Betting on Bureaucracy Beating AI (For Now)

Unlocked Edition #11. May 2026

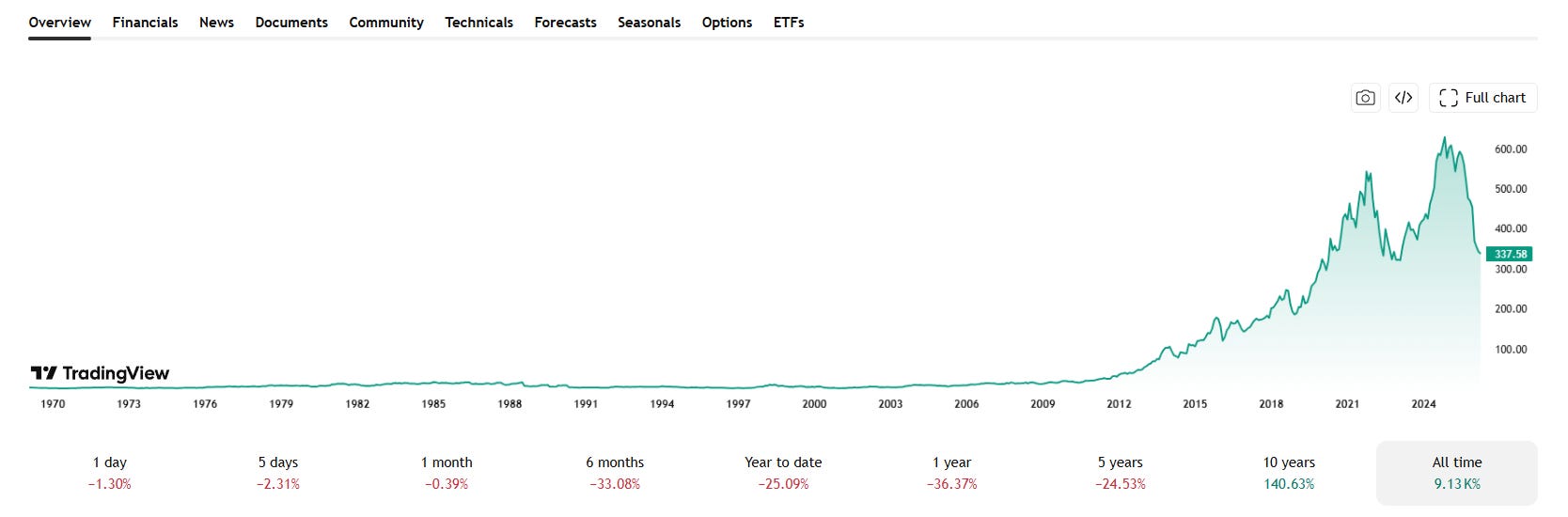

Today’s idea is a modestly speculative bet on a software company that governments can’t easily quit: Tyler Technologies (NYSE: TYL). The stock has been cut nearly in half over the past two years, and we think the sell-off has created a real entry point for a business that’s more durable than the market is currently giving it credit for.

You’re reading a free weekly idea. Want 1–3 ideas every Tuesday plus access to 80+ live ideas? Consider becoming a paid subscriber. Already a paying subscriber? Enjoy the new Unlocked Edition at no additional cost.

Expected Profits

18.5% profit in 14 months

~136% profit in 10 years, 9% CAGR

Description of the Business

Tyler Technologies (NYSE: TYL) is a U.S.-based technology company that develops and sells workflow software exclusively for the public sector. Its principal customers are local and state governments, federal agencies, school districts, and education agencies.

