Hitting the Right Note With Music Giants

Unlocked Edition #8. April 2026

Today’s idea is a moderately speculative bet on two dominant players in the global music industry that, for now, look mispriced relative to the durability of their underlying businesses. The setup is straightforward: high-quality assets, steady cash flows, and a market narrative that may be leaning too far in one direction.

Issuers

Universal Music Group N.V. (Euronext Amsterdam: UMG) — a Dutch music company

Warner Music Group Corp. (NASDAQ: WMG) — U.S.-based music company

Expected Profits

Universal Music Group (UMG): 23.5% profit in 15 months; 159% profit in 10 years, 10% CAGR (including dividends)

Warner Music Group (WMG): 24% profit in 15 months; 136% profit in 10 years, 9% CAGR (including dividends)

Description of the Business

Universal Music Group N.V. was originally an American business, but over time it passed through multiple owners before ending up under the French media conglomerate Vivendi. In 2021, Universal Music was spun off and listed as a standalone company in Amsterdam, although its operational center of gravity remains in California. That split created a cleaner equity story and made its economics more visible to public market investors.

Here’s how the company’s revenue was structured in 2025:

Recorded Music — 75.21%. This segment includes licensing UMG-owned recordings (IP) to distributors and digital platforms. While it may appear passive at first glance, it is anything but: Universal signs artists, funds production, manages promotion, and monetizes recordings across a wide range of channels.

Segment adjusted EBITDA margin: 25.6%.Music Publishing — 17.75%. Revenue from third-party use of copyrights on musical works owned or administered by the company. This is a steadier, rights-driven business that benefits from long-tail monetization of catalog assets.

Segment adjusted EBITDA margin: 24.3%.Merchandising and Other — 7.05%. Sales of artist-related merchandise, including apparel, accessories, and various branded goods. While smaller and lower-margin, this segment complements the core music business and deepens fan engagement.

Segment adjusted EBITDA margin: 2%.

Geographically, the U.S. accounts for 50.46% of Universal’s revenue, followed by the U.K. at 9%. Japan at 6.43% and Germany at 5.1%, with the remainder spread across smaller markets.

