5 Ways to Ride the Copper Wave

Unlocked Edition #5. February 2026

If there’s one metal quietly sitting at the center of AI servers, electric vehicles, wind turbines, and power grids, it’s copper. And right now, the red metal is behaving like it knows it’s indispensable. Today we’re looking at a basket of copper-mining stocks positioned to benefit from what may be a structural shift in copper pricing — not just a short-term spike.

You’re reading a free weekly idea. Want 1–3 ideas every Tuesday plus access to 40+ live ideas? Consider becoming a paid subscriber. Already a subscriber? Enjoy the new Unlocked Edition at no additional cost.

Expected Profits

28% profit in 19 months (Central Asia Metals)

29.5% profit in 18 months (KGHM Polska Miedź)

26.5% profit in 18 months (China Nonferrous Mining Corp.)

25% profit in 18 months (Nittetsu Mining)

19.5% profit in 18 months (iShares Copper and Metals Mining ETF)

Issuers

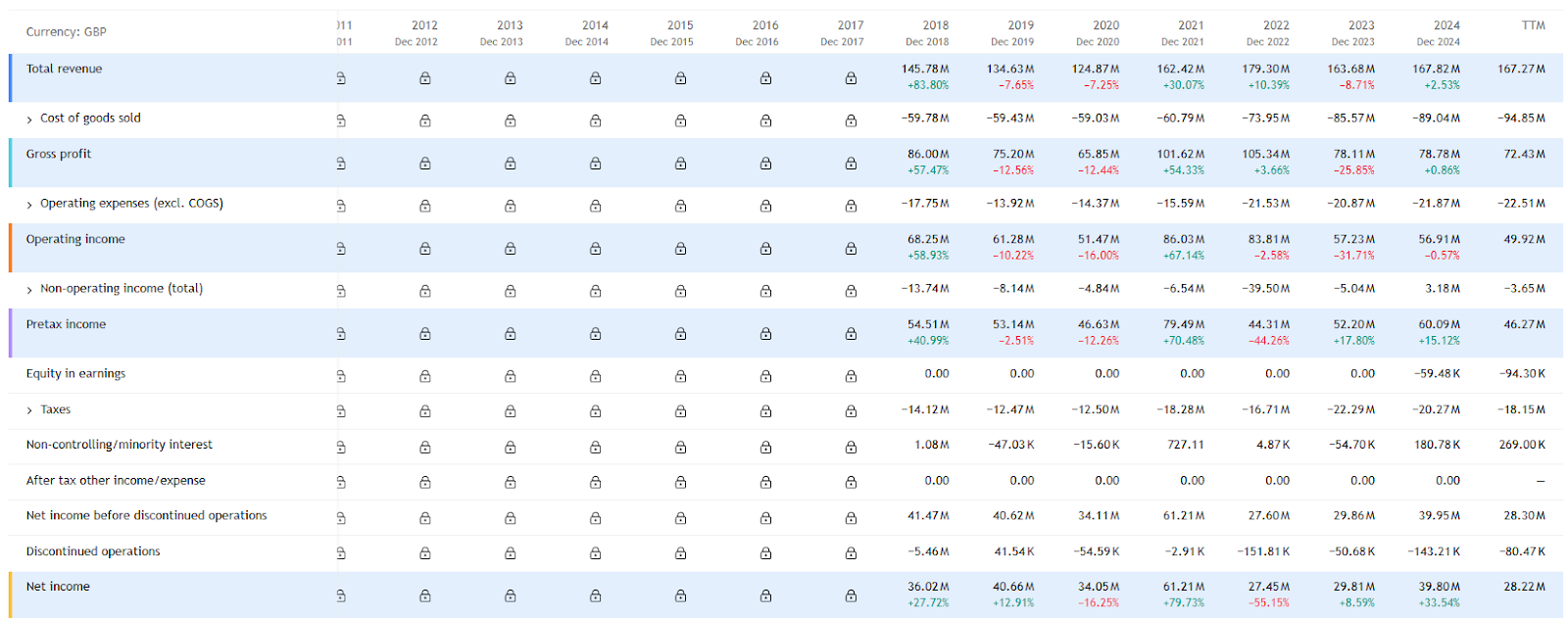

Central Asia Metals (London Stock Exchange: CAML) is a UK-based mining company operating primarily in Kazakhstan. Just under 57% of its revenue comes from copper; the rest generated by a zinc-lead mine in North Macedonia.

