Built for Chaos: Betting on Commodity Trading Houses

Unlocked Edition #7. March 2026

Our pick today is a moderately speculative bet on an overlooked corner of the market: shares of commodity trading houses, which we expect to have an exceptional financial year.

You’re reading a free weekly idea. Want 1–3 ideas every Tuesday plus access to 40+ live ideas? Consider becoming a paid subscriber. Already a subscriber? Enjoy the new Unlocked Edition at no additional cost.

Issuers

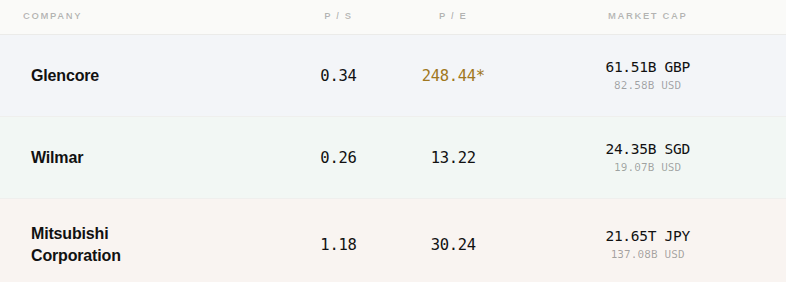

Glencore (London Stock Exchange: GLEN) — Swiss commodity trading giant specializing in metals and minerals.

Wilmar International Limited (Singapore Exchange: F34) — Singapore-based firm specializing in feedstock and food trading.

Mitsubishi Corporation (Tokyo Stock Exchange: 8058) — Japanese trading house with a highly diversified portfolio spanning chemicals, fuels, electronics, metals, and IT. The company also provides professional services and consulting. One common mix-up worth clearing up: Mitsubishi Corporation does not make cars — that’s Mitsubishi Motors, a separate company.

Expected Profits

Glencore: 17.5% profit in 18 months; ~318% profit in 15 years, 10% CAGR (including dividends)

Wilmar International: 27% profit in 18 months; ~318% profit in 15 years, 10% CAGR (including dividends)

Mitsubishi Corporation: 16.5% profit in 18 months ~318% profit in 15 years, 10% CAGR (including dividends)

Description of the Business

Trading houses are sometimes just called “traders” — which, stripped of jargon, simply means merchant.

Here’s how it works in practice. A U.S. corn farmer wants to sell his harvest. He doesn’t have time to hunt for buyers halfway around the world, and arranging international delivery on his own would be a logistical nightmare. That’s where a trading house steps in. The trader finds a buyer — say, a supermarket chain in Taiwan — and handles everything in between.

The trader buys the corn from the farmer at $5 per bushel (a bushel is a standard U.S. and U.K. unit of volume; in this context, it equals roughly 38.691 kg) and sells it to the Taiwanese buyer at $6.25. That $1.25 spread sounds attractive — until you see where it goes. The trader is responsible for the entire journey: loading the grain at the farm, moving it into dedicated storage elevators, insuring the cargo at every stage, and then transporting it to port and on to the buyer by sea or air.

Of that $6.25 per bushel, roughly $1.10—$1.15 covers logistics: elevator loading and storage, freight, and insurance. With the corn itself costing $5 and delivery running about $1.15, the trader clears about $0.10 per bushel. And that $0.10 still has to cover staff costs (or agent fees, such as the inspectors who certify quality and volume), taxes, and, finally, profit.

In other words, this is an extremely thin-margin business. Gross margins hover around 1.6% of revenue — a figure that would make any software executive weep. Yet that paper-thin margin is by design, and it’s exactly what makes the model resilient.

So why does commodity trading exist at all? Because for most producers and buyers, managing international logistics and supply chains in-house is either too expensive or too complicated. They’re happy to outsource the work — much like the average PC user doesn’t install Windows themselves. In theory, they could. In practice, it’s not worth the time and frustration, so they pay someone who specializes in exactly that.