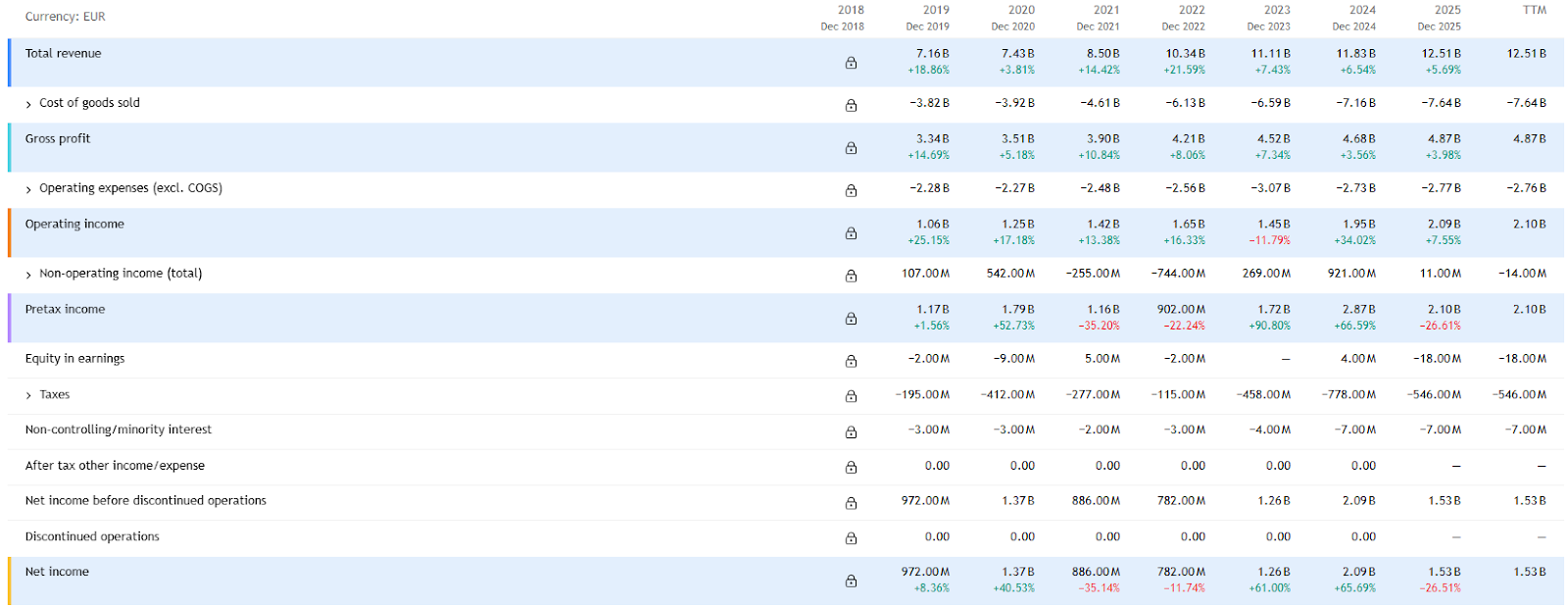

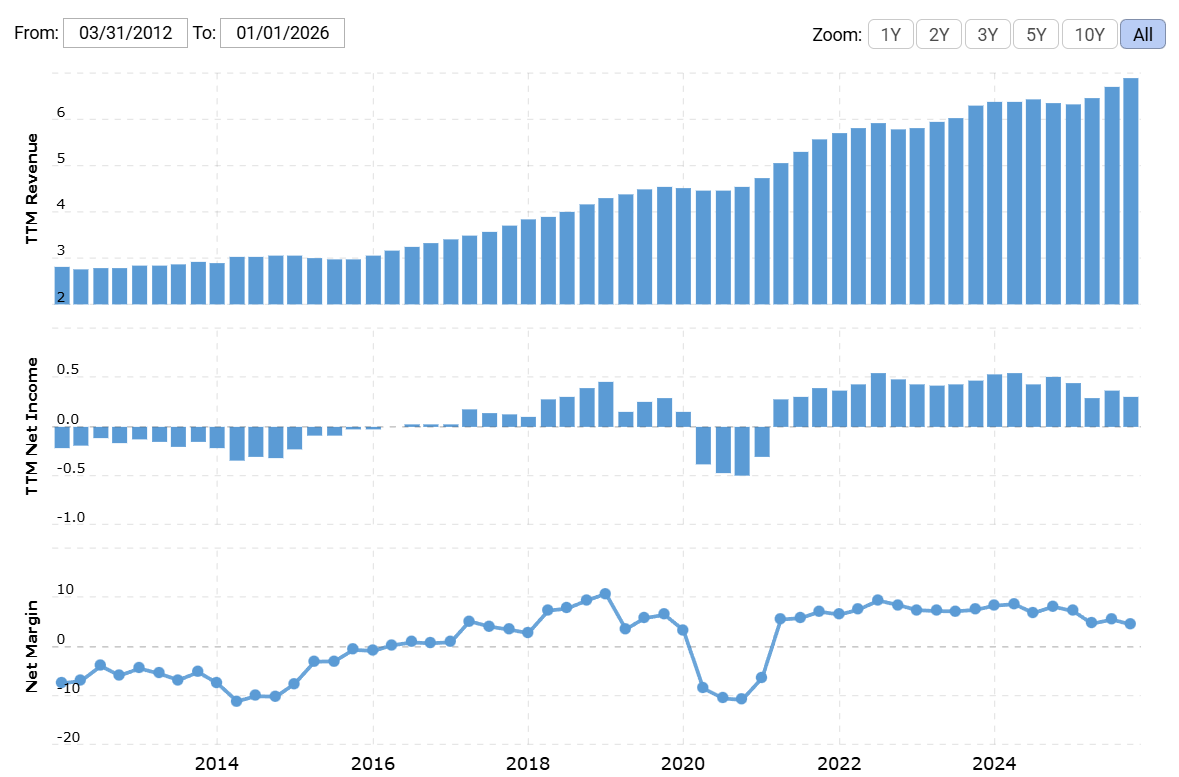

Universal Music is profitable: in 2025, its gross margin was 38.92%, operating margin 16.78%, and net margin 12.23%.

