Kawasaki Heavy: The Bet Beyond the Motorcycles

Unlocked Edition #12. May 2026

Today’s idea is a bet on a Japanese industrial giant that has quietly held its ground through an energy crisis — and looks undervalued enough to reward patient investors: Kawasaki Heavy Industries (Tokyo Stock Exchange: 7012).

Expected Profits

19% profit in 15 months; ~184% profit in 10 years, 11% CAGR, including dividends

Note: Our return expectations include the possibility of spin-offs.

Description of the Business

Kawasaki Heavy Industries (Tokyo Stock Exchange: 7012) is a Japanese industrial conglomerate founded in 1878, spanning motorcycles, defense systems, trains, energy infrastructure, and industrial robotics.

Here’s how Kawasaki Heavy’s revenue was structured in 2024 — the 2025 annual report hasn’t been published yet.

Note: The company doesn’t specify which profit margin metric it reports at the segment level — operating, EBITDA, or otherwise.

Powersports & Engine — 28.7%. Motorcycles, off-road utility vehicles and ATVs, personal watercraft, and general-purpose gasoline engines.

Segment profit margin: 7.9%.Aerospace Systems — 26.7%. A mini-conglomerate within the conglomerate: military aircraft for Japan’s Ministry of Defense, commercial aircraft components, commercial helicopters, missiles, space equipment, aero engines, and aerospace gearboxes.

Segment profit margin: 9.8%.Energy Solution & Marine Engineering — 18.7%. A broad portfolio ranging from LNG tanks to boiler plants, and industrial energy systems.

Segment profit margin: 11.1%.Rolling Stock — 10.4%. Train-related products, including locomotives and freight cars.

Segment profit margin: 3.8%.Precision Machinery & Robot — 11.3%. Industrial and automation equipment — from hydraulic components for construction machinery to medical and pharmaceutical robots.

Segment profit margin: 2.9%.

By geography, Japan — 40.7%, the Americas — 31.5%, other Asian countries — 12.8%, Europe — 10.3%, other regions — 4.7%.