P/S: 2.6

P/E: 15.45

Market Cap: 394.85 million GBP ($533 million)

Dividend Yield: 5.83% (0.18 GBP per share annually; payout ratio 79.89%)

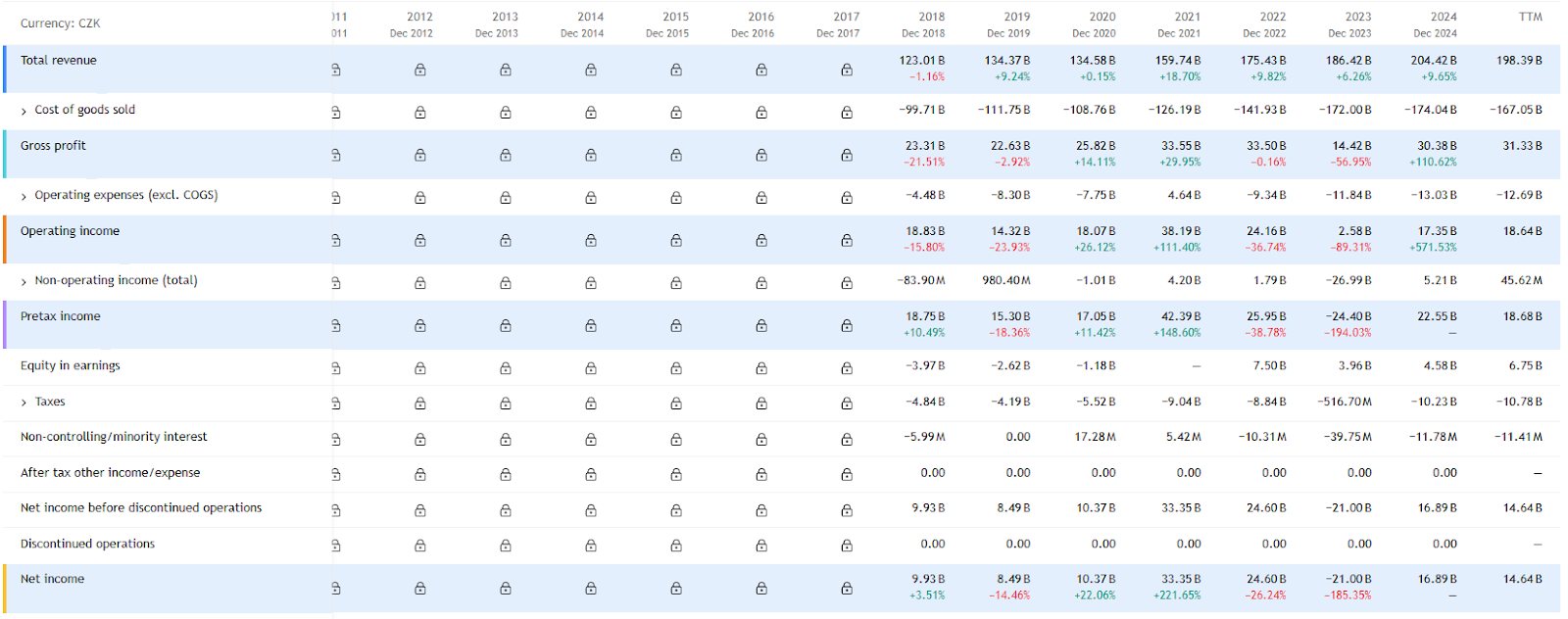

KGHM Polska Miedź S.A. (Prague Stock Exchange: KGH) is a Polish mining company listed in the Czech Republic. It operates mines in Poland, the U.S. and Chile.