Warner Music Group Corp. operates with a similar structure, though with some differences in mix and margins. In 2025, the company’s revenue came from:

Recorded Music — 80.63%. This includes the sale, marketing, distribution, and licensing of music produced by Warner’s artists. As with Universal, this is the company’s primary revenue driver, anchored in its catalog and artist relationships.

Here’s a more detailed breakdown of this segment:

Digital — 53.58%. Revenue from streaming and downloads, which continues to dominate consumption trends.

Physical — 7.85%. Sales of vinyl, CDs, and DVDs — still relevant, particularly among collectors and niche audiences.

Artist Services and Expanded Rights — 12.44%. Fees and revenue shares from distribution, marketing, and rights management.

Licensing — 6.43%. Royalties from third-party use of Warner-owned recordings.

Segment operating margin: 15.71%.

Music Publishing — 19.37%. Payments received as the copyright owner or administrator of musical works.

Segment operating margin: 17.15%.

Geographically, 42.85% of Warner Music’s revenue comes from the U.S., 12.78% from the U.K., and 7.68% from Germany, with the rest distributed globally. The mix is slightly less U.S.-heavy than Universal’s but still anchored in developed markets.

Warner Music is also profitable, though margins are thinner: gross margin was 45.87%, operating margin 11.16%, and its net margin was 4.43% in 2025. The gap largely reflects cost structure differences and capital allocation choices.

Why the Stocks Are Down

It’s somewhat puzzling that the market has repriced these companies lower without any obvious deterioration in fundamentals. There are no major red flags — just a shift in sentiment that appears to be driven more by narrative than by numbers.

The dominant concern is AI. Investors worry that if AI-generated music becomes “good enough,” record labels could lose relevance. It’s a clean story, and the market tends to price those in quickly.

We think that concern is overstated. Both Warner and Universal own vast catalogs built over decades of cultural relevance and fan loyalty. Replacing artists like Fleetwood Mac, Madonna, Prince, or The Doors with AI-generated equivalents is not just a technical challenge — it’s a cultural one.

AI-generated music will likely grow as a category. But replacing deeply embedded human artists is a different question entirely, and one that seems far less imminent. In that context, current fears look more like a sentiment overreaction than a structural shift — which is often where opportunities emerge.