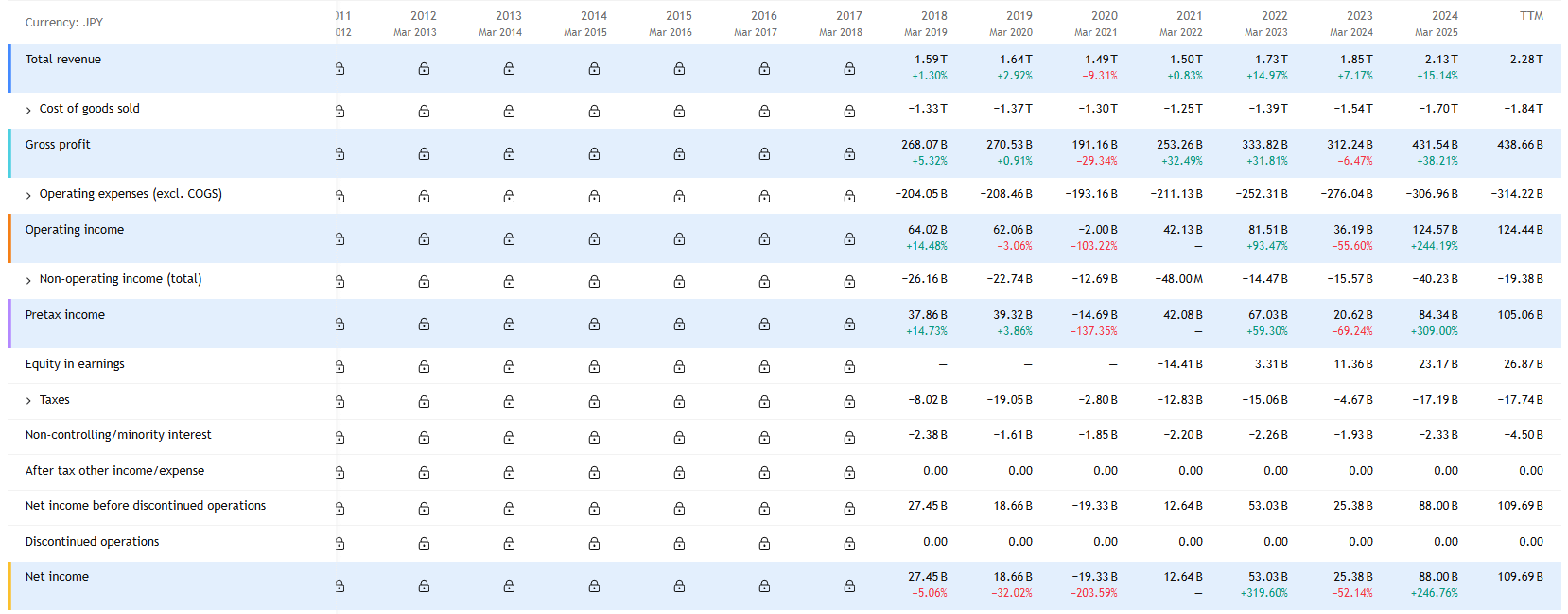

Kawasaki Heavy is profitable. For the 12-month period ended March 31, 2026: gross margin — 19.21%, operating margin — 5.43%, net margin — 4.78%.

You’re reading a free weekly idea. Want 1–3 ideas every Tuesday plus access to 80+ live ideas? Consider becoming a paid subscriber. Already a paying subscriber? Enjoy the new Unlocked Edition at no additional cost.

Pros

Relatively Cheap. At a P/S of 1.19 and a P/E of 24.79, the stock isn’t bargain-bin cheap — but the P/S in particular is low enough to suggest the market hasn’t fully priced in the business’s earnings potential. There’s room for a meaningful re-rating.

A Finger in Every Pie. Kawasaki Heavy is one of those rare industrial conglomerates where diversification actually feels like an advantage. Several segments are sitting squarely in the path of strong structural tailwinds right now.

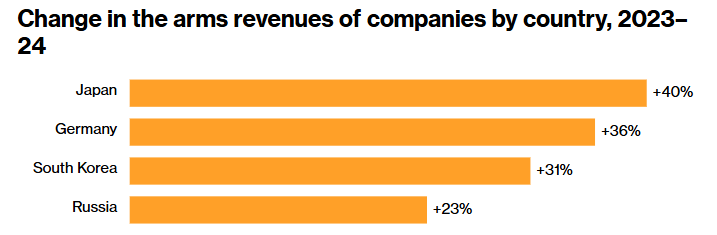

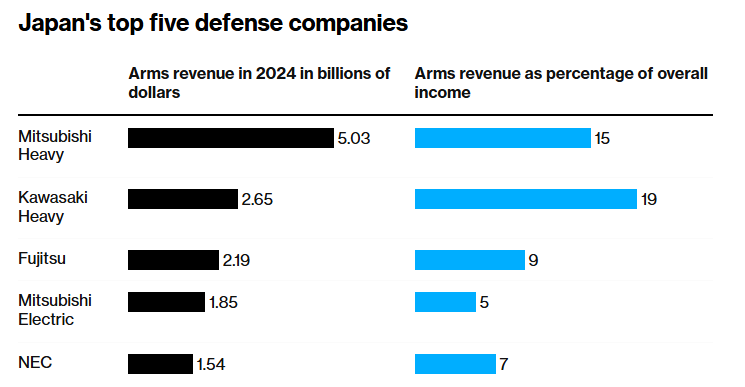

The Aerospace segment is perhaps the most compelling. Japan’s new prime minister has taken a noticeably more assertive foreign policy stance, and the country has recently lifted most of its longstanding restrictions on defense exports — a watershed shift for one of Asia’s most capable defense manufacturers.

Japan is already among the fastest-growing arms exporters in the world, and for good reason: depending on the category, Japanese military products can run roughly 35% cheaper than their U.S. equivalents. The Iran war has only sharpened the relevance of that cost advantage, exposing the budget strain of deploying expensive U.S.-made missiles against much cheaper enemy drones — a dynamic the Pentagon is reportedly addressing with about $200 billion in war-related funding requests to Congress. Kawasaki Heavy, one of Japan’s largest defense companies, is well-positioned to fill the role of a high-quality, cost-competitive supplier in a world that’s suddenly paying closer attention to price.

The Precision Machinery & Robot segment should also see strong demand over the next two years as manufacturers globally accelerate automation investment. And the remaining segments — with one notable exception covered in the Cons — can reasonably expect steady order flow, supported by ongoing capital expenditure cycles and the need to replace aging infrastructure both in Japan and abroad.

