Investing in the Worst Subscription Cancellation Flow on the Market

Unlocked Edition #9. April 2026

This week we are looking at a modestly speculative opportunity in a name most investors already know well: Adobe (Nasdaq: ADBE). The setup isn’t flashy, but the valuation is doing most of the work here. At current levels, the stock looks cheap enough that even a modest normalization could deliver meaningful upside.

You’re reading a free weekly idea. Want 1–3 ideas every Tuesday plus access to 80+ live ideas? Consider becoming a paid subscriber. Already a paying subscriber? Enjoy the new Unlocked Edition at no additional cost.

Expected Profits

20.5% profit in 15 months;

45.5% profit in 26 months;

178.5% profit in 10 years

Description of the Business

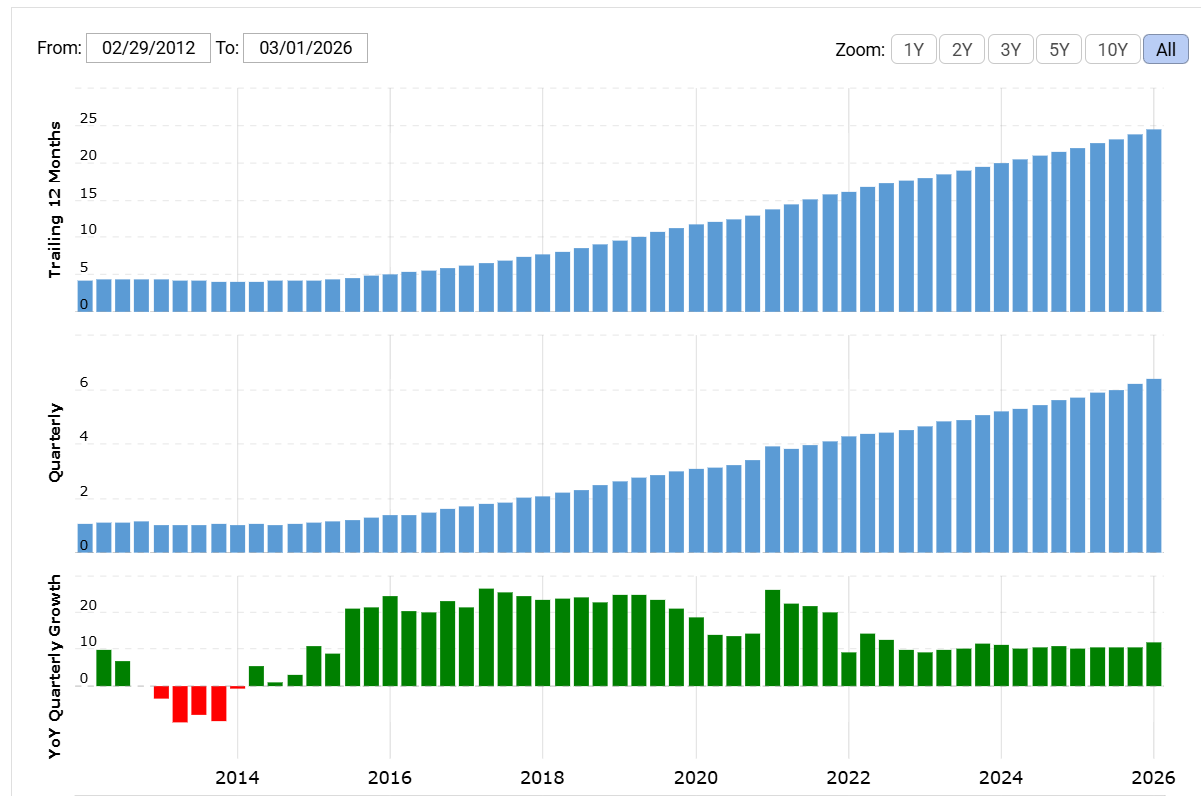

Adobe is, at its core, a cloud company. Its products are delivered through infrastructure it owns and operates — the standard SaaS (software as a service) model — where users access software remotely rather than installing it locally.

That wasn’t always the case. Adobe built its early dominance selling boxed software in the 1990s, then gradually transitioned to the cloud starting in the late 2000s. The shift from one-time purchases to recurring subscriptions is what turned Adobe into the highly predictable, high-margin business it is today.