Pros

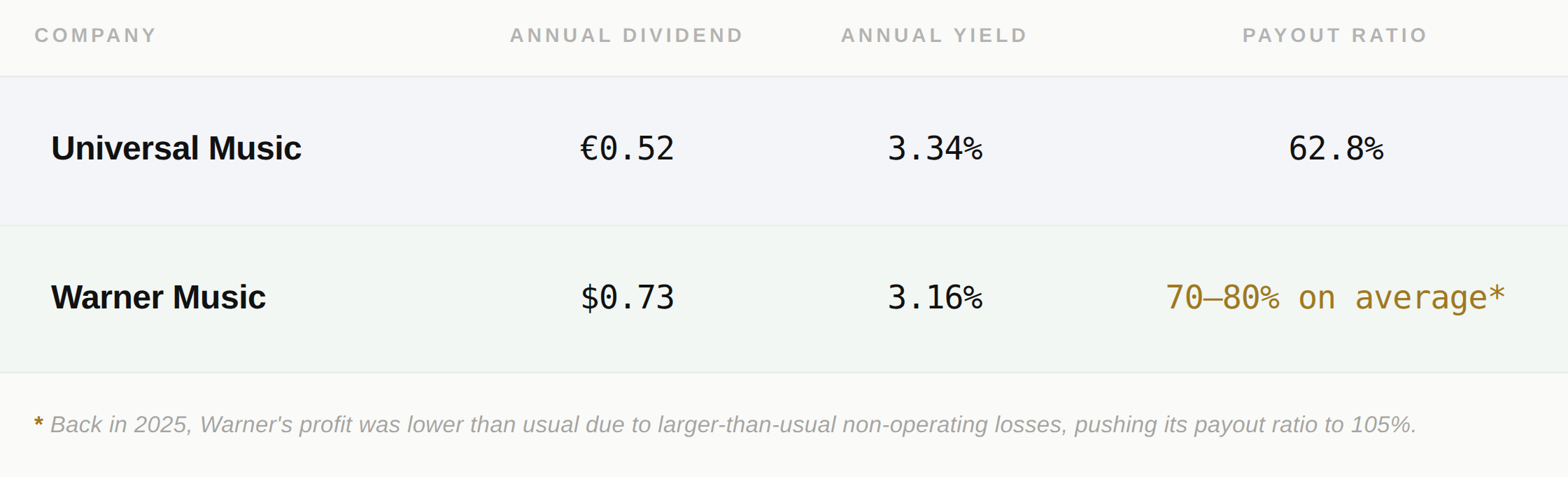

Attractive Yields. Both companies generate relatively stable and predictable cash flows, which support consistent dividend payments. While yields are not extraordinary, they are solid enough to matter in a market where income is back in focus.

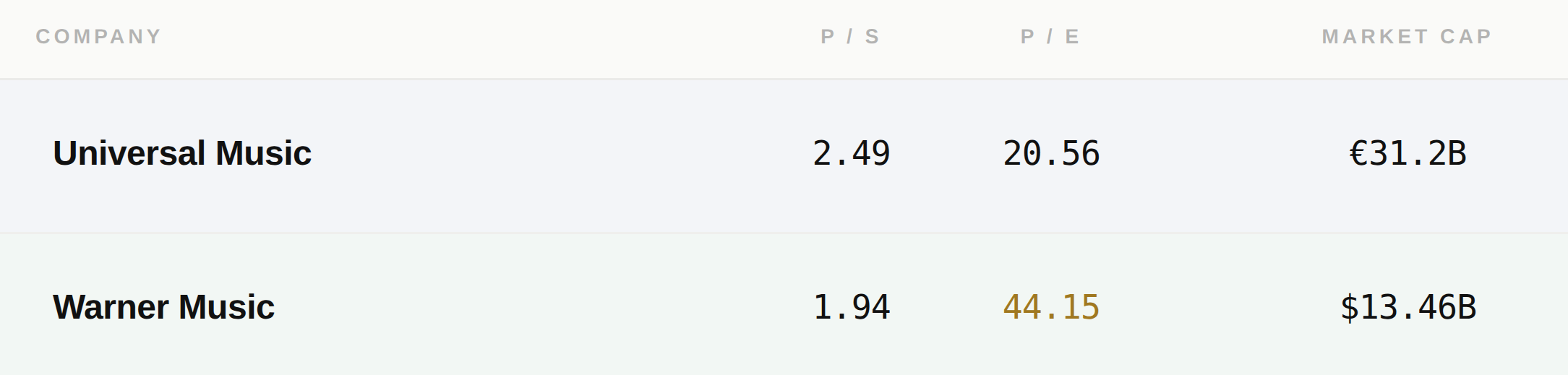

Relatively Cheap. Valuations are modest both in absolute terms and relative to the quality of the underlying assets. These are effectively oligopolistic businesses with long-lived intellectual property, yet they are not priced as such.

Attractive Acquisition Targets. Given their scale, cash flows, and asset quality, both companies could draw interest from private equity or strategic buyers. There are relatively few assets of this caliber available, which increases their appeal. Even a possibility of M&A — however theoretical — can act as a valuation floor.

Cons

Corporate Governance Issues. Both companies have dominant shareholders, which creates potential misalignment with minority investors. Warner Music’s dual-class structure gives outsized voting power to entities linked to Len Blavatnik, while Universal is controlled by a Tencent-led consortium. This concentration can influence key decisions in ways that don’t always favor public shareholders.