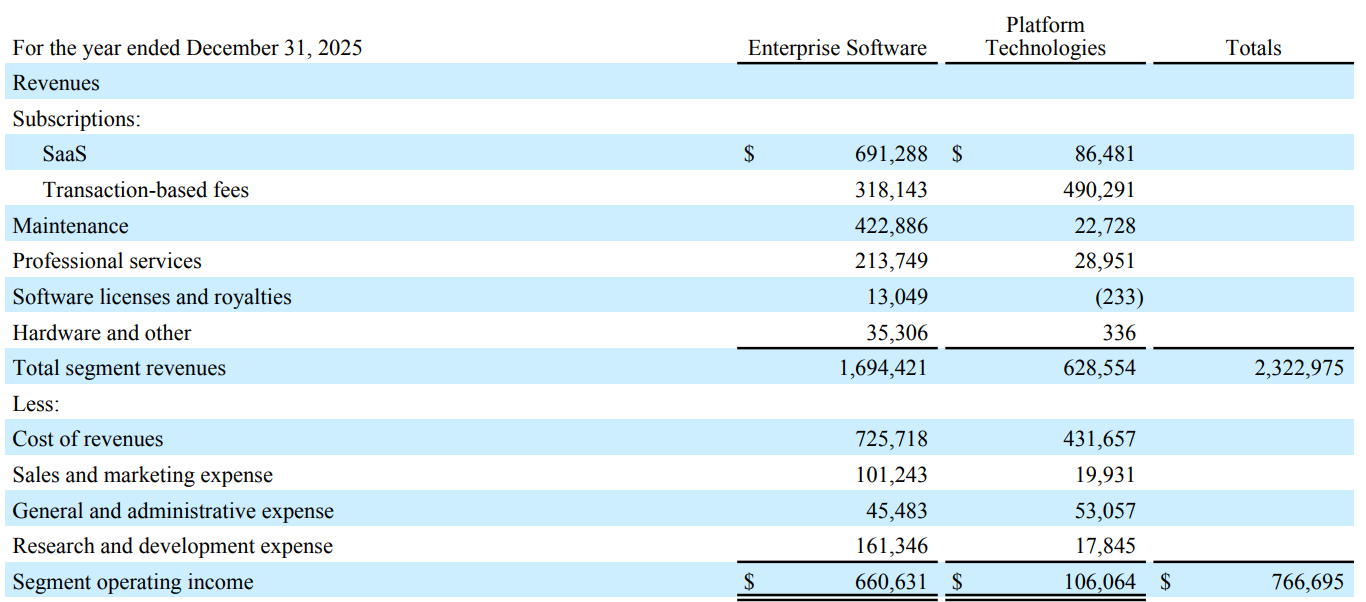

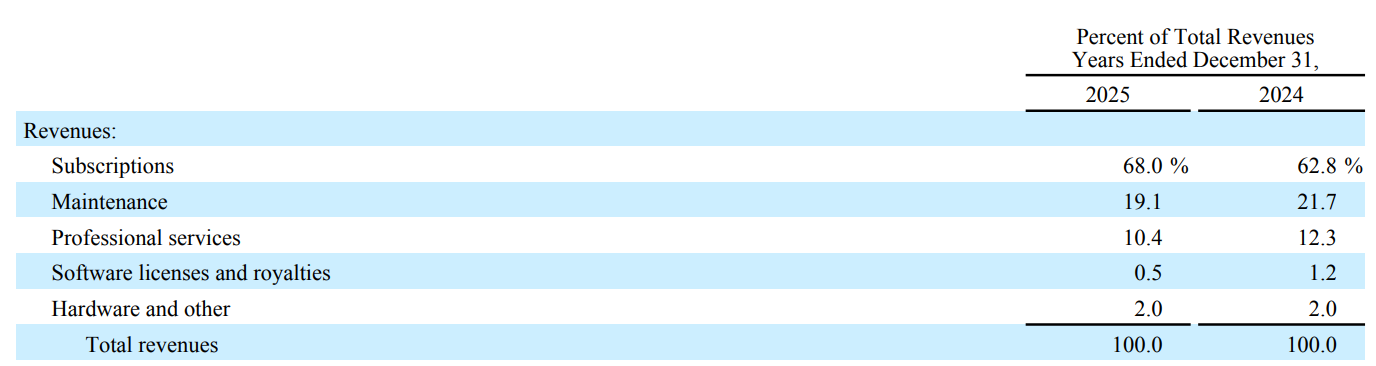

Here’s how Tyler’s revenue was structured in 2025:

Enterprise Software — 72.95%. The name undersells it: this segment powers core government operations — taxes, courts, education, property records, and more.

Segment operating margin: 38.96%.Platform Technologies — 27.05%. Online payments, digital government transactions, data platforms, dashboards, and workflow tools.

Segment operating margin: 16.86%.

Almost all of Tyler’s sales are generated in the U.S.

For 2025: gross margin — 46.46%, operating margin — 15.34%, net margin — 13.53%.