P/S: 1.69

P/E: 22.93

Market Cap: 362.29 billion CZK ($17.7 billion)

Dividend Yield: –

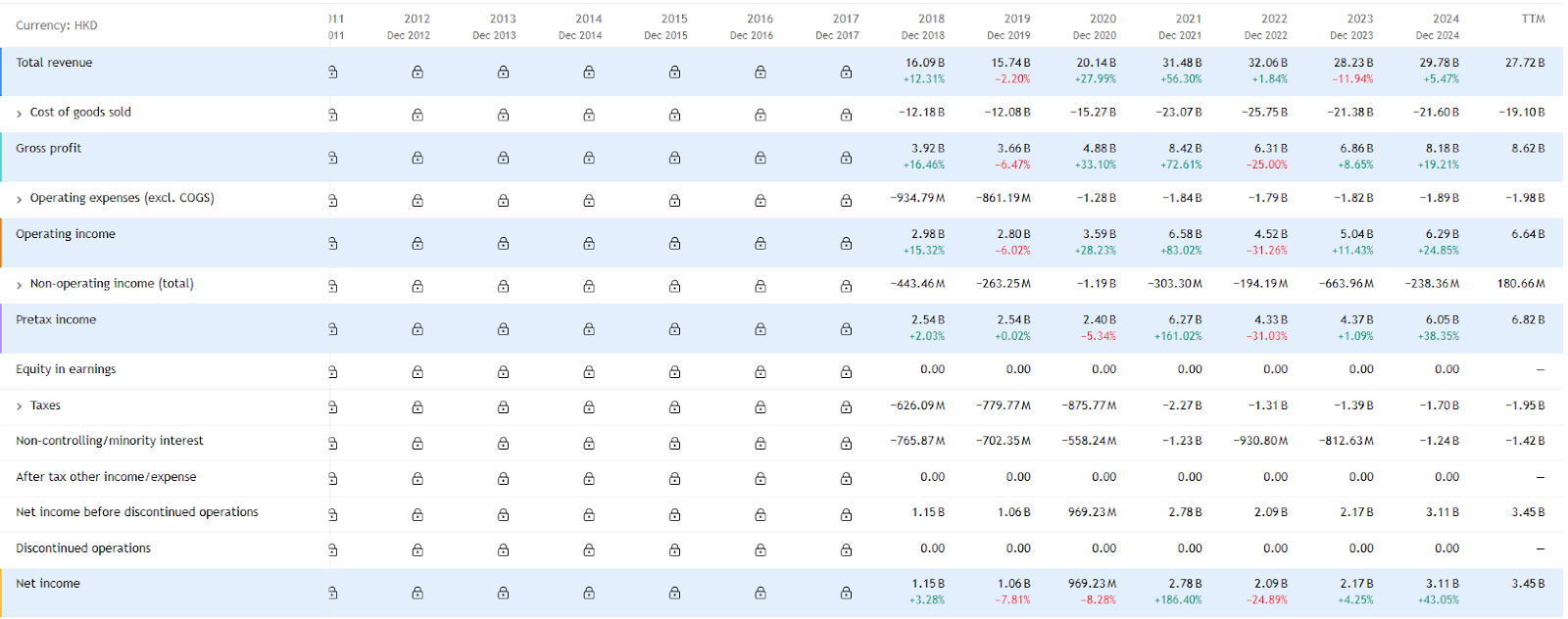

China Nonferrous Mining Corp (Hong Kong Stock Exchange: 1258) is a Chinese holding company focused primarily on copper production.

P/S: 2.21

P/E: 17.83

Market Cap: 61.14 billion HKD ($7.82 billion)

Dividend Yield: 2.15% (0.34 HKD per share a year; payout ratio 41.75%)