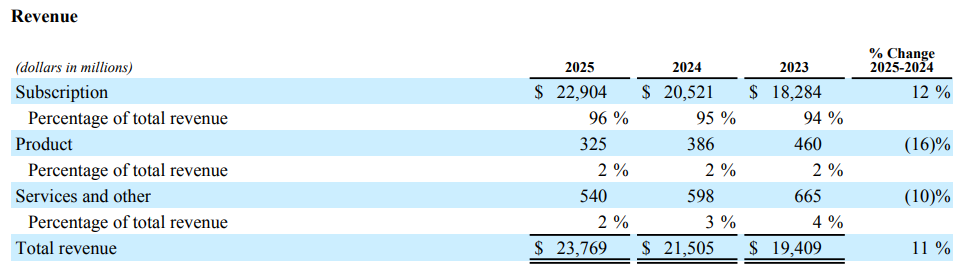

Here’s how revenue was structured in 2025:

Digital Media — 74%. Creative and content tools: Photoshop, After Effects, and the broader Creative Cloud ecosystem that has become an industry standard for designers, video editors, and digital creators.

Digital Experience — 25%. Marketing and analytics tools for enterprises, including Audience Manager and Primetime — products designed to help companies understand and target users more effectively.

Publishing and Advertising — 1%. Legacy and niche offerings: eLearning tools, document platforms, web conferencing, and high-end publishing solutions.

About three-quarters of revenue comes from individual creators and marketing professionals, with the remainder coming from enterprise clients. The mix gives Adobe both a broad base of sticky individual users and higher-value corporate relationships.

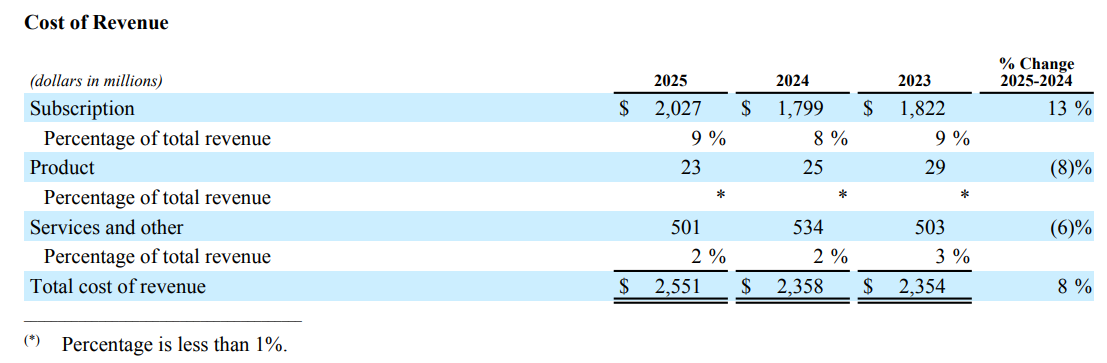

Subscriptions account for 96% of total revenue. That’s the key to the story: recurring revenue, high visibility, and very little cyclicality compared to traditional software models.

Geographically, the business is still anchored in the U.S., which generates 52.71% of revenue, with the rest spread across international markets.