Why the Stock Is Down

Tyler’s stock has lost nearly half its value over the past two years. The decline appears to reflect a broader reassessment of high-multiple software stocks in an environment where AI is raising real questions about which software categories are defensible — and which aren’t. We think the market has been too aggressive in punishing Tyler, and that the sell-off has opened up a more attractive entry point than this business typically offers.

Pros

Not Obsolete — at Least Not Yet. This is the crux of the Tyler thesis, so it’s worth unpacking carefully. Most software stocks facing AI headwinds make an easy target: their products generate text, summarize content, or handle tasks that a well-prompted language model can replicate for a fraction of the cost. Tyler is different.

Tyler’s core products are record-keeping and workflow systems embedded inside government operations — courts, tax authorities, property records, police and emergency services, ERP platforms, permitting systems, school administration, and payment infrastructure. These aren’t text-generation tools. They carry user permissions, regulatory requirements, audit logs, compliance frameworks, system integrations, and payment rails that have been built up over years of implementation.

A city that adopts ChatGPT or Microsoft Copilot still needs the underlying database, workflow engine, and compliance layer that Tyler provides. AI can help draft a document, classify a record, or automate data entry — but it is not going to calculate municipal taxes, manage court case workflows, process permits, or dispatch emergency services. Tyler operates in a world of compliance obligations that off-the-shelf AI tools simply cannot address yet.

AI Integration Is Actually Happening. Tyler isn’t sitting still on AI — it’s embedding it directly into existing products. In Q1 2026, the company launched an early-adopter pilot adding agentic AI features directly into its applications, developed in collaboration with AWS and various AI model providers. It’s also rolling out agentic coding tools for its roughly 2,000 product-development employees.

Early results are encouraging. Tyler’s Resident AI Assistant is live in six states. In Indiana alone, around 17,000 residents use it monthly, generating almost 50,000 government-services queries. The company also reports that its AI-enabled Document Automation and Priority-Based Budgeting products are delivering productivity and labor-efficiency gains of 10–30%. For now, Tyler looks more like a beneficiary of AI adoption than a casualty of it.

