Going Long on Doximity — Collateral Damage in the AI/Software Selloff

Unlocked Edition #2

You’re reading a free weekly idea. Want 1–3 ideas every Tuesday plus access to 40+ live ideas? Consider becoming a paid subscriber. Already a subscriber? Enjoy the new Unlocked Edition at no additional cost.

Instead of chasing hype, today’s idea comes from the opposite direction: a high-quality business that the market may have punished too aggressively. We’re looking at Doximity (NYSE: DOCS), an American healthcare technology company whose stock has been hit hard after a guidance reset. In our view, the reaction looks excessive — and that opens the door to a meaningful rebound.

Expected Profits

24.5% profit in 15 months;

52% profit in 3 years;

~11% CAGR over 10 years.

Description of the Business

Doximity is a professional networking and workflow app designed specifically for U.S. healthcare professionals. Think of it as a purpose-built digital hub for clinicians rather than a generic social network. Doctors and other medical professionals use Doximity to stay connected with colleagues, manage parts of their daily workflow, and access job-related tools.

The platform supports telehealth and secure video visits, on-call scheduling, and other routine administrative tasks. It’s also widely used by hospitals and health systems for hiring and recruiting medical professionals.

Clinicians typically use Doximity for free. The company makes money on the other side of the marketplace — by charging pharmaceutical companies and health systems for digital marketing, and by selling hiring, recruiting, and enterprise workflow products to healthcare organizations.

According to Doximity’s 2024 annual report:

Subscription — 95.33%. These subscriptions are sold mainly to pharmaceutical companies, health systems, and recruiting firms.

Other — 4.67%. Non-recurring revenue such as fees from temporary staffing and permanent placements.

All of Doximity’s revenue is generated in the U.S.

