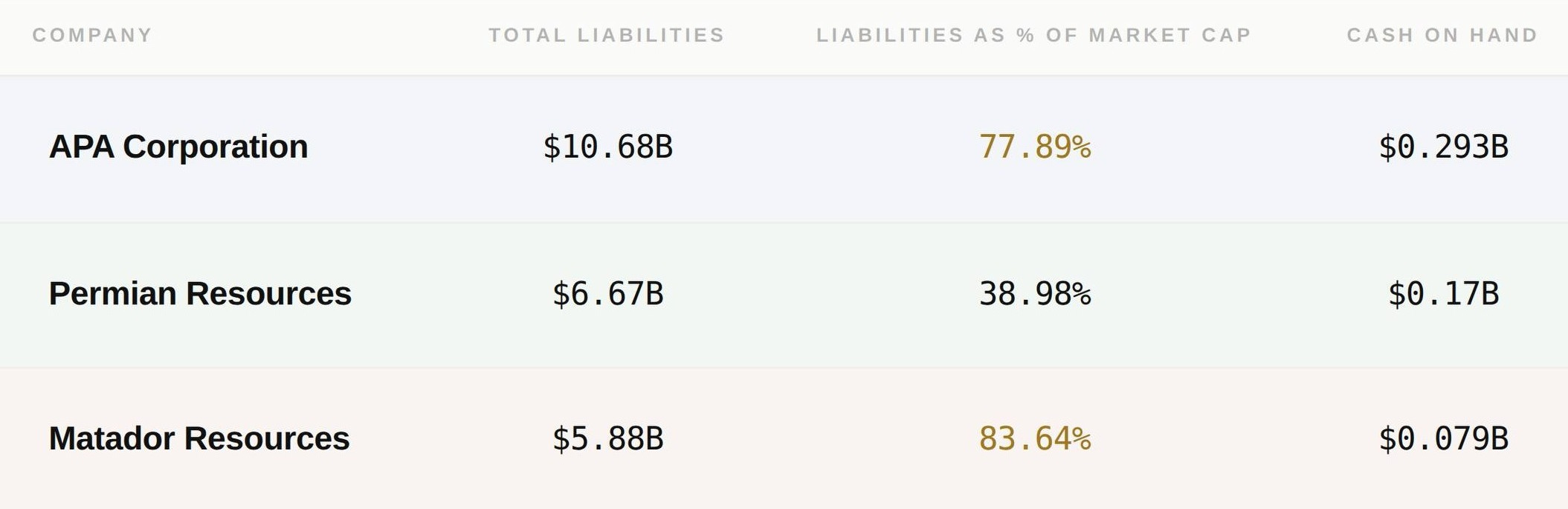

Debt. All three companies carry meaningful liabilities, and that limits how aggressively they can grow dividends — even in a strong pricing environment. Outright bankruptcy isn’t our base case, but it can’t be ruled out entirely, and a sustained downturn in oil prices would make the debt burden considerably harder to manage.

ESG and Green Energy Headwinds. Higher energy prices cut both ways: they make renewables more financially competitive and strengthen the energy-security case for domestic clean energy. There’s also the risk that the investing and banking community reverts to the 2020–2021 playbook: aggressively promoting green stocks while discounting or avoiding fossil-fuel names. That shift could suppress the multiples these companies deserve on fundamentals alone. The key uncertainty isn’t whether it happens, but when.

Verdict

APA Corporation. Buy at $38.80. The stock traded at roughly 3.5x this level in April 2011, which leaves substantial room for recovery. Two scenarios:

$48 within the next 16 months — 23.5% gain, excluding dividends.

Hold for 7 years and target 12% CAGR, including dividends.

Permian Resources. Buy at $20.44. The stock is trading near its historic peak, but the valuation still supports further upside. Two scenarios:

$24.30 within the next 16 months — 18.5% gain, excluding dividends.

Hold for 7 years and target 11% CAGR, including dividends.

Matador Resources. Buy at $56.64. The stock’s all-time high of $66.45, set in October 2022, anchors our expectations. Two scenarios:

$68 within the next 16 months — breaking above the prior high for a 20% gain, excluding dividends.

Hold for 7 years and target 11% CAGR, including dividends.