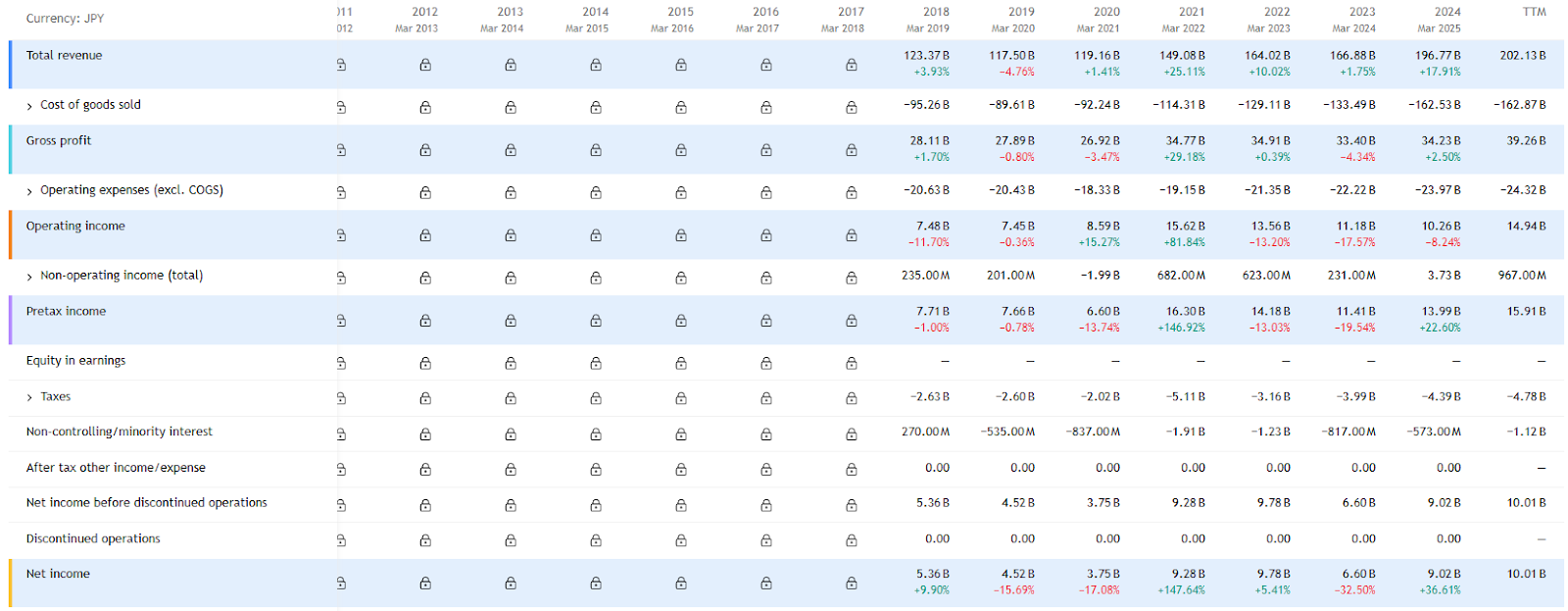

Nittetsu Mining (Tokyo Stock Exchange: 1515) is a Japanese copper producer with additional exposure to real estate and other businesses.

P/S: 1.43

P/E: 28.71

Market Cap: 293.08 billion JPY ($1.88 billion)

Dividend Yield: 1.37% (44.8 JPY per share annually; payout ratio 40.97%)