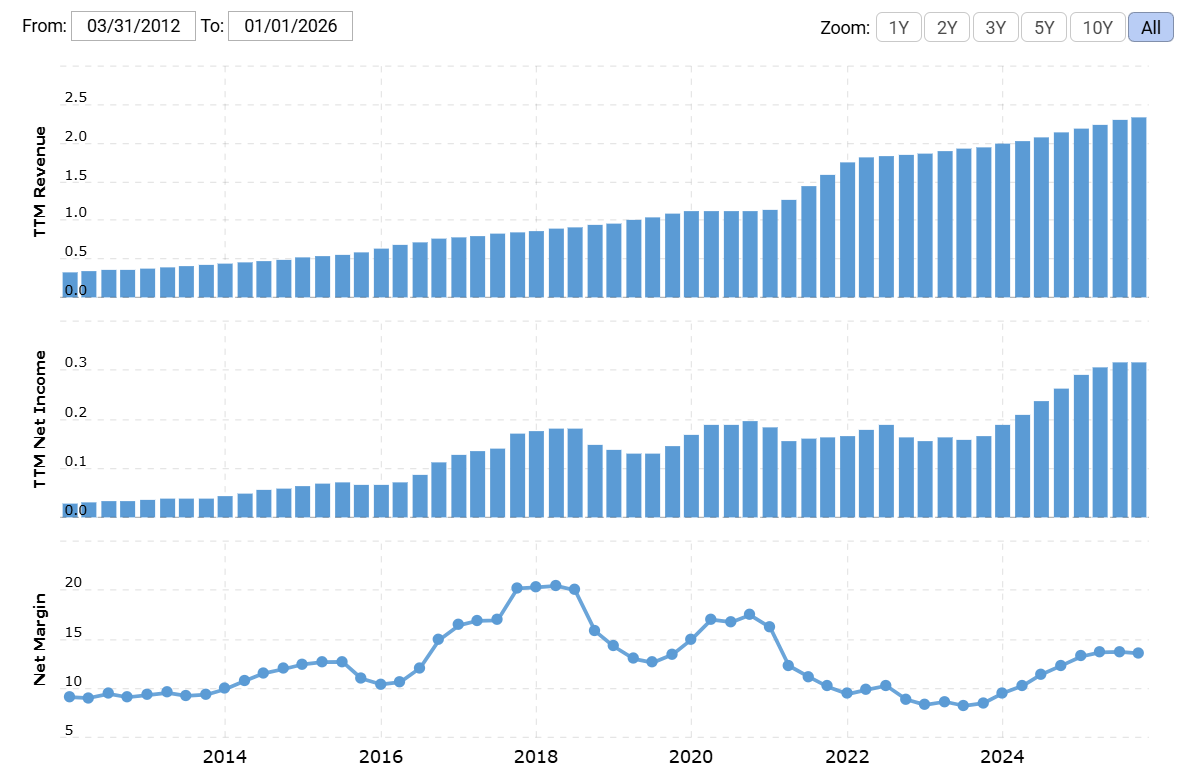

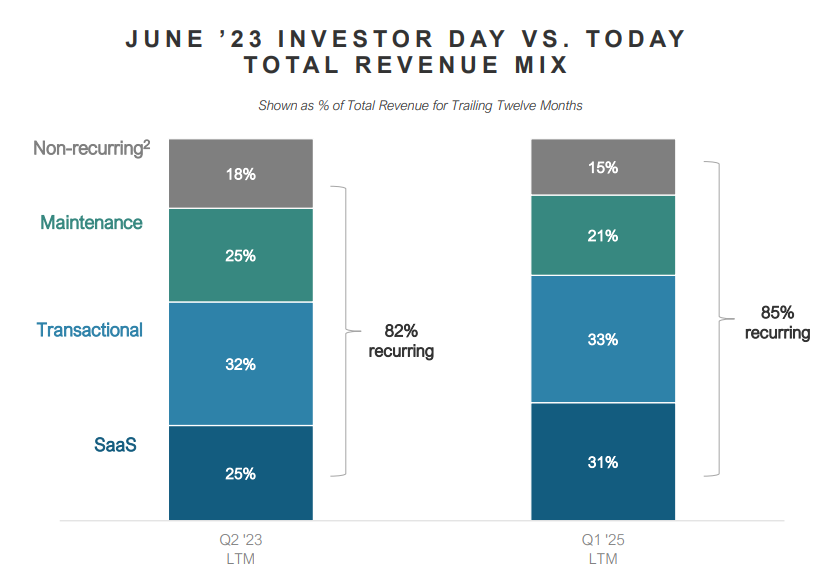

Sticky Revenue. Around two-thirds of Tyler’s revenue comes from subscriptions, and when you add in continuously renewed maintenance contracts and similar items, recurring revenue accounts for roughly 85% of the total. That stickiness isn’t accidental — switching away from Tyler means migrating sensitive government data, retraining public-sector workforces, rebuilding integrations, and navigating procurement cycles that can take years. Bureaucratic inertia is effectively a moat for Tyler. Investors who value predictability tend to pay a premium for businesses that look like this.

Dividend Potential. Tyler doesn’t pay a dividend today, but with earnings of about $7.20 per share annually, there’s a credible case for a meaningful payout. A dividend of $4.00 per share or more is plausible — and initiating one would likely attract a new class of income-oriented investors, giving the share price a lift in the process.

Acquisition Potential. A dominant position in a sticky, high-margin, government-software niche — with a market cap around $14.33 billion — is exactly the profile that attracts acquirers. Private equity in particular tends to gravitate toward businesses like this: predictable cash flows, high switching costs, and a customer base that isn’t going anywhere. A take-private scenario is not difficult to imagine.

Cons

AI Could Still Be a Threat. We’ve made the case that Tyler is more AI-resistant than most. But “more resistant” is not “immune,” and there are several specific ways that AI pressure could show up in the financials over time.

Lower Services and Add-On Revenue. If AI automates implementation work, document processing, citizen support, budgeting analysis, or back-office administration, Tyler could see demand erode for certain professional services and lower-value software modules. The company itself warns investors that AI tools may be seen as automating functions that have traditionally driven demand for some Tyler products.

Higher R&D Costs. Staying competitive means keeping up, and keeping up costs money. In 2025, Tyler reported that R&D expenses rose partly due to new product initiatives, including AI-related investments — a line item that is unlikely to shrink.

Cybersecurity and Data Exposure. Tyler handles sensitive government data at scale, and the company acknowledges in its annual report that AI increases the risk of cyberattacks, data breaches, and accidental exposure of proprietary information. Moving workloads to the cloud adds another layer of potential vulnerability.