That said, at sufficiently large scale, the economics can shift. If a company’s production volumes are massive enough, the savings from running an in-house trading desk can justify the investment. Among major agricultural producers, Archer Daniels Midland (ADM) and Cargill both trade actively. Among oil and gas majors, Shell and ExxonMobil do the same. The pattern holds broadly: the larger the business, the stronger the incentive to manage commodity trading internally. Smaller trading firms might operate in the millions; the largest work at the scale of tens or even hundreds of billions of dollars.

Commodity trading also requires enormous amounts of capital. Traders routinely handle volumes worth hundreds of millions — sometimes billions — of dollars, and very few companies have that kind of cash sitting idle. That’s why trading houses depend on constant access to credit lines.

It’s also why some of the world’s largest banks — Goldman Sachs, Morgan Stanley, JPMorgan Chase, and Barclays, among others — participate in commodity trading directly. Big banks already have the balance sheets for it, along with deep industry relationships built through lending and advisory work.

In short, the core functions of a trading house are: matching sellers with buyers, and organizing the storage and transportation of the commodity from origin to destination. Put simply, commodity traders help keep the global economy moving by ensuring goods actually reach the people who need them.

Pros

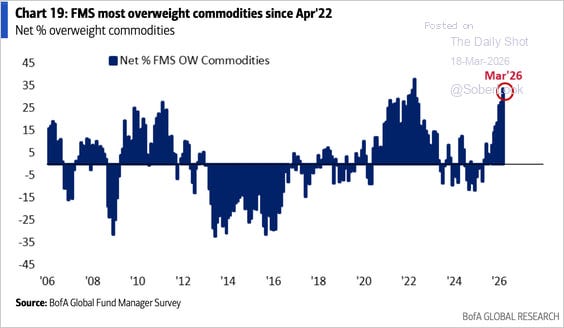

A Perfect Storm for Profits. This year is shaping up to be a strong one for commodity traders. Following the start of the latest U.S. military campaign in Iran, markets were thrown into turmoil. Commodity prices surged — and not just oil and gas. Agricultural products, fertilizers, and a wide range of industrial inputs all moved sharply higher.

The 2022 playbook is instructive here. When the war in Eastern Europe sent energy prices soaring, commodity trading houses booked record profits — because when prices rise sharply enough and fast enough, traders can typically negotiate wider margins. We think 2026 could be a repeat.

AI-Proof and Competition-Proof. Could trading house customers handle supply-chain logistics on their own, with the help of AI-powered tools? In principle, yes — but it only makes economic sense at a very large scale, where saving half a percentage point translates into tens or hundreds of millions of dollars in value.

And even then, building an in-house trading operation is no small feat. You could deploy hundreds of AI agents, but a significant portion of this work still requires time on the ground and on the road: commodities are often sourced from dozens of producers, and relationships and execution matter enormously. Once you replace an external trader with an internal solution, you’re committed to running it permanently — with all the overhead that implies.

That’s why we believe commodity trading houses will remain relevant for a long time. They specialize in finding markets and organizing supply chains, and they do it professionally and at scale.

Cheap Enough to Notice. All three stocks are relatively inexpensive — and in today’s market, that’s no small thing. Even after a wave of sell-offs across the broader market, genuinely cheap stocks remain surprisingly hard to find.

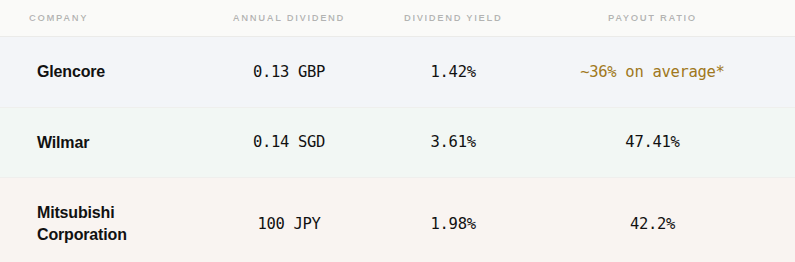

Dividend Upside. When commodity trading houses have a standout year, they tend to reward shareholders — either by raising the regular dividend or paying a special one-time distribution. Given our expectation for a strong 2026, these stocks could also attract yield-seeking investors looking for income in a volatile environment.