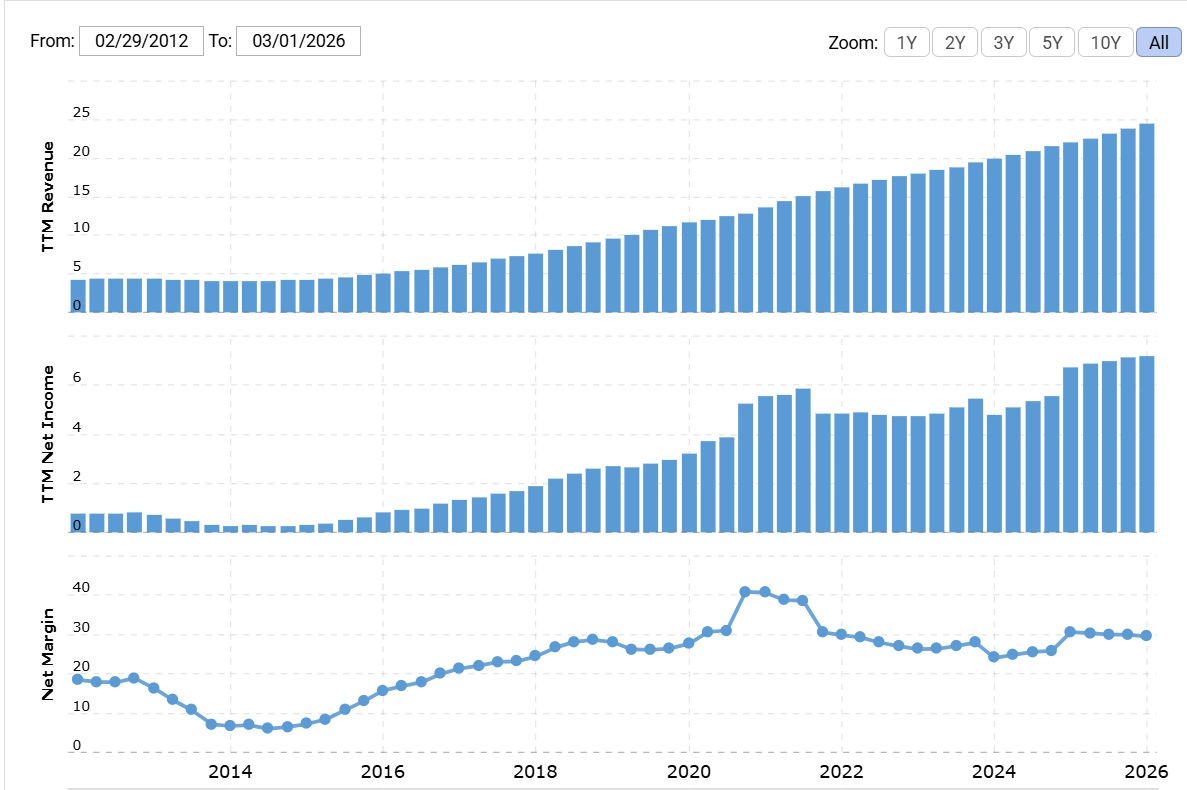

And the margins are exactly what you’d expect from a scaled SaaS leader: 89.4% gross margin, 36.65% operating margin, and 29.48% net margin over the past 12 months.

Pros

Deep Value By Tech Standards. Adobe looks inexpensive almost no matter how you slice it. A P/S of 3.79 and a P/E of 13.13 put it well below typical U.S. tech valuations — even after the broader market’s recent pullback. In a sector where “expensive but justified” is the norm, Adobe stands out for simply being… cheap. That alone is enough to put it on the radar.

AI Fears Haven’t Materialized (Yet). The market punished Adobe when AI tools started looking like potential substitutes for parts of its product suite. That concern wasn’t irrational — if cheaper tools can replicate core functionality, pricing power comes under pressure.

But so far, the feared exodus hasn’t shown up in the numbers. Recent results actually show continued growth, with no sign of users abandoning the platform at scale. More importantly, Adobe isn’t standing still: AI tools like Google’s Gemini/Nano Banana are now integrated directly into its ecosystem (Firefly, Generative Fill, etc.).

In other words, AI is increasingly being absorbed into Adobe’s offering rather than replacing it. If that dynamic holds, the narrative around “AI disruption” could shift quickly — and with it, the stock’s valuation.

Optionality on Capital Returns. Adobe doesn’t pay a dividend — but it easily could. This is a mature, highly profitable business with predictable cash flows and strong margins. The company earns roughly $17 per share annually, which implies it could, in theory, return around $8.50 per share without straining the business — roughly a 4% yield.

That’s unusually high for a tech company, and it opens the door to a classic catalyst: activist pressure. With the stock still far below its 2021 peak, a dividend or structured capital return program would be one of the simplest ways to re-rate the shares.

Two structural details make that scenario more plausible: no dual-class shares and no controlling shareholder. Management doesn’t have an easy way to ignore investor pressure if it builds.

Cons

AI Competition Is Real — Just Not Immediate. The risk isn’t hypothetical. Adobe’s pricing reflects extremely high margins — north of 90% — which naturally invites competition sooner or later. Cheaper AI-driven alternatives are starting to emerge, and for a certain segment of users, they’re already “good enough”.