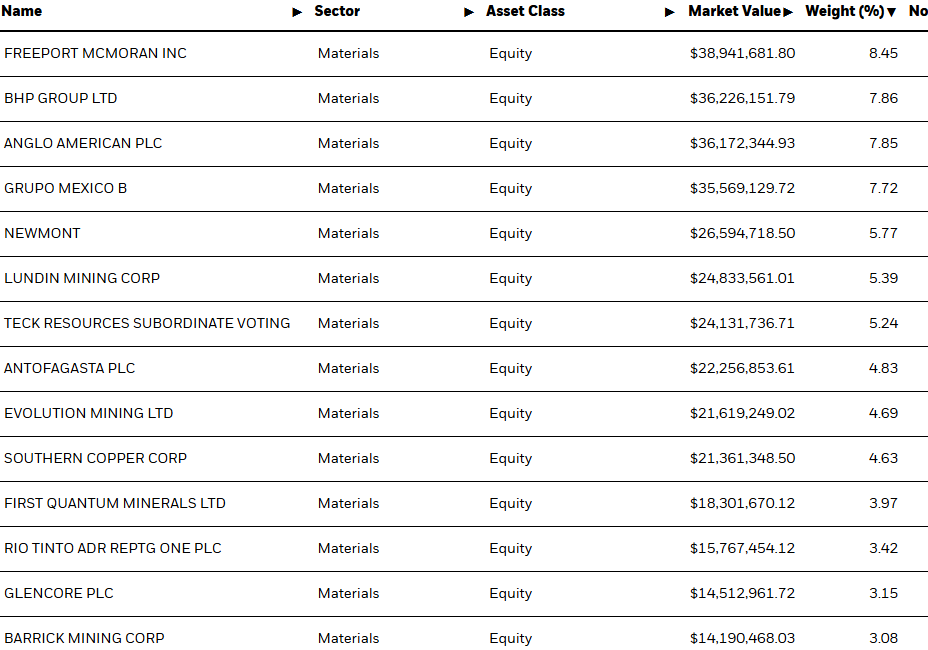

iShares Copper and Metals Mining ETF (NASDAQ: ICOP) provides diversified exposure to major global miners. Large Western producers such as Freeport and Newmont make up a significant share of its holdings.

Pros

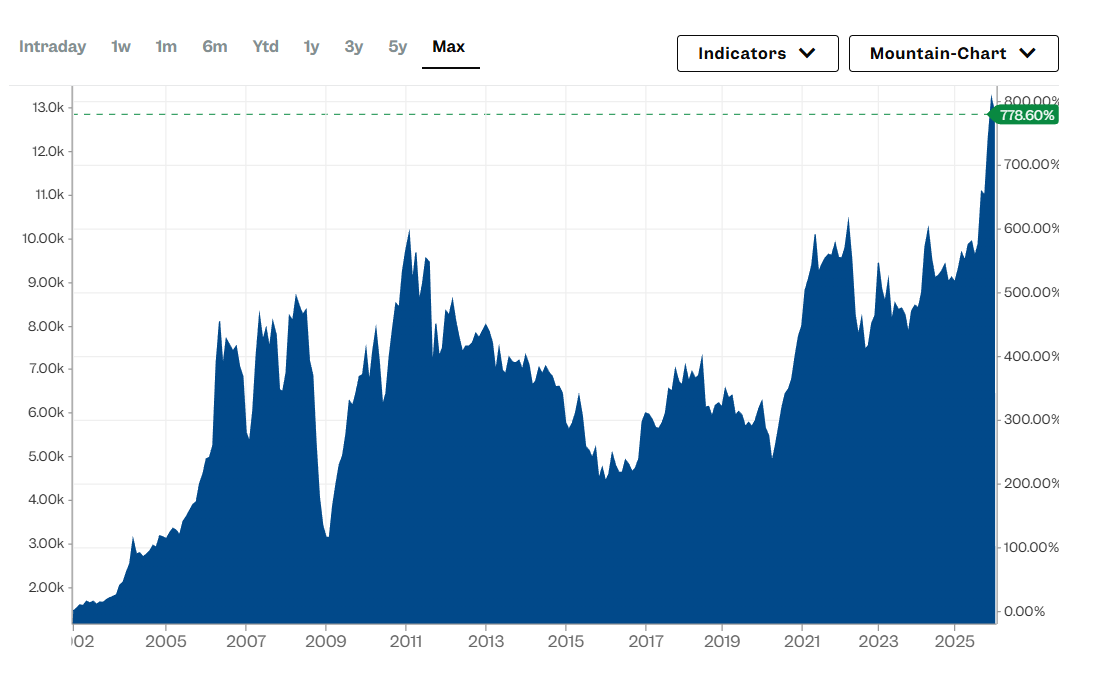

The Bullish Case for Copper. Copper has climbed nearly 35% over the past year. That kind of move can look speculative at first glance, but the drivers beneath it are structural rather than emotional.

Start with supply. Major copper discoveries are becoming increasingly rare. Copper has always been considered “abundant,” but economically viable, high-grade deposits are harder to find than many assume. The pipeline of new, large-scale discoveries has thinned meaningfully over the past decade. When new supply struggles to keep up, the long-term risk tilts toward shortages — and markets tend to price that in early.