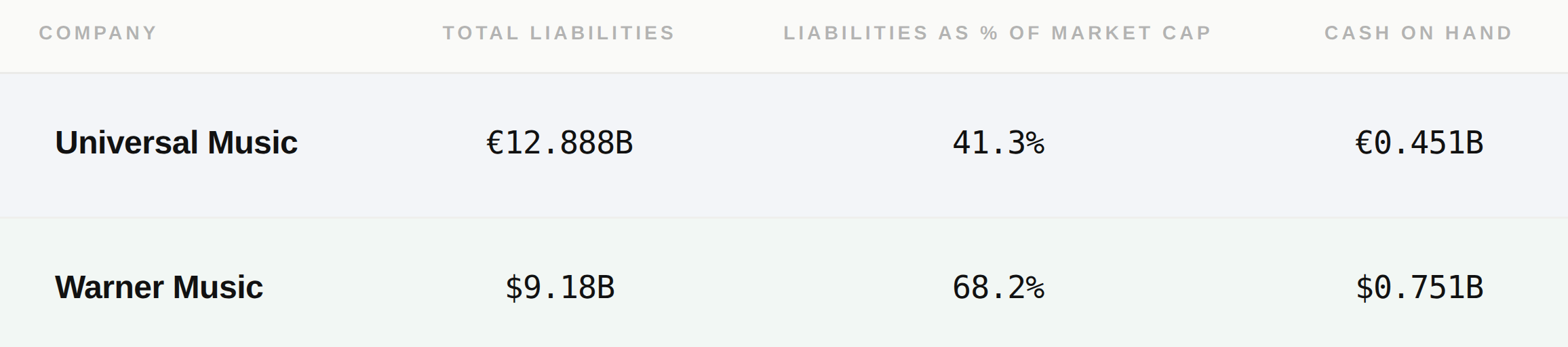

Balance Sheets. Debt levels at both companies are relatively high, particularly in a higher-rate environment. What looked manageable during more accommodative monetary conditions now carries greater risk, especially if refinancing costs rise. Dividend cuts to prioritize debt repayment are a plausible downside scenario.

AI Could Still Be a Threat. While current fears may be overstated, AI is not irrelevant — and it’s worth taking the risk seriously, even if it’s not immediate. AI-generated music could affect these businesses in two ways, both tied to how content is produced and consumed.

Lower Licensing Sales to Third Parties. Some portion of revenue comes from content creators who pay Universal and Warner for the right to use their music in films, ads, games, and other media. As production costs rise, there’s a growing incentive to cut expenses wherever possible — and music licensing is an obvious target. If AI-generated alternatives become “good enough,” some creators may opt for cheaper, custom-made tracks instead of paying for existing catalogs. That said, licensing revenue is meaningful, but it is not the core driver of either company’s business, which limits the immediate downside.

Proliferation of Fan-Made Music. A more structural risk is a shift in how music is created and consumed. If AI tools become cheap, intuitive, and widely adopted, users may start generating more of their own music — or consuming AI-generated content tailored to their preferences. Over time, that could reduce both listening time and spending on established artists, which would directly impact label revenues. This scenario is still highly hypothetical, but it’s not without precedent: two decades ago, it wasn’t obvious that phone cameras would disrupt standalone digital photography — yet that’s exactly what happened.

That said, none of these risks has materialized in any meaningful way so far. For now, this is less a confirmed threat and more a reminder to stay attentive — perhaps even a bit overly cautious.

Verdict

Universal Music — Buy now at €16.97.

The stock traded at €28 in May 2024, which provides a useful reference point for potential upside. From here, there are two reasonable paths:

Wait for a move to €21 in the next 15 months, implying a 23.5% profit excluding dividends.

Hold for 10 years and target a 10% CAGR, including dividends.

Warner Music — Buy now at $25.76.

The stock reached $49.99 in October 2021, and that prior level helps frame expectations. Again, there are two main scenarios:

Wait for a move to $32 in the next 15 months, implying a 24% profit, excluding dividends.

Hold for 10 years and target a 9% CAGR, including dividends.