Plowing Into a Bargain With AGCO

Unlocked Edition #15. June 2026

Today we have a reasonably risky idea: buy shares of the American agricultural equipment maker AGCO Corporation (NYSE: AGCO). Despite some systemic headwinds, the stock looks dirt cheap (pun intended) and offers substantial shareholder value.

Expected Profits

19% profit in 16 months

30.5% profit in 3 years

~460% profit in 20 years (9% CAGR, excluding dividends)

Description of The Business

AGCO is a relatively young company (founded in 1990, like one half of the Opportunity Report’s team) that manufactures agricultural equipment.

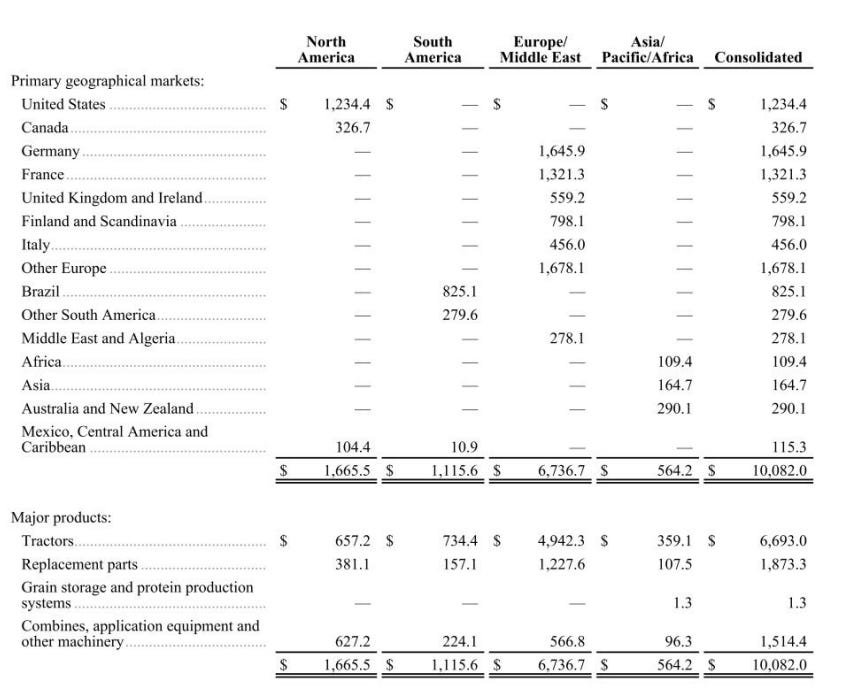

Here’s how AGCO’s revenue was structured in 2025:

Tractors — 66%

Combines — 2%

Hay tools, forage equipment, planters, implements, precision agriculture solutions, and other — 11%

Application equipment — 2%

Replacement parts — 19%

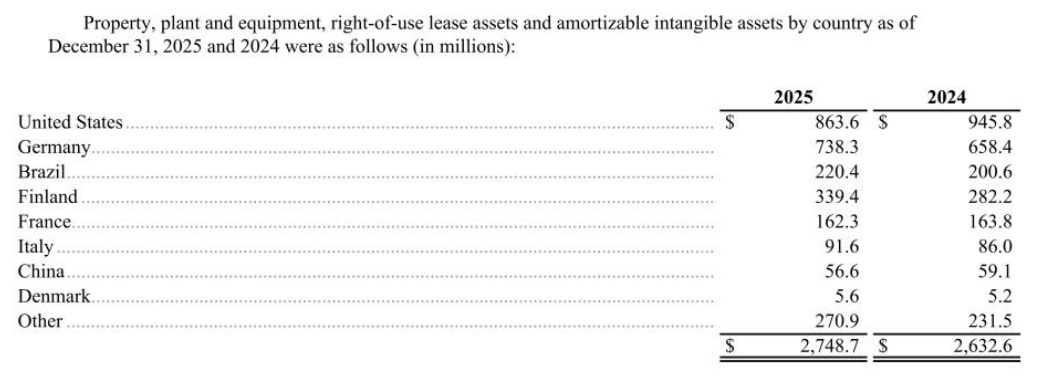

AGCO’s sales are highly diversified geographically. Germany is the single largest market (16.33%), followed by France (13.11%), and the U.S. (12.24%). No other countries account for more than 10% of sales: Brazil (8.18%), Finland and Scandinavia (7.92%), the UK and Ireland (5.55%), Italy (4.52%), and Canada (3.24%), with the remainder coming from other countries.