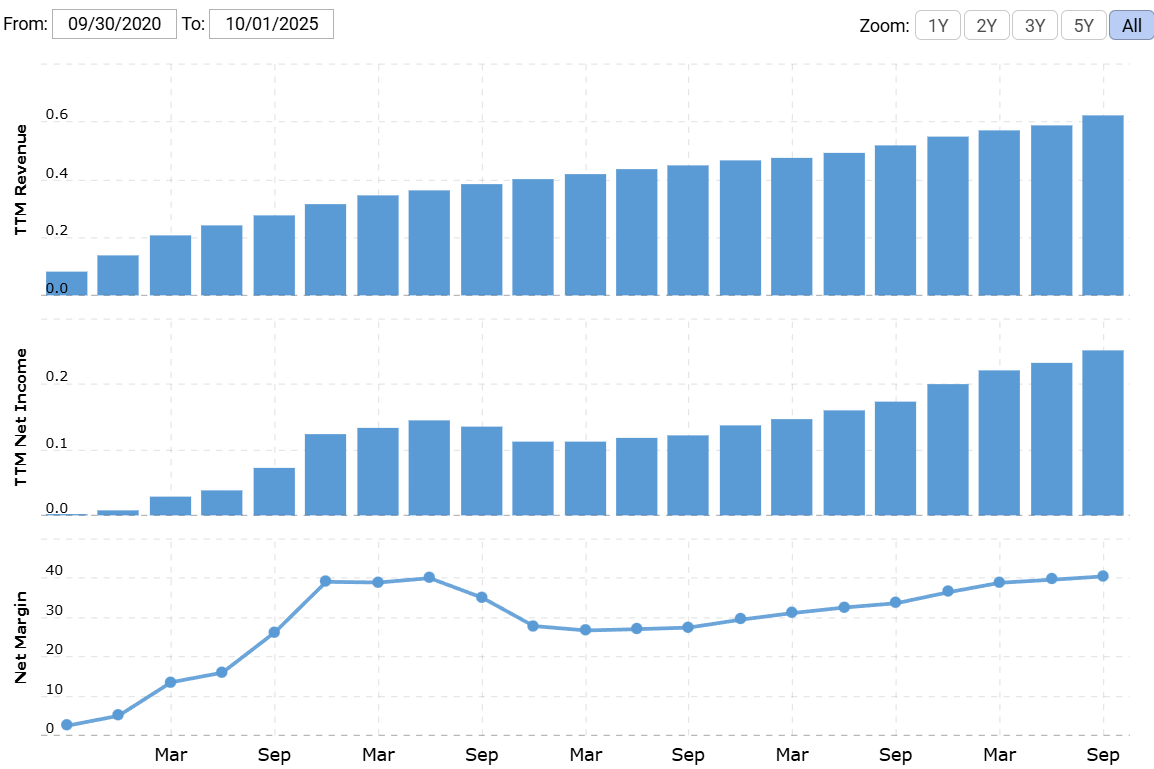

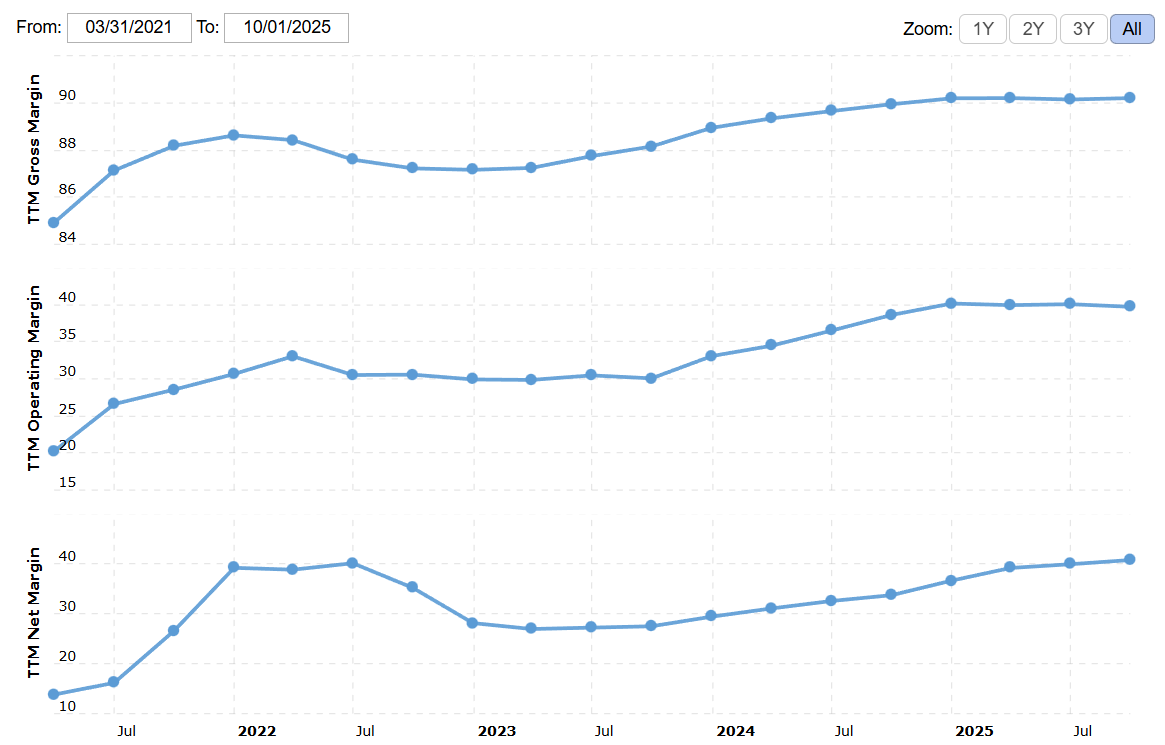

The company is highly profitable: for the 12-month period ended September 30, its gross margin was 90.2%, operating margin was 39.72%, and net margin was 40.72% (The net margin figure is boosted by a one-time non-operating income item).

Why Doximity Stock Is Down

Doximity shares are hovering near all-time lows after a sharp drop. Following its earnings report on February 5, the stock lost almost 40% of its value in a matter of days. What triggered such a dramatic move? Surprisingly little.

The company did two things that markets tend to overreact to:

It lowered its full-year sales outlook to a range of $642.5 million to $643.5 million, compared with prior guidance of $640 million to $646 million.

For the current quarter, it projected revenue of $143 million to $144 million, below the $150.4 million analysts were expecting.