Built for Chaos. A few years ago, we came across a book that reframed how we think about this industry: World for Sale: Money, Power, and the Traders Who Barter the Earth’s Resources, by Javier Blas and Jack Farchy. It’s a collection of stories about how trading houses go to extraordinary lengths to procure essential resources — often striking deals in war-torn regions or under intense time pressure.

After reading it, you stop thinking of trading houses as mere middlemen. They’re more like corporate fixers — companies that can deliver when delivery is hardest. In a world that’s becoming more volatile, that skill set is increasingly valuable.

In-house supply-chain managers can’t always be expected to keep cargo moving when shipping lanes are disrupted or insurance markets freeze up. Commodity traders, with their expertise, experience, and deep networks, often can — and historically have. That’s why we believe today’s instability could put a premium on their valuations.

Cons

Credit Risk Is Always Lurking. Trading houses operate on borrowed money, essentially around the clock. They often control far more in assets than their equity would suggest — selling goods they don’t yet physically hold, financed by credit from banks and counterparties. When markets are calm, that system hums along. But when volatility spikes, credit can tighten fast — and a trading house can be brought to its knees in a matter of days.

Trafigura’s experience in 2022 is a useful reminder. That year was a record-breaker in terms of revenue and profits, yet few remember that in March 2022, rapid commodity price spikes triggered billions of dollars in margin calls, and Trafigura faced a severe liquidity crunch. The company survived by raising a significant amount of emergency funding, but it was a close call.

The current turmoil in the Middle East could trigger a similar wave of stress — or worse, a wave of insolvencies — that restricts the credit lines available to the companies we’re recommending. In a worst-case scenario, it could mean something more serious. This is a permanent structural risk in the sector, and it should be priced into your thinking accordingly.

The risk is particularly relevant right now. The conflict has lifted inflation expectations, and central banks are talking less about rate cuts and more about potential hikes. Higher borrowing costs can set off a chain reaction: defaults, tighter bank risk appetite, reduced credit availability — exactly the conditions that squeeze commodity traders hardest.

The silver lining: the largest trading houses (including the publicly traded ones we’ve selected) are widely considered “too big to fail.” Without them, supply disruptions could reach a scale severe enough to cause rationing-style outcomes even in wealthy countries. In an extreme scenario, some form of government support might be available. But share prices could take a serious hit before any rescue materializes.

The Same Tailwinds Can Become Headwinds. Traders may outperform financially during periods of crisis — but they’re not immune to the disruptions they’re navigating. Border closures, surging freight rates, transportation shortages, and prohibitively expensive cargo insurance can all compress margins and weigh on profits. The very conditions that create trading opportunities can also make them harder and costlier to execute.

Verdict

Glencore — Buy at 518.2 GBX.

A quick note on the currency: GBX (Penny Sterling) and GBP (Pound Sterling) are both used to quote U.K. stocks. 100 GBX equals 1 GBP, so 518.2 GBX equals 5.18 GBP.

The shares are trading near historic highs, but we still see two viable paths forward:

Over the next 18 months, we think Glencore can capitalize on current market volatility and reach 610 GBX — a 17.5% gain, excluding dividends.

For long-term holders, the target is 10% CAGR over 15 years, including dividends.

Wilmar International — Buy at 3.77 SGD.

The stock is trading at about two-thirds of its 2021 peak, which gives it meaningful room to recover if our profit thesis plays out. Two ways to approach it:

Target 4.80 SGD over the next 18 months — a 27% gain, excluding dividends.

Hold for 15 years and target ~10% CAGR, including dividends.

Mitsubishi Corporation — Buy at 5,397 JPY.

The stock is at historic highs, so further upside will require more patience and conviction. That said, the company delivered strong revenue and profits in both 2021 and 2022 — two years defined by supply-chain stress — and we expect a similar dynamic to play out under current conditions. Two ways to play it:

Target 6,300 JPY over the next 18 months — a 16.5% gain, excluding dividends.

Hold for 15 years and target ~10% CAGR, including dividends.