Overall, you could say AGCO is a distinctly Old World–oriented business.

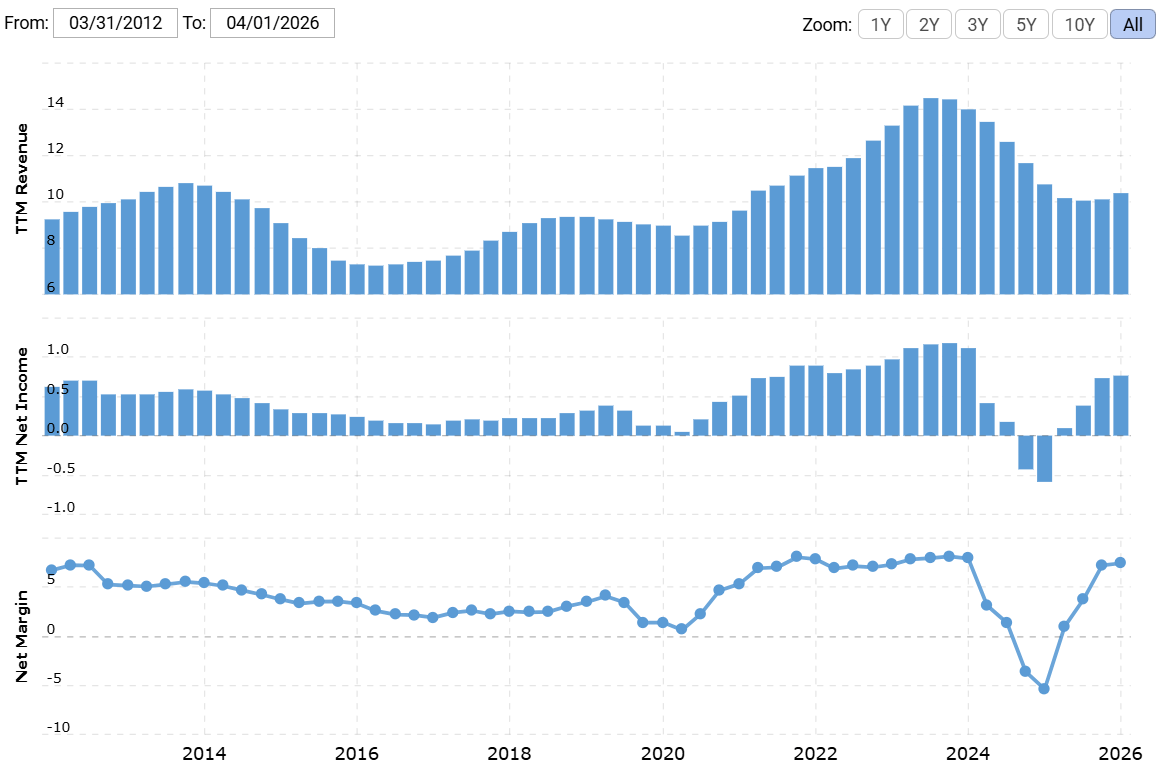

AGCO is profitable: for the 12-month period ended March 31, 2026, its gross margin was 25.33%, its operating margin was 6.04%, and its net margin was 7.43% (partly an accounting one-off, driven by non-operating income and a large one-time tax benefit).

