Blueprints for a Bounce: The Case for Nemetschek

Unlocked Edition #10. April 2026

Today we have a pretty speculative idea: buy the German software stock Nemetschek SE (Deutsche Börse Xetra: NEM). While it isn’t especially cheap, we think it still has meaningful upside potential.

You’re reading a free weekly idea. Want 1–3 ideas every Tuesday plus access to 80+ live ideas? Consider becoming a paid subscriber. Already a paying subscriber? Enjoy the new Unlocked Edition at no additional cost.

Expected profits

19% profit in 14 months

~159% profit in 10 years (10% CAGR, incl. dividends)

Description of the business

Nemetschek SE is a long-established German company, founded in 1963. Today, it’s a technology player specializing in software for architecture, engineering, and construction (AEC).

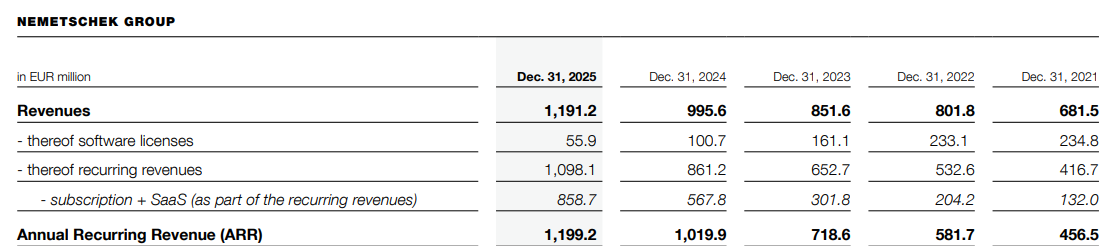

Here’s how Nemetschek’s revenue broke down in 2025:

Design — 45.42%. Software for architects and engineers used for design, modeling, structural engineering, data management, checking, and visualization.

Segment EBITDA margin: 28.1%.Build — 40.4%. Solutions for construction companies, developers, suppliers, general contractors, planning offices, and civil engineers. The software supports estimating, tendering, scheduling, cost accounting, construction ERP, digital documentation, collaboration, and on-site workflows.

Segment EBITDA margin: 35.8%.Media — 9.92%. Creative tools: software for 2D/3D design, motion graphics, visual effects, rendering, sculpting, and visualization.

Segment EBITDA margin: 33.9%.Manage — 4.35%. Software for real estate, facility, and workplace management — focused on workspace usage, maintenance, efficiency, and broader building operations.

Segment EBITDA margin: 12%.

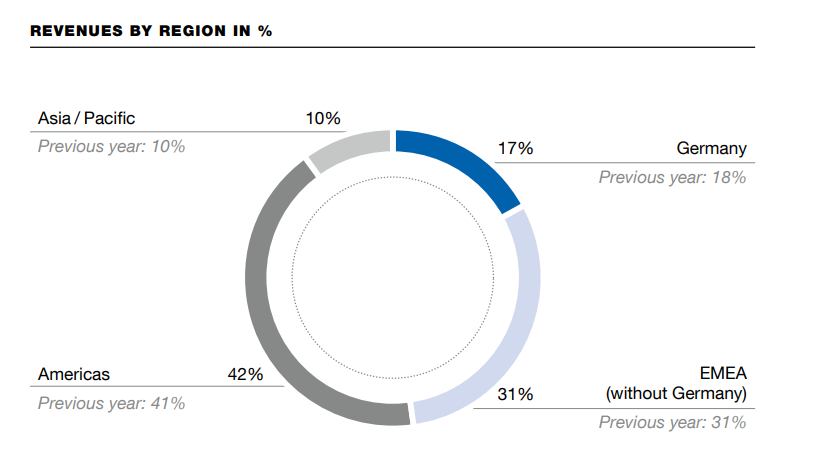

The U.S. is Nemetschek’s single biggest market, accounting for 41.8% of sales. Germany is the next largest at 18% of revenue. The rest comes from other (unnamed) countries.