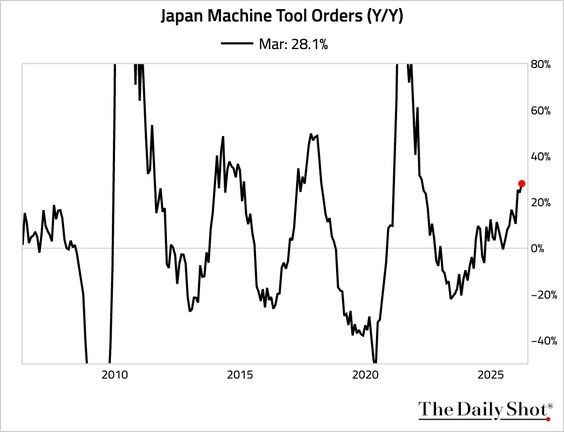

Japan’s Manufacturing Sector Is Holding Up. Japanese industrial activity indicators came in strong in March 2026 — a meaningful signal that the broader manufacturing environment, and likely Kawasaki Heavy’s order book, is weathering current conditions better than many global peers.

Spin-Off Potential. Kawasaki Heavy is a classic sum-of-parts story waiting to happen. If the company were to separate its divisions into standalone businesses, each could plausibly trade at a higher multiple and grow faster than the combined entity currently does. There’s no indication management is moving in that direction — but the optionality is real, and it adds a layer of upside that isn’t captured in the current valuation.

Strong Foreign-Investor Interest. In dollar terms, Kawasaki Heavy is roughly a $17 billion company — modest by U.S. large-cap standards, but a meaningful name in the Japanese market. Foreign investor flows in Japanese equities have remained elevated, and a relatively cheap, high-quality industrial with defense exposure is exactly the kind of name that tends to attract overseas capital when that trend is running.

Cons

Risk of a Stronger Yen. With close to 60% of sales generated outside Japan, Kawasaki Heavy benefits when the yen is weak — foreign-currency revenue converts into more yen on the income statement. The problem is that Japanese policymakers have grown uncomfortable with how far the yen has weakened, partly as a result of war-related currency shocks. A shift toward more hawkish rate policy could strengthen the yen and meaningfully weigh on reported earnings. This is one of the clearer macro risks in the thesis, and worth watching closely.

Oil Supply Repercussions. Japan imports about 95% of the oil it consumes, and its primary suppliers — the UAE, Saudi Arabia, Kuwait, and Qatar — are exactly the countries most exposed to a potential Strait of Hormuz disruption. That’s a concentrated vulnerability. The mitigating factor is Japan’s strategic reserve position: as of December 2025, the country held about 254 days’ worth of oil consumption in reserve. It’s a useful buffer, although not an unlimited one. It’s also worth noting that the latest quarterly report predates the war and the subsequent oil price spike, so the full operational impact on Kawasaki Heavy remains unknown.

Powersports & Engine Segment. If elevated oil prices persist, this segment could face pressure — motorcycles are relatively fuel-efficient, but sustained high energy costs tend to dampen consumer confidence and discretionary spending. Japan’s consumer confidence index has already dipped over the past two consecutive months, and a further softening could weigh on sales in this division.

Debt Load. Total liabilities stand at ¥2.41 trillion, and roughly 80% of that comes due by the end of this fiscal year. Cash on hand is just ¥0.108 trillion. The company can likely manage near-term obligations through receivables (¥0.984 trillion) and inventory (¥0.901 trillion) — but neither is risk-free. Customers can default, receivables can turn into losses, and inventory values can move against you. That balance sheet profile limits how much management can do on dividends: Kawasaki Heavy currently pays ¥30 per share annually — about a 0.59% yield — distributing roughly 28.55% of net profit. A meaningful payout increase would stretch an already tight balance sheet, and rising Japanese interest rates would make debt servicing incrementally more expensive over time.

Verdict

Buy now at ¥3,266. The stock traded around ¥3,651 in February, and that level anchors our upside expectations. Two scenarios from here:

¥3,900 within the next 15 months — 19% profit, excluding dividends.

Hold over 10 years and target ~11% CAGR, including dividends.

Enjoyed the reasoning and our recent streak? 9 of our last 20 picks have already hit their targets (four within four days of publication). If you know one person who invests, sharing Opportunity Report is the biggest favor you can do us (their portfolio won’t mind either).