Pros

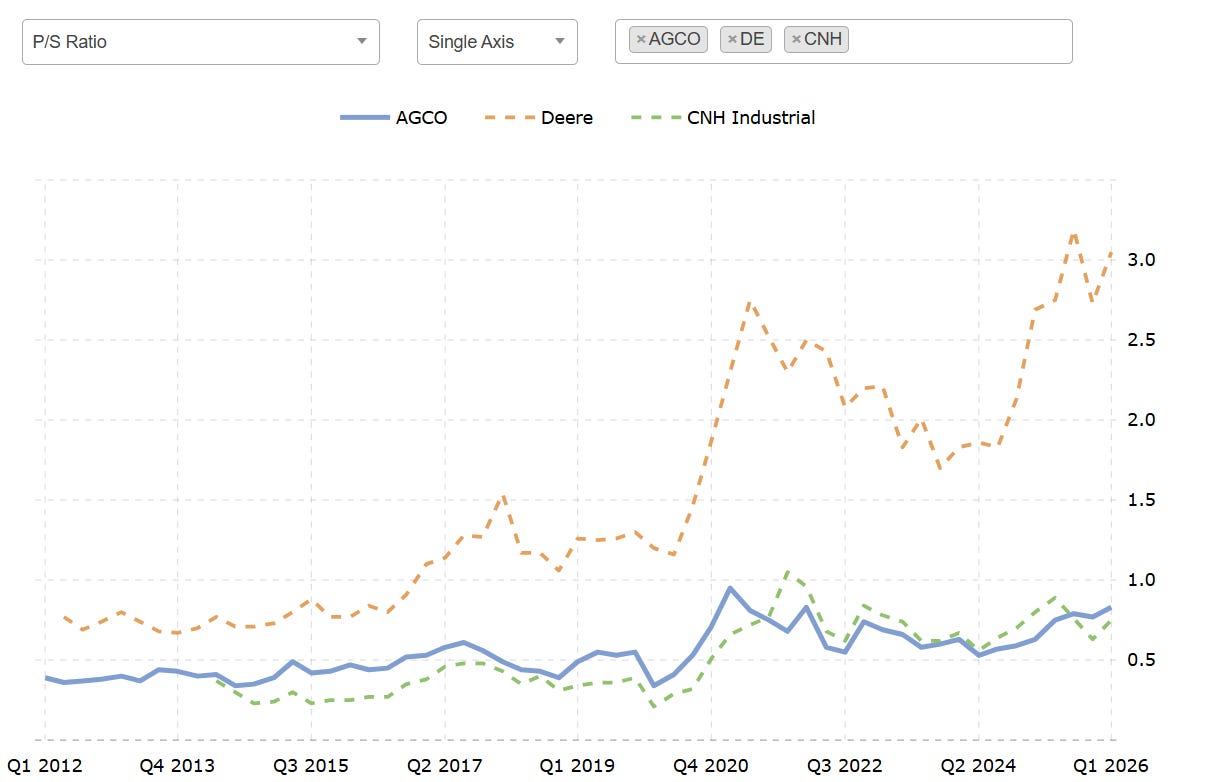

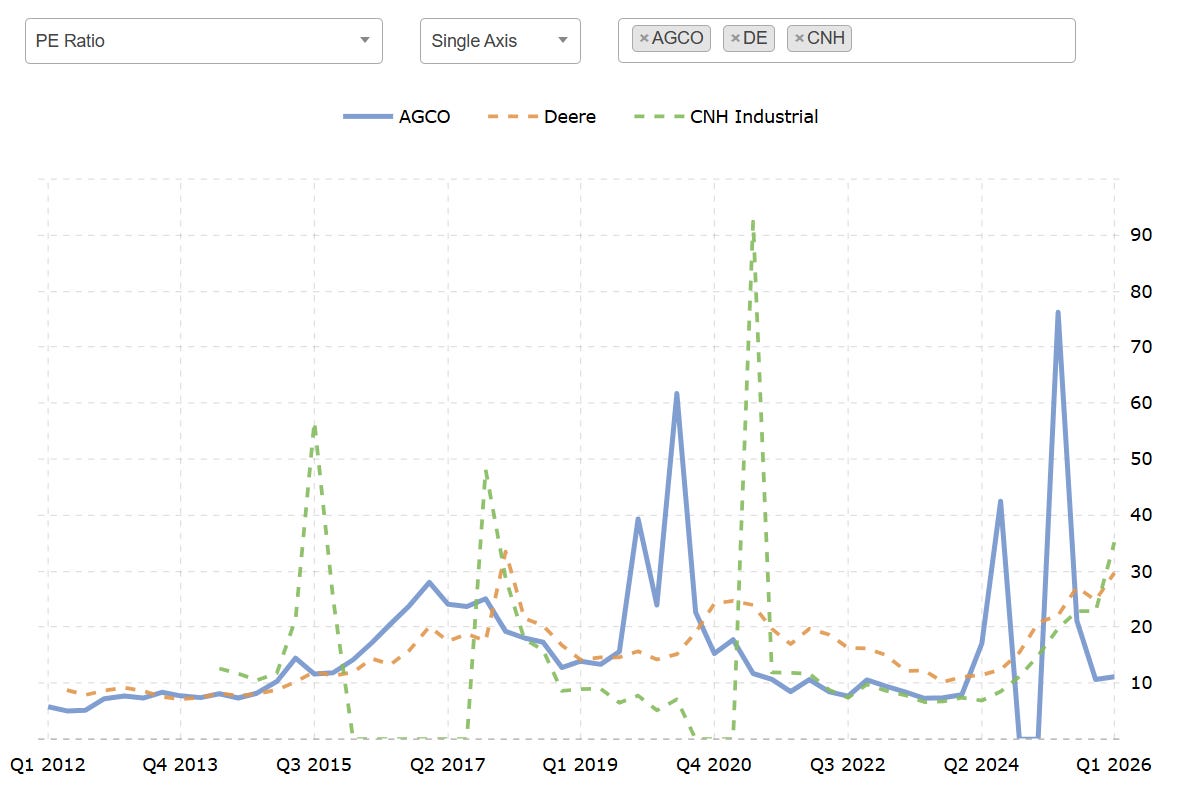

Very cheap. AGCO trades at 0.81x P/S and 11.16x P/E, which is extremely inexpensive. It’s also much cheaper than its competitor John Deere. With a market cap of about $8.19 billion, AGCO could bounce strongly from these levels — the stock looks like a bargain.

“Hillbilly balling, counting money on my tractor.” World food prices are high enough that, in theory, farming remains profitable — making it rational to invest in agriculture and potentially boosting AGCO’s order book. Of course, it’s not that simple (more on that in the “Cons”), but the logic holds: the world always needs food, and you can’t vibe-code nutrition (at least not yet).

Dividend growth potential. The company pays $1.20 per share annually, which is a mediocre 1.06% yield. However, AGCO spends relatively little on dividends: in 2025, the payout ratio was 11.88%, high by the company’s own standards. Potentially, AGCO could triple its payout over time, or at least deliver special one-time dividends, which could help lift the share price.

By virtue of exporting nature. AGCO is decidedly an exporter with the lion’s share of revenue coming from outside the U.S. which under current conditions (weakening USD) means more dollars reported in earnings reporting season.

M&A potential. In a sense, AGCO is a cash-generating business waiting for the right buyer: it’s cheap and relatively reliable. That’s why we think there’s a meaningful chance AGCO could be taken private either by a larger ag player or by private equity.

Cons

“I’m a small town boy with some big city dreams.” Contrary to the picture painted in Taylor Sheridan’s shows, farming is a hard and often depressing business with limited financial upside (to be fair, his shows portray financial hardship quite accurately).

While we don’t have exact numbers, the language in AGCO’s annual report suggests that most end customers are individual farmers (some of them may be very large), not giant agribusiness holdings. AGCO sells primarily through roughly 2,800 independent dealers and distributors worldwide. That matters because smaller farms face real hardship even in “good” years.