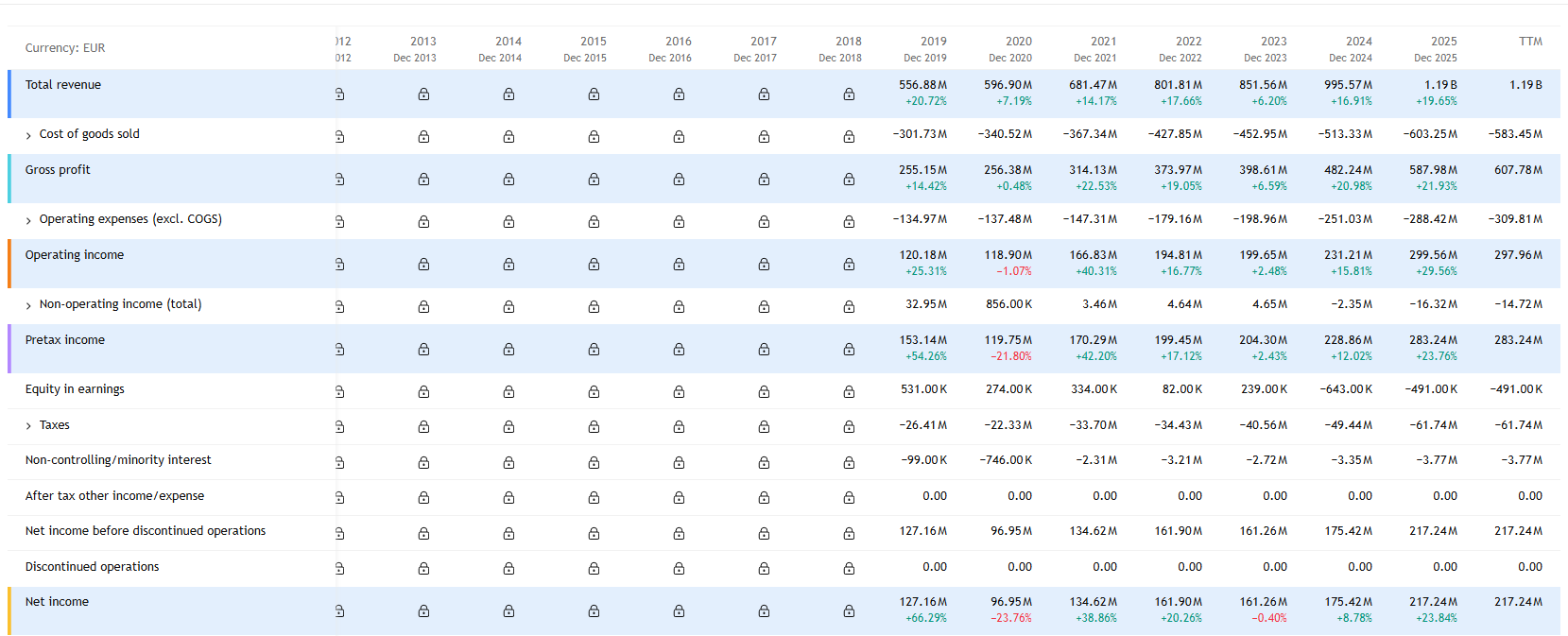

Nemetschek is profitable: in 2025, its gross margin was 51%, its operating margin was 25%, and its net margin was 18.23%.

Pros

The stock is down. In a philosophical sense, every sell-off is an invitation to a bounce. Nemetschek has lost about half of its market cap since July 2025, and much of that decline reflects the fact that the stock was previously overpriced.

Even now, NEM still looks relatively expensive (more on that in the “Cons”). Still, we think the upside factors (more on that in the “Pros”) justify expecting a rebound.

Rotation out of the U.S. Surprisingly, U.S. stocks still trade at roughly a 39% premium over the rest of the world. That could push some investors to rotate from the U.S. into other developed markets and pick up strong local tech names like Nemetschek.