The trade-off is straightforward: Adobe offers a deeply integrated, professional-grade ecosystem — but at a price. And as budgets tighten, that price becomes harder to ignore. Many users, especially individuals or smaller teams, now have a clear incentive to experiment with cheaper tools like Nano Banana, which — outside of Adobe’s bundled ecosystem — can be significantly cheaper.

That doesn’t mean users are leaving en masse. So far, they aren’t. Adobe’s tools still set the standard in many categories, and for serious creative work, switching costs — both technical and behavioral — remain high. The company is also moving quickly to integrate AI into its own products, which helps neutralize some of the competitive threat.

But the question isn’t whether pressure exists — it’s how it evolves. Could a meaningful customer shift toward cheaper AI tools happen over time? Absolutely. The more difficult question is timing. Does that shift begin in the next few quarters, or does it take years, as AI tools become more capable, more reliable, and more deeply embedded in creative workflows?

Figma Remains a Structural Competitor. Figma is arguably Adobe’s most credible direct competitor — and importantly, it’s still independent. Adobe’s attempt to acquire the company in 2022 ultimately failed under regulatory pressure, leaving a strong rival firmly in place.

Figma’s growth metrics are hard to ignore. Its reported net retention rate (NRR) of 136% suggests that existing customers are not only staying, but expanding their usage meaningfully over time. Adobe, notably, does not disclose its own NRR — and in most cases, companies highlight that metric when it’s a strength.

Note: Net retention rate (NRR) shows how much the company’s existing customers are spending compared to last year. 100% NRR means no change, less than 100% means customers are shrinking or leaving, and more than 100% means customers are expanding their spending.

There is, however, an important caveat. Figma’s growth comes at a cost — literally. The company reportedly loses about $1.31 for every $1.00 of revenue, which raises questions about how sustainable its current level of customer acquisition and pricing strategy really is. Competing aggressively is easier when profitability isn’t a priority. Even so, Figma doesn’t need to win the entire market to matter. It just needs to keep chipping away at Adobe’s edges — and for now, it’s doing exactly that.

AI Is a Costly Investment. Adobe isn’t just reacting to AI — it’s spending heavily to stay competitive. While the company doesn’t break out AI-specific costs, the direction is clear: over the past three years, annual R&D spending has increased by 43.75%, reaching $4.294 billion.

That aligns with a broader industry trend. Across U.S. tech, a growing share of capital is being funneled into AI — whether for infrastructure, talent, or model development. Adobe is no exception, and it’s reasonable to assume that AI now accounts for a significant portion of its R&D budget.

The challenge is that this kind of investment tends to compound. As more companies compete for the same inputs — engineers, compute, data infrastructure — costs rise. What starts as a necessary investment can gradually become a structural expense.

In other words, even if AI strengthens Adobe’s product offering, it may also weigh on margins over time. That’s the trade-off.

Balance Sheet Constraints. Adobe’s financial position is solid, but not frictionless. The company carries $18.27 billion in total liabilities, with $11.39 billion coming due by the end of February 2027. Against that, it holds approximately $6.89 billion in cash.

This isn’t alarming — Adobe generates strong cash flow and remains highly profitable. But it does limit optionality. When you combine near-term obligations with rising AI-related spending, the likelihood of initiating shareholder payouts becomes lower.

Negative Sentiment. Even strong businesses can underperform when sentiment turns against their sector. Right now, that’s the case for much of tech.

Investors have been rotating toward “hard” asset-heavy — utilities, energy, infrastructure — while keeping relatively lighter exposure to software and other intangible-heavy businesses. Adobe, despite its profitability, is still caught in that shift.

That doesn’t change the fundamentals, but it does affect timing. A stock can remain undervalued longer than expected if the broader market simply isn’t interested.

Verdict

Buy now at $240.11. From there, the path is fairly straightforward:

The conservative approach is to target $290 within 15 months — a 20.5% return. That’s a reasonable base case if valuation simply normalizes.

A stronger recovery could push the stock to $350 within 26 months, delivering a 45.5% return.

And for long-term holders, a return to the 2021 peak of $669 over a 10-year horizon would imply a 178.5% profit.