Now layer in demand. Forecasts suggest global copper demand could be roughly 40% higher by 2040 than it was in 2024. That growth isn’t just coming from traditional sectors like housing and heavy industry. It’s being pulled forward by structural themes that aren’t going away:

AI data centers require enormous volumes of copper wiring and infrastructure.

Electric vehicles contain substantially more copper than internal combustion cars.

Wind, solar, battery storage, and grid modernization are all copper-intensive.

In other words, copper is quietly embedded in every “future-facing” industry investors are excited about. When demand expands structurally and supply responds slowly, price floors tend to reset higher.

Valuations Leave Room for Upside. What makes this setup interesting is that many of the miners haven’t priced in perfection. Despite copper’s strength, most of these stocks are not trading at euphoric multiples or historic highs. That provides breathing room. If copper prices stay elevated or climb further, higher realized prices should translate into stronger revenue, healthier margins, and potentially richer dividends.

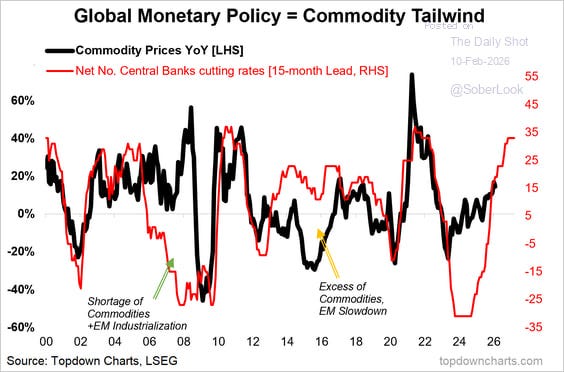

Rate Cuts Could Amplify the Move. Central banks globally have been leaning towards easing. Lower policy rates make borrowing cheaper, stimulate consumption, and typically accelerate economic activity. Historically, broad rate-cut cycles have coincided with stronger commodity prices. If that pattern holds, copper may not be done running.

Strategic Optionality Is Real. Several of these companies aren’t enormous in absolute dollar terms. In a world increasingly focused on critical minerals and supply security, overseas buyers or strategic investors may find certain copper assets attractive. We’re not betting the thesis on M&A — but in commodities tied to electrification and AI, strategic value is rarely zero.

Cons

Forecasts Are Catching Up — But Not Fully Bullish Yet. Copper currently trades around $12,800 per ton, already above many published forecasts that sit below $13,000. We expect those projections will gradually adjust upward — similar to what happened with gold last year — but until they do, the lack of overtly bullish analyst targets could weigh on sentiment.

There’s also positioning risk. Commodity allocations have increased as the rally gained momentum. If investors decide to lock in gains simultaneously, price pullbacks can be swift.

Scarcity Cuts Both Ways. The same scarcity story supporting higher prices also forces miners to spend more. New copper projects are capital-intensive, and developing them often requires billions in upfront investment. Meanwhile, older mines tend to see declining ore grades, which makes extraction more complex and expensive. Even in a strong copper market, miners may need to reinvest a substantial portion of cash flow simply to sustain production.

Disruptions Boost Prices — But Increase Volatility. Part of copper’s recent strength was event-driven. In 2025, an earthquake hit the Kamoa–Kakula mine in the DRC, triggering flooding. Another earthquake disrupted Chile’s El Teniente operation. Indonesia’s Grasberg mine — one of the world’s largest — suffered a collapse that halted production. In Peru, strikes temporarily shut down the Constancia mine.

Each event tightened global supply and supported prices. But they also highlight how fragile copper production can be. Mining is exposed to geology, labor disputes, weather, and political instability. The same forces that push prices higher can also inject sharp volatility into the market.

Geography adds another layer. Many new projects are concentrated in regions with rising political and security risk. Regulatory changes, logistics bottlenecks, or social unrest can disrupt output with little warning. In copper, volatility is part of the operating model.