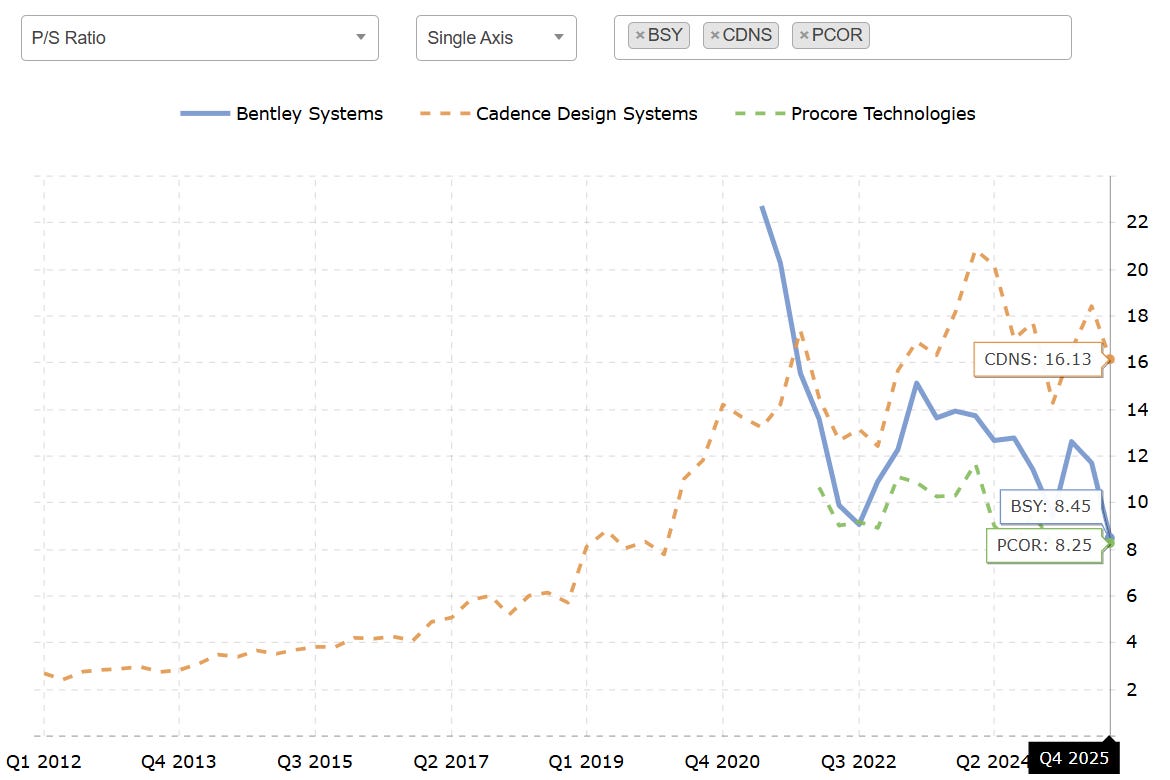

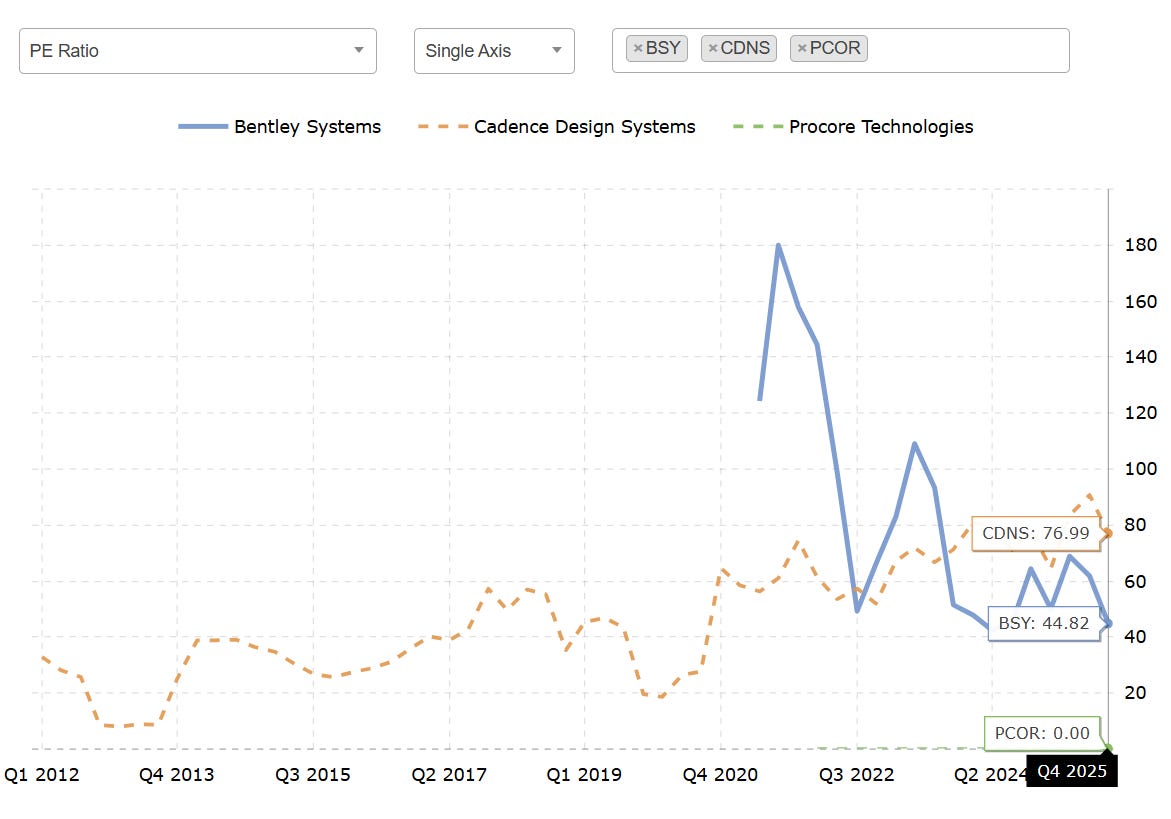

The U.S.-peer comparison helps Nemetschek: when you compare it with other engineering software names like Bentley Systems (NASDAQ: BSY), Cadence Design Systems (NASDAQ: CDNS), and Procore (NYSE: PCOR), Nemetschek’s valuation looks somewhat more muted. In other words, NEM can appeal to some U.S. investors as a “cheaper Cadence”.

Degree of stability. Nemetschek is a fairly predictable business, with a large share of revenue coming from recurring sources. That makes the stock attractive to investors who prioritize stability.

What we’re saying is this: while NEM isn’t as cheap as we’d like, it still delivers solid revenue growth and excellent margins — so it arguably deserves some valuation premium.

The market backdrop is supportive. Nemetschek’s sales and profits have grown for years for a simple reason: its software is in high demand, and that demand should remain strong for quite some time. It also helps that the engineering and construction industries still have surprisingly low levels of digitization, which leaves room for further adoption-driven growth. And with massive global engineering demand — from maintaining existing infrastructure to building new data centers — demand for engineering software should stay robust for a long time.