Right now, European farming sentiment (AGCO’s core market) is souring. In May, prices for many agricultural commodities slid, while fertilizer costs remained very high due to the Iran war. Given that many farmers operate on thin margins (five years of losses, five years of profits, and then one year that determines whether the farm lives or dies), they may scale back capital expenditures, which would hurt AGCO’s sales.

The silver lining is straightforward: if farmers underinvest this year, next year’s harvest could be smaller, which would push food prices higher and make farming more profitable, ultimately supporting a rebound in demand for agricultural equipment.

Supply-chain fatigue. AGCO’s assets are scattered around the globe, and with the war in Iran throwing a wrench into global transport, some of that stress could weigh on AGCO’s earnings. That said, it’s worth remembering that AGCO held up well in 2020–2022, when supply-chain disruptions were even more severe than they are now.

Heavy debt load. The company has $7.45 billion in total liabilities, $4.13 billion of which comes due by the end of March 2027. Meanwhile, it has just under $0.515 billion in cash on hand. On the bright side, it has $1.24 billion in receivables and about $3.0 billion in inventory, but the value of those assets can fluctuate.

Overall, the balance-sheet profile may deter some investors and could prompt AGCO management to cut the dividend (or, at minimum, limit meaningful payout growth).

“True” P/E is higher. Over the last 12 months, AGCO reported $642 million in operating profit, plus $45.5 million in equity earnings and a $74.8 million tax benefit. Adjusting for these non-operating items, AGCO’s “real” P/E would be closer to 15–16x. That’s not a dealbreaker, but it does make the stock look less dramatically undervalued.

Verdict

Buy now at $113.14. AGCO traded around $136.50 back in February: not an all-time high (it was almost $148 in 2022), but still a useful reference point that leaves meaningful room for a bounce. From here, we see a few ways to play it:

Bounce case: Wait 16 months for the stock to reach $135, which would imply a 19% gain, excluding dividends.

Extended case: The stock could reach $148 within the next 3 years, implying a 30.5% gain, excluding dividends.

Long-term case: Hold for 20 years and target roughly 9% CAGR, excluding dividends.