High Prices Invite More Supply. When copper trades near record highs, producers respond. Companies ramp up output, accelerate development, and explore aggressively. That can lead to temporary oversupply cycles — and commodities are famous for sharp reversals when supply catches up.

Copper’s long-term case may be strong, but short-term swings are part of the terrain.

Tariff Headlines Can Move the Market Overnight. Copper’s rally hasn’t been driven solely by supply shortages and electrification demand. Trade-war dynamics have also played a meaningful role.

In the summer of 2025, U.S. President Donald Trump announced plans to impose a 50% tariff on copper imports. That announcement alone triggered a noticeable jump in copper prices, as markets quickly priced in tighter U.S. supply. Ultimately, the tariffs that were implemented applied only to semi-finished copper products — not refined metal or cathodes — which tempered the impact.

However, the story didn’t end there. The U.S. Department of Commerce outlined potential tariffs of 15% in 2027 and 30% in 2028 on refined copper and cathodes. That prospect encouraged U.S. buyers to front-run potential duties by building inventories early, effectively pulling forward demand and supporting prices in the short term.

More recently, the Supreme Court canceled most Trump-era tariffs. Copper-related measures, however, remain in place — and there is still room for escalation. Heavier duties could be introduced going forward, particularly if policymakers attempt to compensate for tariffs struck down by the court. If that happens, U.S. copper consumption could decline. That matters, even though the U.S. represents only about 7.85% of global copper demand — a non-trivial share in a tight market.

At the same time, the opposite risk is equally real. If more aggressive 2027–2028 tariff proposals are ultimately not implemented, copper prices could fall. U.S. inventory-building would likely slow or reverse, and the emotional component of the market could amplify the move. In fact, we’ve already seen how sensitive copper is to policy headlines: in late July 2025, when news broke that tariffs would not apply broadly across all copper categories, prices plunged roughly 20% in a single day — wiping out months of gains.

Rotation and Equity-Specific Risk. Capital flows can shift quickly. The same rotation out of software that has recently benefited “hard asset” sectors like mining could reverse just as fast. If the U.S. tech sector continues to look oversold, investors may decide to buy the dip in software — pulling money out of physical-resource stocks, including copper miners. That dynamic could pressure the space, especially given that most of the individual stocks we cover are listed outside the U.S., which may limit their appeal to domestic investors.

The iShares ETF could be particularly sensitive in such a scenario. Its core holdings are large-cap Western miners that already trade at somewhat elevated multiples, often with P/S ratios above 3. If sentiment cools, those names could compress quickly.

Copper Stocks Are Not Copper Itself. Mining shares carry company-specific risks — leverage, operational risks, cost inflation, execution missteps — and they can lag the metal even in a strong commodity environment. Copper prices may rise, but equity performance depends on discipline, capital allocation, and operational stability. Over time, higher copper prices should translate into strong profits for well-managed producers. But the path from metal price to shareholder return is rarely linear.

Verdict

Central Asia Metals — Buy at 234.5 GBX. We expect a move to 300 GBX within 19 months (still below its 2018 peak of 323 GBX). That would be a 28% gain, excluding dividends.

Note: GBX (Penny Sterling) and GBP (British Pound Sterling) are both used to represent UK currency: 100 GBX equals 1 GBP. So 234.5 GBX = 2.34 GBP.

KGHM Polska Miedź — Buy at 1,694.5 CZK. Our 18-month target is 2,200 CZK, below the 2,280 CZK level last seen in January 2026. That implies a 29.5% gain.

China Nonferrous Mining Corp — Buy at 14.99 HKD. Although the stock trades near historic highs, valuations remain reasonable given copper’s backdrop. We target 19 HKD within 18 months — a 26.5% gain, excluding dividends.

Nittetsu Mining — Buy at 4,160 JPY. Despite trading at all-time highs, its valuation is not stretched. We see potential for 5,200 JPY over the next 18 months — a 25% gain, excluding dividends.

iShares Copper and Metals Mining ETF — Buy at $56.05. We expect the ETF to break above prior highs and reach $67 within 18 months — a 19.5% gain.