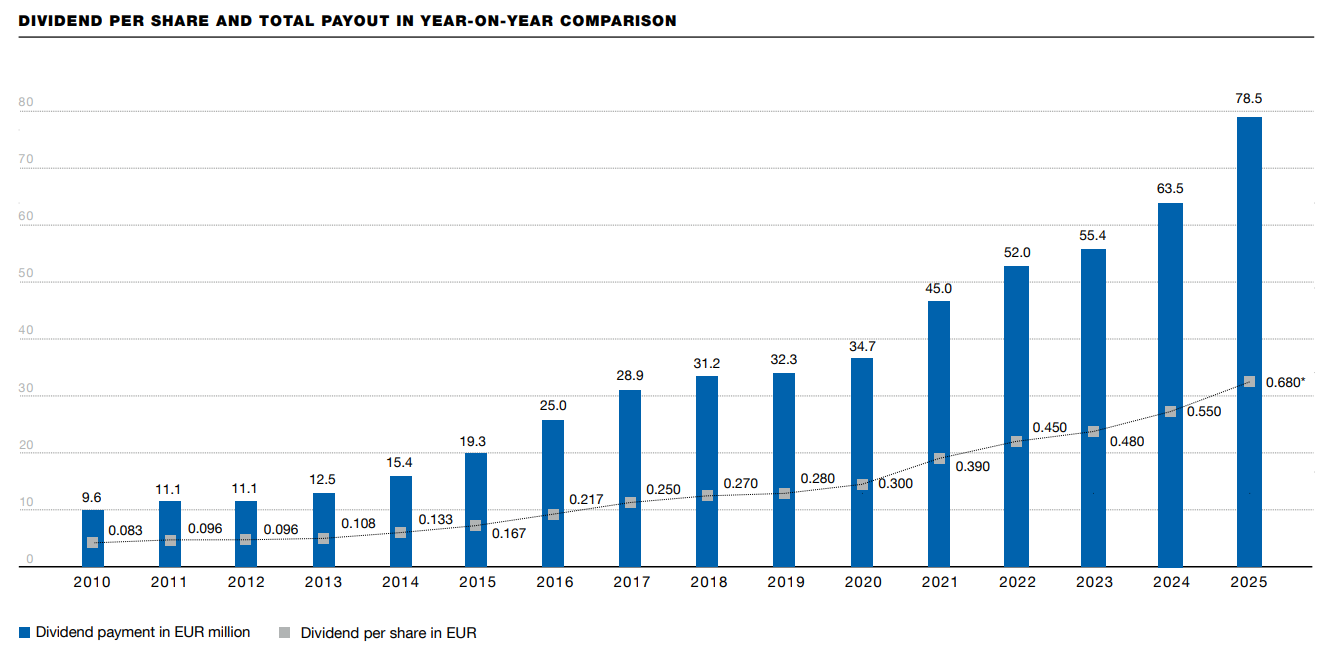

Dividend growth potential. Nemetschek pays €0.68 per share annually, which implies a 0.79% dividend yield — well below the German market average of about 2.5%. That said, dividend-paying tech stocks are relatively rare globally, and NEM’s payout has room to grow.

The company currently pays out about 36.15% of net profit as dividends, so in theory it could double the payout — especially if the long-term outlook continues to improve.

A good fit for M&A hunters. Nemetschek’s market cap is only about €8 billion, and given the company’s quality, it’s plausible it could attract a buyout offer in the foreseeable future. It’s even possible that a player like Cadence could show interest for exactly these reasons.

Cons

AI is an open question. AI tools pose a theoretical threat for two reasons:

More price competition. Cheaper (though less functional) AI and “vibe-coding” solutions could lure away some of Nemetschek’s smaller clients. That said, larger firms will still need Nemetschek’s software, especially given its compliance and data-protection standards — something today’s vibe-coded tools typically can’t match.

Higher spending to keep up. Nemetschek is effectively forced to invest in AI to stay competitive. The company is already embedding AI capabilities, which is strategically positive, but it can weigh on margins and profits.

For now, both risks remain mostly theoretical: Nemetschek’s margins are still strong, and there’s no clear evidence of customers leaving en masse for cheaper AI alternatives.

Not cheap on traditional multiples. Nemetschek’s P/E is more than 2x the German market average — around 36.81. Its P/S is also high even by U.S. standards, at about 6.84. That makes further upside harder to justify and increases the risk of valuation-driven volatility.

Weaker greenback. Nemetschek generates a little under half of its sales in the U.S., earning dollars — but it reports in euros. With the USD weakening over the past 1.5 years, there’s a real risk the next earnings report could disappoint investors: unless sales growth outpaces currency moves, Nemetschek’s reported revenue in euros may shrink once U.S.-dollar sales are translated.

Recent acquisition. In April 2026, NEM announced it would buy a 72% stake in the U.S. software company Heavy Construction Systems Specialists (HCSS) for $2.4 billion. It raises a bunch of questions.

The first is whether the new acquisition is worth it. HCSS is private, but media reports suggest its annual revenue is around $215 million, and its profitability is not publicly known (though its EBITDA margin is estimated at about 40%). That valuation looks expensive, and it’s fair to question how much of a boost it will deliver — and whether it’s really worth the price.

Another question is how NEM intends to pay for HCSS. The company has only about €0.258 billion in cash, so it’s very likely it will take on additional debt. Management indicated that “the deal won’t change the ownership structure,” meaning NEM does not plan to issue new shares. That implies more leverage, which would also reduce the likelihood of a meaningful dividend increase.

Also, there may be some ownership-related downside due to the deal structure. NEM is buying 72% of HCSS from Thoma Bravo, while the fund will retain a 28% stake. HCSS will be integrated into NEM’s Build segment, which means Thoma Bravo will effectively remain exposed to part of the Build business after the deal closes in the second half of 2026. That creates a theoretical risk that Thoma Bravo could eventually sell its stake, putting pressure on the shares.

On the other hand, there could be an upside: an active U.S. fund like Thoma Bravo could end up playing a meaningful role in shaping the asset and helping drive execution after the acquisition.

Verdict

Buy now at €66.50. The stock is currently far below the €130 level the stock reached in 2025, and that anchors our price expectations. We see two possible scenarios:

Bounce case: Hold until the stock to reach €78 within the next 14 months. That would be a 19% gain, excluding dividends.

Long-term case: Hold the stock for the next 10 years and target ~10% CAGR, including dividends.