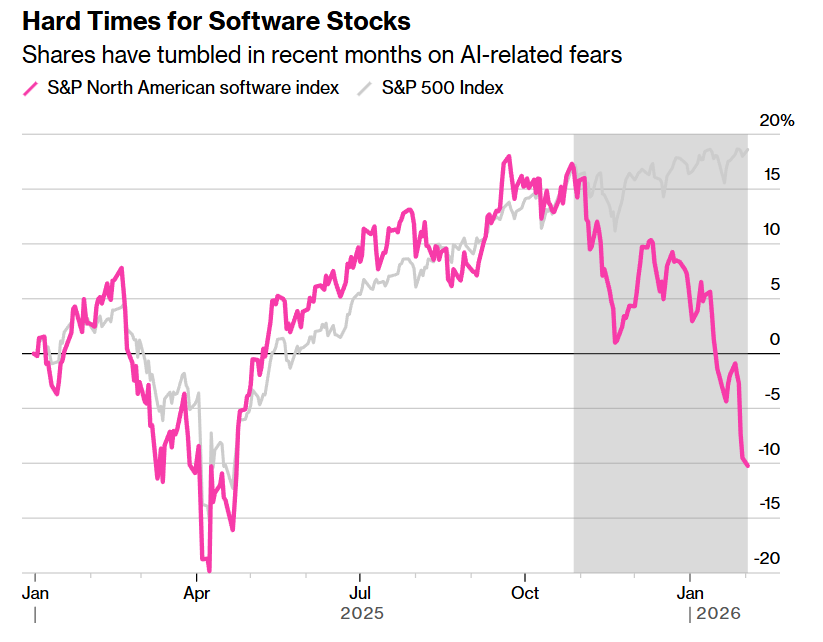

That sell-off looks harsh on its own, but it makes more sense in context. Before the crash, Doximity traded at a P/S of 11.39 and a P/E of 28.12. That valuation isn’t outrageous for a high-margin software company, but it did leave little room for disappointment. Once expectations slipped — even slightly — the stock was repriced quickly and brutally.

The broader market didn’t help. Software stocks have been under pressure across the board, as investors worry that AI tools will replace large chunks of existing software. This particular wave of selling was partly triggered by the release of Anthropic’s newest AI automation product. In our view, that fear has become indiscriminate — and in Doximity’s case, largely misplaced (more on that in “Pros”).

Taken together, these factors have pushed the stock down to levels that look disconnected from the underlying business. We think Doximity is now dramatically oversold.

Pros

Share Price Decline Looks Excessive. Doximity shares fell below $21, well under the IPO price of $26. Even without any positive surprises, this kind of move sets up a classic rebound scenario.

AI Is Not a Direct Threat — at Least Not Yet. Let’s tackle the biggest concern head on. In our view, Doximity is better insulated from AI disruption than most software companies.

Healthcare is a heavily regulated, compliance-driven environment. That’s where Doximity has a structural advantage over generic “cheap AI.” Its recruiting business, for example, relies on a verified clinician network and structured data on credentials and specialties. Making high-stakes physician hiring decisions based on outputs from an unverified chatbot is not something hospitals are eager to do.

More broadly, the idea that AI will simply “eat software” assumes organizations will abandon trusted platforms and build their own tools. That might happen in some industries. It’s far less likely in U.S. healthcare, where workflows are complex, liability is high, and compliance requirements are constant. If anything, bureaucratic systems tend to gravitate toward established, reputable vendors — not DIY experiments.

Doximity’s management also isn’t ignoring AI. The company has already rolled out several AI-powered features:

Doximity GPT, a compliance-friendly administrative writing assistant with clinical citations.

Doximity Scribe, which automates parts of clinical documentation.

PeerCheck, a physician-led validation layer designed to review and improve AI outputs.

So far, AI appears to be helping rather than hurting. Margins have improved, not deteriorated — no small feat given how expensive AI pivots can be. Based on what we know today, we think Doximity has at least a decade before AI becomes a serious competitive threat.

It’s also an insanely high-margin business. Gross margins above 90% are rare anywhere, and almost unheard of in healthcare-adjacent software. The fact that Doximity has maintained — and even improved — margins over time is a major point in its favor.

A Technical Rebound Looks Likely. From a market-structure perspective, U.S. software stocks look deeply oversold. When sentiment eventually shifts, Doximity has better-than-average odds of bouncing — especially given its strong fundamentals and relative insulation from AI fears.

Valuation Finally Makes Sense. With the share price around $25.69 and annual EPS of $1.19, Doximity now trades at a P/S of 10.1 and a P/E of 21.56. That’s below the average P/E of the U.S. software sector and supports the case for a rebound. Yes, the P/S is still on the high side — but for a business with these margins and defensibility, it’s reasonable.