Pressure from Larger Platforms. Microsoft, AWS, OpenAI, Anthropic, and vertical AI startups are all capable of targeting the edges of Tyler’s workflow — resident chatbots, document automation, data search, budgeting tools. If those capabilities become commoditized, some of Tyler’s add-on revenue could lose its differentiation.

Becoming the “Smaller Partner.” Today, government employees live inside Tyler systems — which means Tyler controls the workflow. But if AI agents become the primary interface between workers and their software (“summarize this case,” “approve this invoice”), some of that control could migrate toward the AI orchestration layer. If Microsoft, AWS, OpenAI, or a vertical AI startup becomes the main interface, Tyler risks being positioned as the underlying database rather than the center of gravity. That probably doesn’t break the business — but it could hurt the valuation multiple, which is already doing a lot of work at current prices.

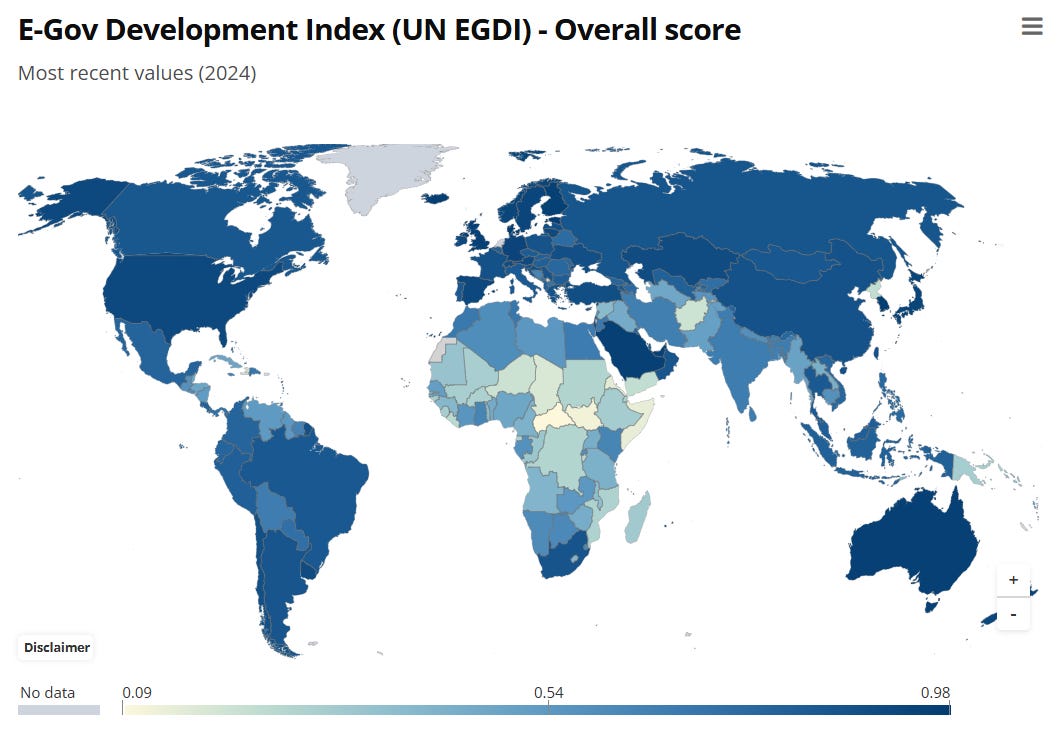

A Saturated Home Market. The U.S. scores 0.92 out of 1.00 on the e-government development index — meaning most of the obvious digitization work has already been done. There’s limited room for the kind of broad-based government IT expansion that would meaningfully accelerate Tyler’s growth domestically. International markets with lower e-government penetration exist, but breaking into them would require substantial investment, and Tyler has shown little appetite for that kind of geographic expansion so far.

Very Expensive. There’s no sugarcoating this one. Tyler trades at a P/S of 6.39 and a P/E of 47.5 — elevated even by U.S. standards, which are themselves elevated by global standards. At those multiples, the stock is priced for continued strong execution, and there isn’t much margin for error. Any stumble in growth or margins could be met with a disproportionate market reaction.

Verdict

Buy now at $337. The stock is well below its historic peak, and we see two scenarios from here:

A bounce to $400 within the next 14 months — 18.5% gain, excluding dividends.

Roughly 9% CAGR over the next 10 years.