Revenue Is Sticky Enough. Doximity’s net revenue retention (NRR) stands at 112%. That’s a strong signal that existing customers are spending more over time — not less. If AI were actively displacing Doximity’s offerings, NRR would likely fall below 100% fairly quickly. The fact that it hasn’t is very encouraging.

Note: net retention rate (NRR) shows how much money the company’s existing customers are spending compared to last year. 100% NRR means no change, less than 100% means customers are shrinking or leaving, and more than 100% means customers are expanding their spending.

A Realistic M&A Target. After the sell-off, Doximity’s market cap is about $4.76 billion. Given its margins, defensibility, and healthcare footprint it’s plausible the company could attract an acquisition offer at a meaningful premium.

Cons

Customer Concentration. One unnamed customer accounts for about 12% of revenue. That concentration gives the customer bargaining power and introduces risk if the relationship changes.

A Growth Ceiling Ahead. Doximity is already deeply embedded in the U.S. healthcare system: roughly 80% of U.S. physicians use the platform, along with more than 60% of nurse practitioners and physician assistants, and over 90% of graduating medical students. While the company doesn’t disclose the exact number of paying customers, the business model makes implications clear. Clinician membership is essentially free; monetization comes primarily from organizations. That means Doximity already covers a large share of the available workflow in its niche — management, recruiting, and routine administrative tools in healthcare.

The flip side of that dominance is growth math. When you already “own the room,” revenue growth tends to slow. As a result, Doximity’s top-line expansion is likely to become more muted with each passing quarter, simply because there’s less untouched territory left. That’s not a deal-breaker, but it does mean we shouldn’t expect explosive growth unless Doximity raises prices, expands its product lineup, or pursues acquisitions and/or international expansion. Each of those levers could work, but they also carry risks and could also weigh on margins over time.

Multiple Battlefronts. Doximity doesn’t face a single, obvious archrival. Instead, it competes across several fronts at once. Clinician engagement overlaps with platforms like LinkedIn, Facebook, Google, and X. Marketing budgets compete with health-focused sites such as WebMD and Medscape, as well as offline channels. Recruiting faces traditional staffing agencies. Workflow management overlaps with tools like QGenda, Zoom, and Microsoft Teams. Telehealth competes with players such as Teladoc and Amwell.

So far, competition hasn’t meaningfully dented Doximity’s economics — its margins make that clear. But over time, pressure could increase as more companies roll out AI-enabled tools aimed at pieces of the healthcare workflow. A more subtle risk is internal: management may feel tempted to buy competitors to defend or expand its position. Acquisitions in healthcare tend to be expensive, and they’re not always kind to shareholders. Finally, Doximity’s extremely high margins are a beacon. They signal that this niche is very profitable, which can attract new entrants — including well-funded digital-health startups backed by venture capital.

Slim Chance of a U.S. Medical Administration Overhaul. This is a long-shot risk, but it’s worth acknowledging. U.S. healthcare’s administrative inefficiency is widely recognized, and serious reform is occasionally discussed — even if it’s politically painful and notoriously hard to execute. Cutting red tape, aligning incentives, and resolving congressional gridlock would be a herculean task.

Still, the conversation itself could matter. Companies like Doximity thrive in a system where hospitals and health systems — often lacking the internal expertise to benchmark software costs — end up paying premium prices for “must-have” administrative tools. Doximity’s gross margin north of 90% didn’t appear by accident. Healthcare has historically had a lot of leeway to pass costs along, and that environment supports unusually high software margins.

If policymakers ever made a serious attempt to cap administrative spending, uncomfortable questions would follow: how much are hospitals paying for each layer of software, and why? Even the announcement of a credible reform effort could pressure stocks like Doximity’s. In an extreme scenario, meaningful simplification of healthcare administration could undermine parts of the business model. That said, this remains mostly theoretical. U.S. pharmaceutical companies, for example, have been political targets for decades — often dragging their stock prices around — yet actual structural change has been limited.

Verdict

Buy now at $25.69. From here, we see three scenarios:

Base case: A rebound to $32 within 15 months, implying a 24.5% gain.

Bull case: A return to $39 over roughly three years as sentiment resets, a ~52% gain.

Long-term case: The business compounds steadily and delivers around 11% CAGR over the next decade.